2026 State of GTM | Benchmarks & Data

ICONIQ's 2026 GTM report + public company efficiency metrics

Paraglide (AI platform handling billing inquiries, collections, and disputes) just raised a round led by Bessemer to enable companies to get paid on time with less manual involvement.

My AR teams have always spent way too much time in their finance inbox: answering billing queries, chasing customers, chasing down PO numbers, and handling disputes…It’s high-volume, boring, and repetitive. Which makes it a perfect place to use AI agents.

2026 State of GTM

Below are my favorite slides from ICONIQ’s recent GTM report (2026 State of GTM), some relevant public company GTM metrics, and some thoughts on how I am thinking about the data.

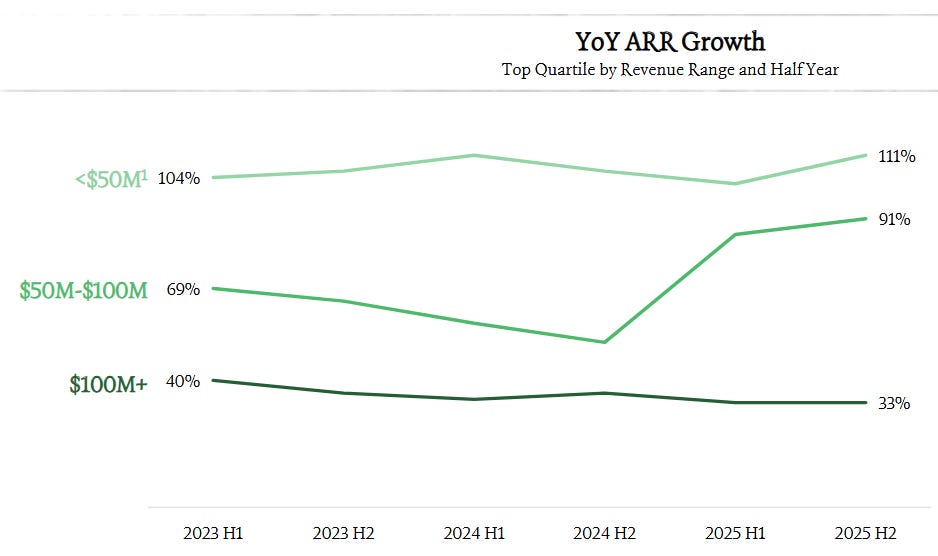

Revenue Growth

Companies with <$100M ARR are showing an acceleration in revenue growth. I think we can likely attribute this to all the new AI-native hyper-growth companies. The $100M+ category is still being dragged down by “legacy software” companies that are slower growth.

Note: below are ICONIQ’s top-quartile growth rates and ICONIQ is already a top-decile VC firm. So it is the best of the best.

There are A LOT more non-AI-native software companies with much lower growth than this. But if you aren’t near ICONIQ’s top-quartile growth, good luck raising money in 2026.

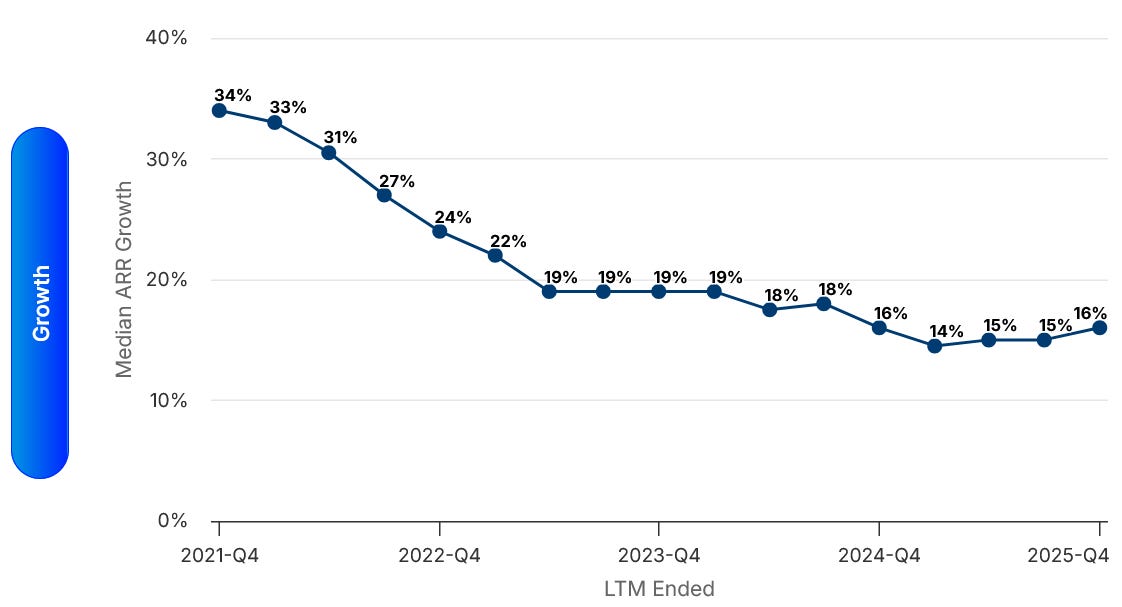

While at a much larger scale, public company revenue growth is just 16% today. However, it seems like we have bottomed and are even slightly accelerating, so we will take the win!

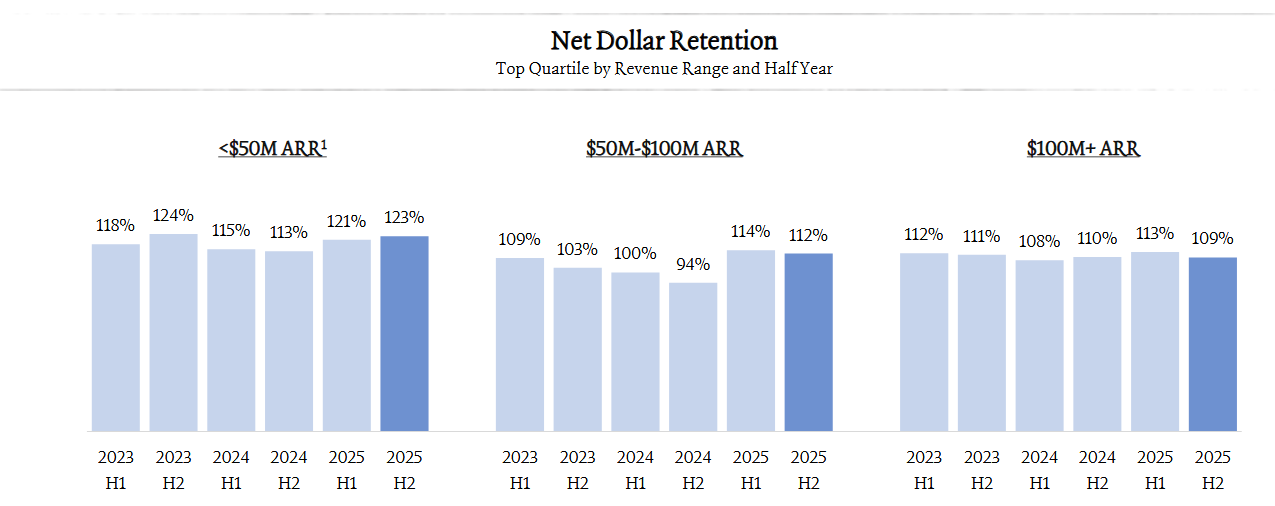

Retention

NRR seems to be holding steady, but…remember that this is top-quartile NRR. The difference between top-quartile and everyone else is going to grow much larger over the next 12-18 months, especially with NRR.

NRR can be a very lagging metric on the health of a business. Things like long contracts and vendor price increases can maintain NRR temporarily but eventually churn will hit.

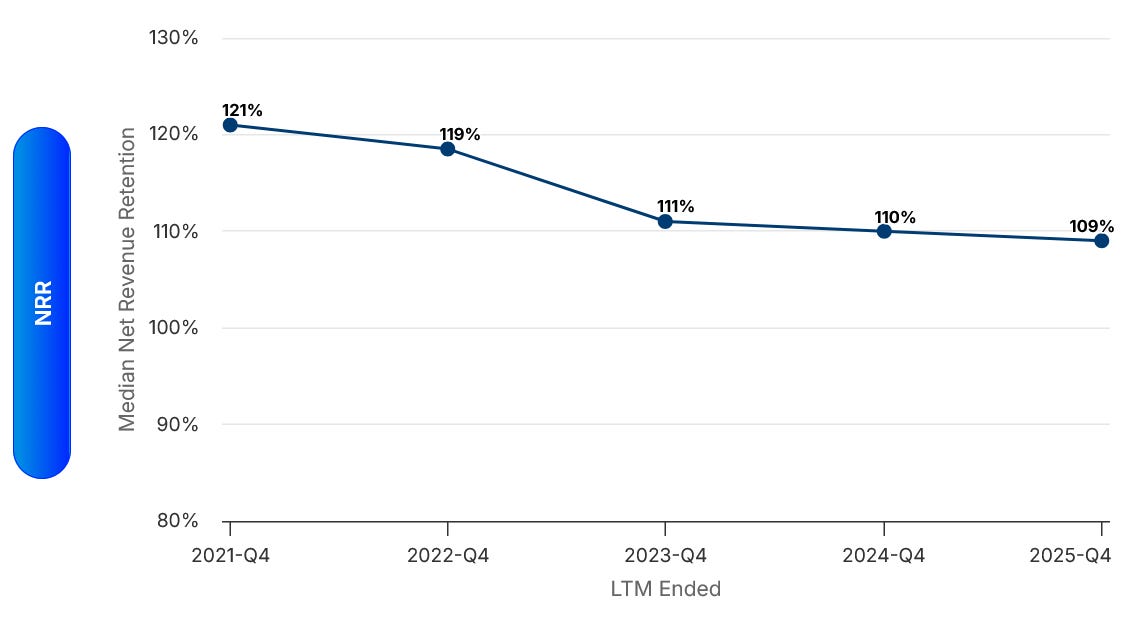

Public company NRR is still declining and it lines up with the $100M+ ARR bucket from ICONIQ’s report (both 109% NRR).

The thing I worry most about software company valuations is the durability of revenue. NRR and GRR are already lagging metrics, so if these keep declining then valuation multiples are going to continue to compress…It’s why public software stocks keep falling. No one is confident on revenue durability.

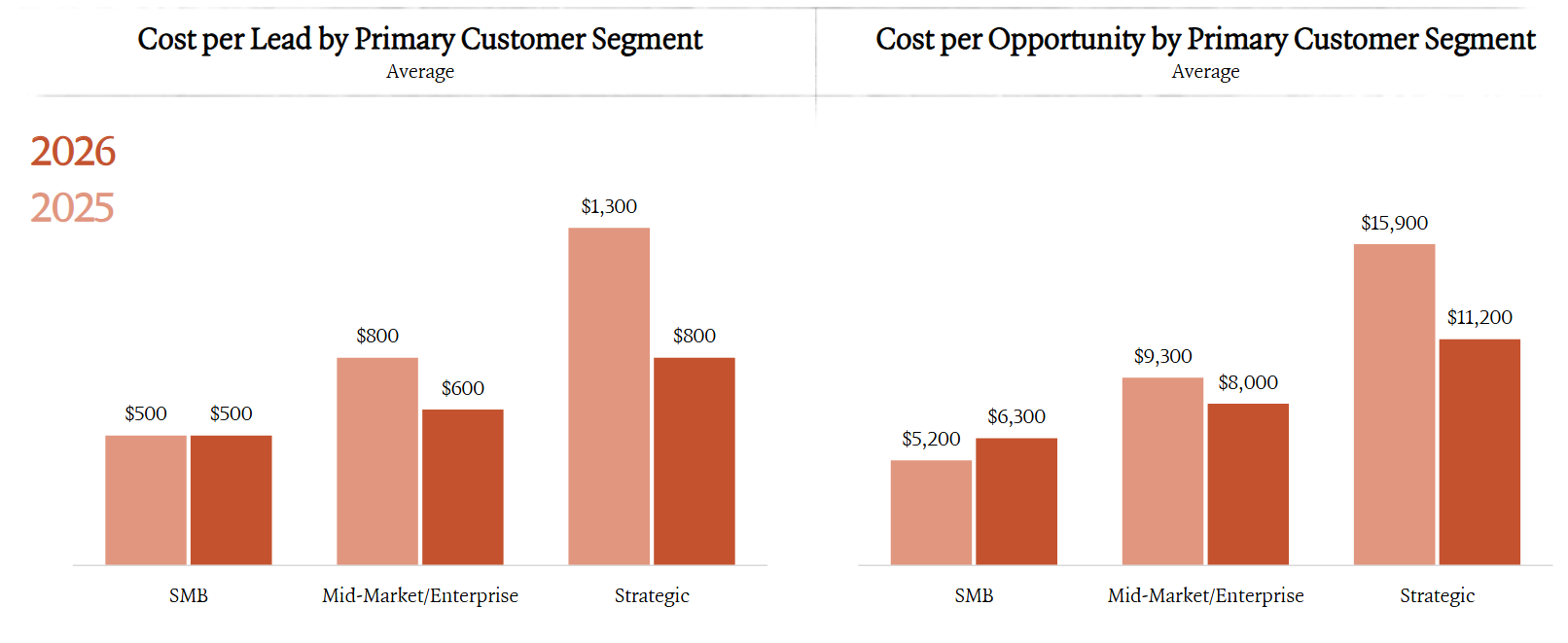

GTM Efficiency

The average dollar costs in ICONIQ’s report don’t mean much, but the trend is interesting. Cost for leads and opportunities dropped significantly over the past year, except in the SMB space.

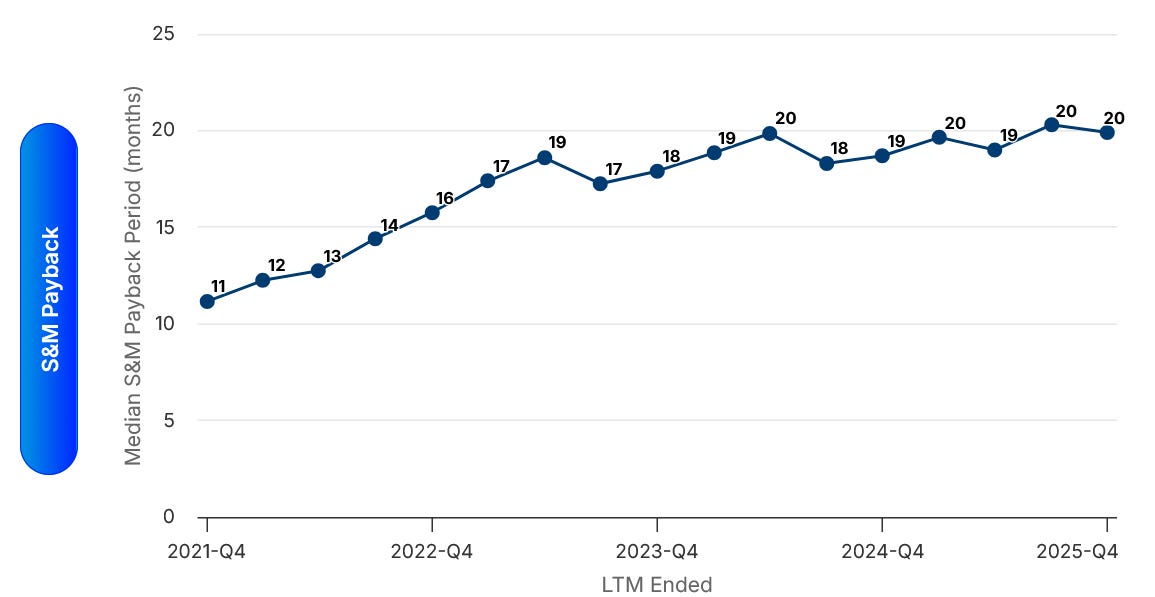

While still up significantly from 2021, CAC payback period has been fairly steady for several quarters for public companies.

CAC payback period should be a top focus metric for companies in 2026. The durability of revenue is uncertain and that has implications for customer lifetime value. Reducing the risk period by cutting the payback period is important.

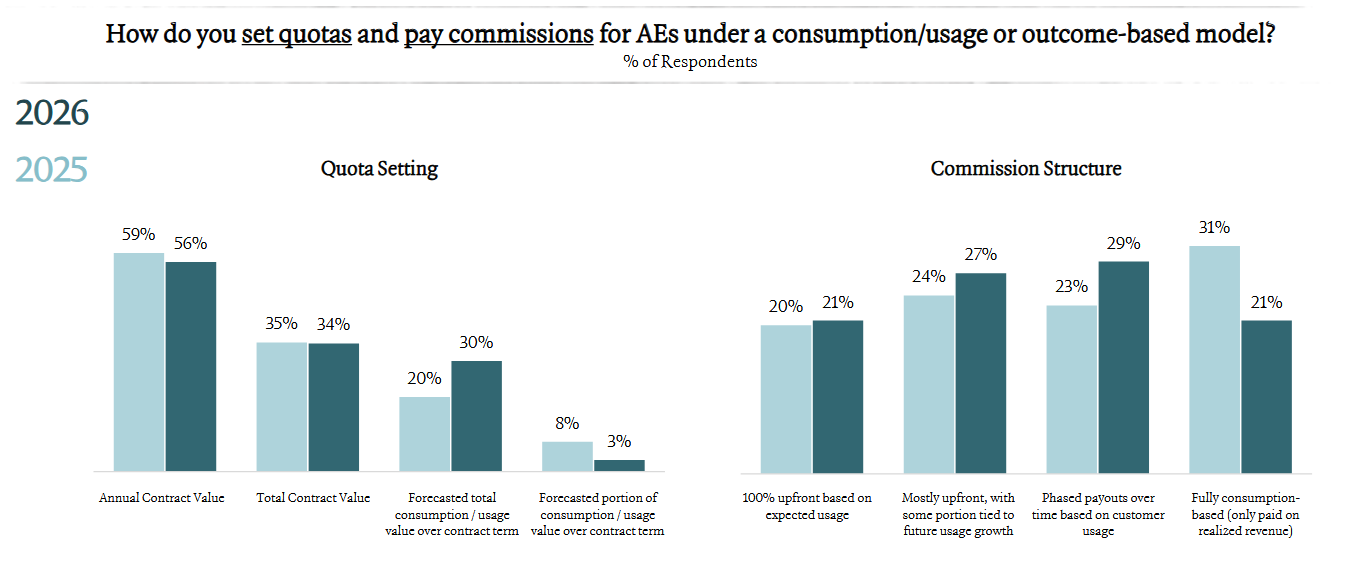

Sales Commissions

There is no single right answer on how to set quotas and pay commissions, but the rise of usage-based pricing likely means changes from what you were previously doing.

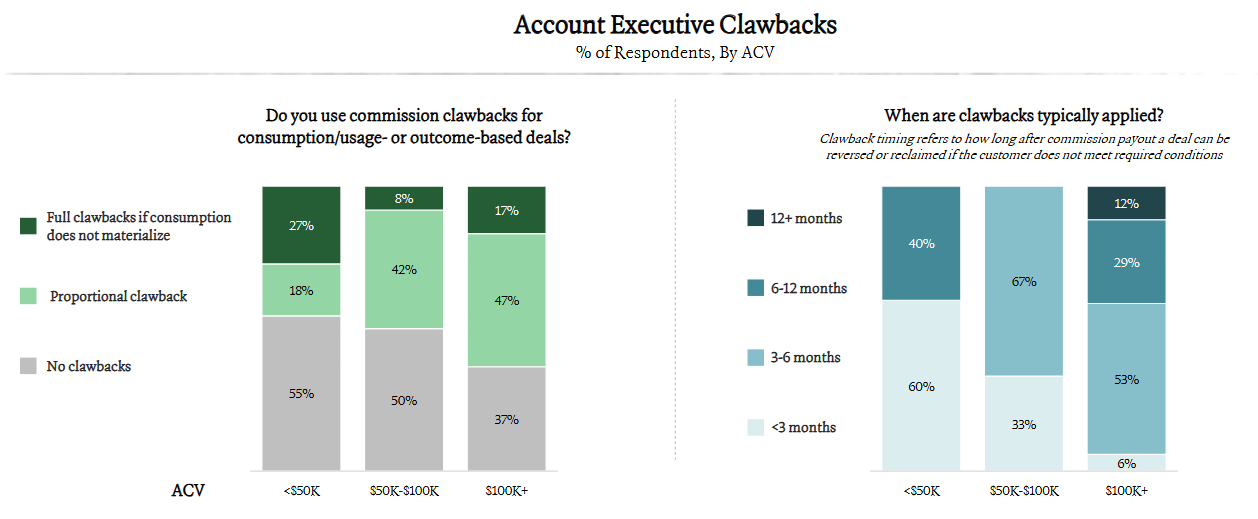

Commission clawbacks are really hard to perform, so I am not surprised most don’t do them. The ideal process is to only pay commissions when the likelihood of a clawback is small, but sometimes that can be hard to balance in usage-based models and you want to pay the rep upfront. I have seen too many cases where the lack of clawbacks creates bad sales rep behaviors…

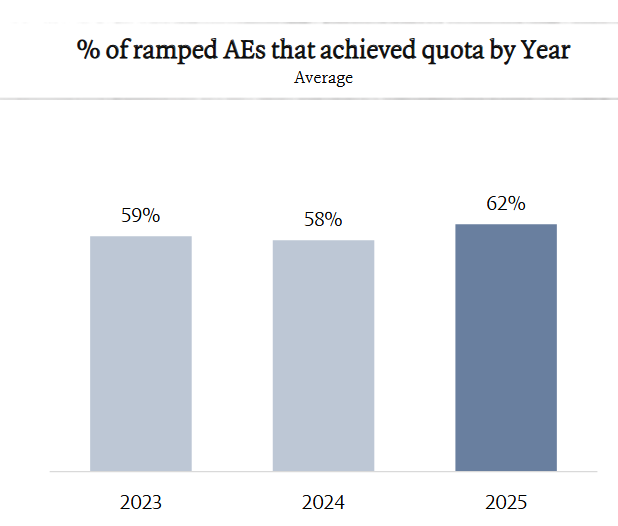

Quota Attainment

Great to see attainment is trending higher. All else being equal, higher quota attainment here means higher GTM efficiency.

But…a lot has changed in GTM efficiency. For example, higher attainment on an AI product with 30% gross margins looks very different than lower attainment on 75% gross margins. Make sure you understand true complete GTM efficiency.

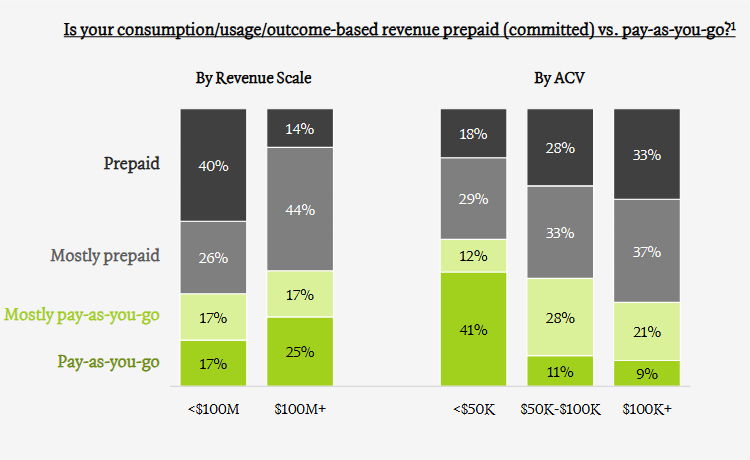

Pricing Model

Interesting data points as usage-based pricing becomes more popular.

It’s so much easier to try new AI products when it’s pay-as-you-go. Competitive pressure likely drives more companies to that model.

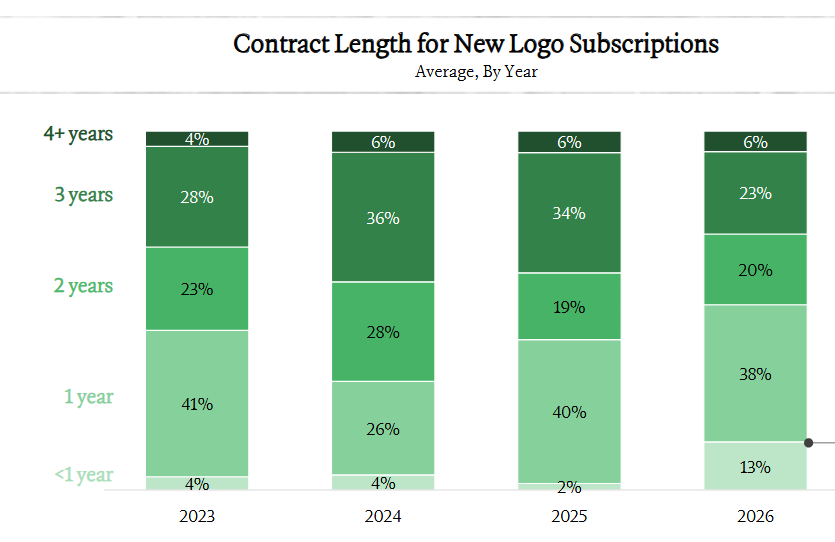

Contract Lengths

There is a combination of things driving shorter contract lengths in 2026:

Uncertainty in software. No one wants to get stuck in a multi-year contract with a tool that becomes irrelevant in 12 months.

Pricing model changes. As more companies shift to usage-based pricing, multi-year deals won’t be as common.

Competitive spaces with unproven ROI. Companies don’t want to overcommit for the new shiny AI thing until value is proven first.

There are only a handful of vendors that I would consider for 2+ year contract terms…Unless a company is mission-critical, the sales reps should not be pushing multi-year deals hard. Let the customer pull you into the conversation if they want it. I dislike SPIFFs for multi-year contracts, especially for SMB deals.

I worry about the competence of any CFO/leader signing up for long duration contracts of non-critical software right now….

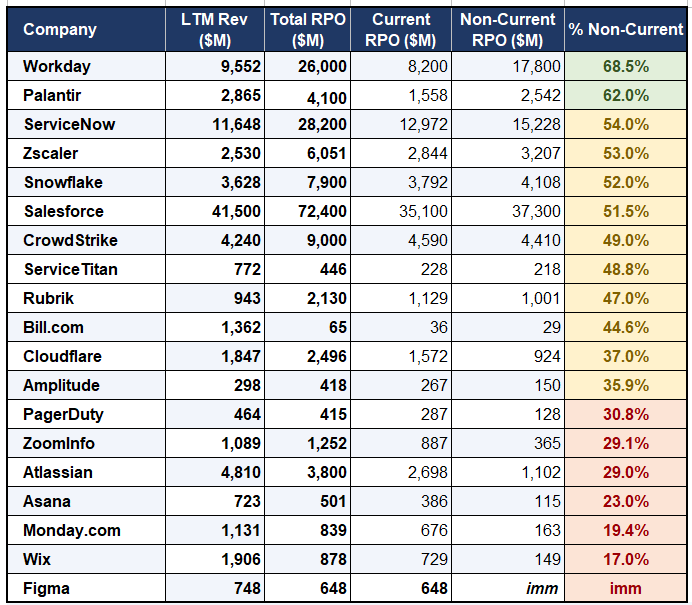

Public companies don’t disclose exact contract lengths but they are required to report RPO (remaining performance obligations), which provides an idea about average contract terms.

“Current RPO” = contracted revenue to be recognized over the next 12 months.

“Non-current RPO” = contracted revenue to be recognized after 12 months

Below is a sample of software company RPOs that I put together. Long-term contracts are quite common and a reason many public companies haven’t really felt the full impact of churn due to AI yet.

Footnotes:

Check out this billing and collection AI agent. If you want to cut costs (everyone needs to) and collect more cash, then you should have an AI agent in accounts receivable. Paraglide is today’s sponsor.

Reply to this email if you want to sponsor OnlyCFO