Are “Insiders” Buying Beaten Down Software Stocks Yet?

The rules behind insider trades and what they actually mean

Today’s Sponsor: Deel

Let Deel handle your international team compliance in 150+ countries, run global payroll, and customize contracts in just a few clicks saving you hours on admin—all within your budget. Get the guide.

“Insider” Bullish Signals

If software stocks are cheap because of the recent SaaSocalypse then lots of “insiders” are probably buying, right?

Wrong. But buying isn’t the only potential positive signal from insiders. Simply not selling (or stopping any selling) can also be a positive indicator.

Executive insider buying is actually pretty rare since a significant amount of their net worth is tied to their equity in the company and they are also regularly granted more equity. So executive insiders buying their stock is kind of like tripling down on your own company.

Insiders might sell their shares for any number of reasons but they buy them for only one: they think the price will rise. — Peter Lynch

I think Peter missed one other important reason why insiders might buy their own shares though: Display confidence in their company.

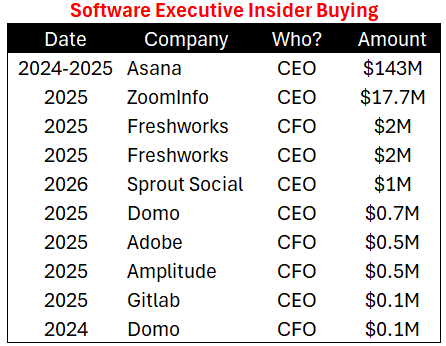

Below are all the executive insiders that have purchased their own stock (out of the 75 software companies that I track):

*ServiceNow CEO announced he is buying $3M of shares, but it hasn’t been disclosed via Form 4 yet.

Here are a few thoughts on these insider buys:

Asana CEO made billions of dollars from Facebook (Meta). He has been selling Meta (a stock price that has been soaring over the past few years) to buy Asana (a stock down 80%+ over the same period). He is one of the most aggressive corporate insider buyers in history (buying $1B+ of Asana stock)….and it has cost him billions of dollars.

Most of this list (like almost all of SaaS) have also seen their stock prices continue to fall after these purchases. Insider buys don’t always equate to better stock performance.

The vast majority of executives are not buying their stock (and actually are selling) and that’s OK. It’s not necessarily a bearish signal.

Very small purchases usually just feel performative (faking confidence).

Insider Stock Reporting

“Insiders” must disclose their equity activity (buys, sells, grants, exercises, etc). Below are considered “insiders”:

Officers (CEO, CFO, COO, etc.)

Board members

10%+ beneficial owners

Insider activity must be reported on Form 4, which must be filed within 2 business days.

Below are some recent examples of insider activity, the rules, and what it may imply about the insider’s thoughts on the company.

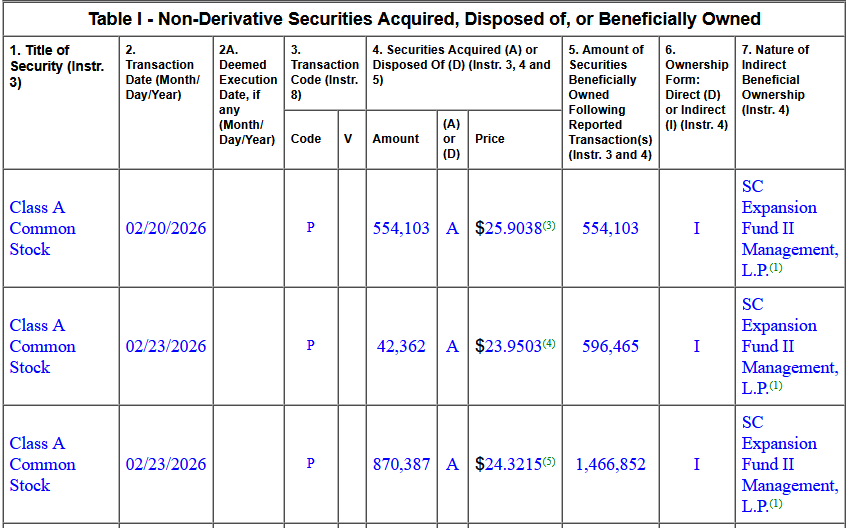

Figma Director Buys $36.5M Shares. Stock Soars

Andrew Reed is a board member of Figma so he is required to disclose all direct and indirect Figma stock activity. Indirect activity would be purchases/sales through his VC firm, Sequoia.

Between February 20th and 23rd, Andrew bought $36.5M stock (through Sequoia). These purchases were reported on Form 4 on February 24th (2 business days later). This was by far Figma’s largest insider purchase. The stock jumped 11% the next day…

10b5-1 Plans: Marc Benioff Sells $1M+ of Stock Every Week

Many retail investors see executive stock sales and think, “Look, even executives are selling after that terrible earnings report”. But often those stock sales are part of scheduled selling from a trading plan set up over a year ago…

A 10b5‑1 plan allows company insiders (executives and directors) to pre-arrange the sale or purchase of their company’s stock on a set schedule. It is commonly used by insiders because it provides them defense against insider trading. For executive insiders, the mandatory waiting period before any trades can execute is the longer of 90 days or the end of the next fiscal quarter (capped at 120 days). For directors who are not officers, the waiting period is 30 days.

While exact details of the 10b5-1 plan aren’t disclosed, companies must file an 8-K when insiders adopt, modify, or terminate a 10b5-1 plan.

Benioff (Salesforce CEO) has been consistently selling stock for $1M+ per week for the past decade…

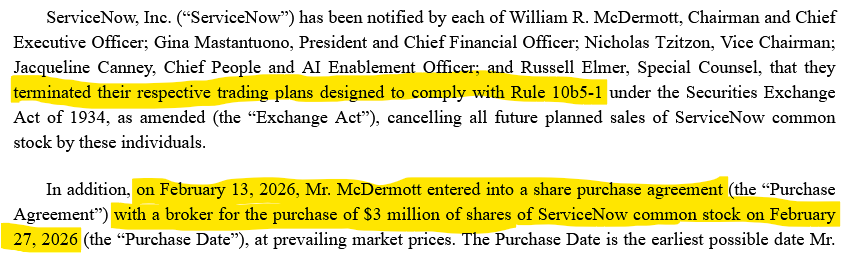

ServiceNow Execs Terminate 10b5-1 Plans

Insider purchases aren’t the only potential bullish signal. Executives canceling future selling under their 10b5-1 plan can be just as meaningful. Terminations must also be disclosed via an 8-K.

For most executives, a significant amount of their net worth is in their stock. Selling under a trading plan is not necessarily a bearish signal. It’s often just executives diversifying and getting some liquidity.

Canceling future selling may be a positive signal though…Why is terminating a selling plan potentially bullish? Because the executive is giving up guaranteed, pre-scheduled liquidity. It’s not easy (or quick) to then resume selling under a 10b5-1 plan because of the cooling-off period and the optics.

On February 17th executives at ServiceNow (CEO, CFO, CPO, AI Officer) all disclosed the cancellation of future selling under their 10b5-1 plans. McDermott (CEO) also announced that he would be buying $3M of stock on February 27th (today).

Why didn’t McDermott buy shares earlier? The stock has fallen a lot in the past several months. Why wait until today?

Because of the “short-swing profit liability” SEC rule.

Because of this rule, companies prohibit executive insiders from taking opposite positions in their company’s stock within a six-month period. i.e. they can’t buy and then sell, or sell and then buy within six months.

McDermott’s last sale was on August 28th (exactly 6 months ago) so February 27th is the earliest he could buy without tripping the rule.

Being forced to wait 6 months from his last sale may work out nicely in his favor though because ServiceNow is down a lot in the past 6 months…

So if executives have a 10b5-1 plan and are regularly selling (many do) then it can take 6+ months for them to actually start buying shares in their company from when they think their stock is cheap and want to buy.

What About Private Company Insiders?

Private company insider buying is even rarer than in public companies. Since there hasn’t been a major liquidity event, most insiders don’t have the cash to do it even if they wanted.

Selling is also less frequent since there’s no active secondary market. In general, the later the company stage, the more comfortable I am with insider selling. Early-stage founder selling at companies with little traction seems like a red flag though, especially when the dollar amounts are large. A few million dollars (<10% stake) for an early-stage founder feels reasonable…gives founders some liquidity so they can focus on building a huge company rather than focusing on more short-term liquidity.

One of the worst examples: the founder of Hopin sold 17% of his stake for $135M+ just two years after launching. Hopin was essentially worthless a few years later…

Final Thoughts

It is important for both employees and investors to understand these rules because it may change what you infer about “insider” intent.

Stronger signals:

Executive buying stock in the open market (especially relatively large)

Executives terminating their 10b5-1 plans, as happened at ServiceNow.

Weaker or noise signals:

Routine sales under a 10b5-1 plan. These were decided at least several months ago for liquidity and say nothing about current sentiment.

Very small open-market buys. These are often performative to signal confidence.

Private Companies:

Large secondary sales at early stage companies can be a negative signal

Footnotes:

Check out this International Hiring Guide. Everything you need to know when building out an international team from my friends at Deel.

Bonus Content:

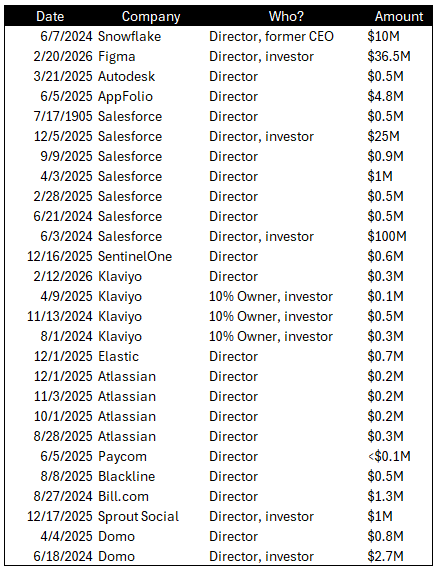

Looking at all other insider buys (Directors and 10%+ owners), they also haven’t been buying much over the last 2 years….Only a few software companies on the list and most are relatively small buys. The bigger buys are because the Directors are buying for their investment firm.

*Disclaimer: This article is for informational purposes only and does not constitute investment, legal, or financial advice.

Cluster buying in beaten-down names is where things start to get interesting.

Not just who buys — but how many insiders step in at the same time.