AI agents in finance are really powerful when they have the right context, controls, and operating environment.

I (OnlyCFO) have been working closely with Brex for over 2 years, and what they’ve built for agentic finance (AF) is incredible. With Brex, agents handle all the tedious stuff, like expense reports, policy enforcement, and month-end close, so your team doesn’t have to. Check out Brex AF!

There is a lot of deception/fraud in “ARR” numbers being reported today. While ARR isn’t governed by formal accounting standards like revenue, there are common practices that should be followed. If not followed, then you are either trying to deceive investors or you don’t understand basic financial stuff. Both are bad…

Let’s start with what “ARR” stands for.

Traditional ARR = Annual Recurring Revenue

2026 ARR = Annual Run-Rate Revenue

With AI, new pricing models, contractual changes, etc. the first “R” in ARR feels a little misleading so I think most companies should think about it as a run-rate amount, but everyone still simplifies it to “ARR”.

This post outlines my views on ARR in an AI world and how you should approach defining it at your company.

There are three primary questions that need to be answered:

What counts as ARR?

How do you report ARR?

How do you calculate ARR?

1. What Counts as ARR

There should be a strong correlation between the following:

Current “ARR”

GAAP revenue, billings, and cash collections over the next 12 months

A greater divergence or risk in that correlation increases the odds that you need either 1) an ARR policy change or 2) separate disclosure of that piece of ARR.

*GAAP (or generally accepted accounting principles) contains the rules that govern how revenue must be recognized (and also lots of other accounting rules)

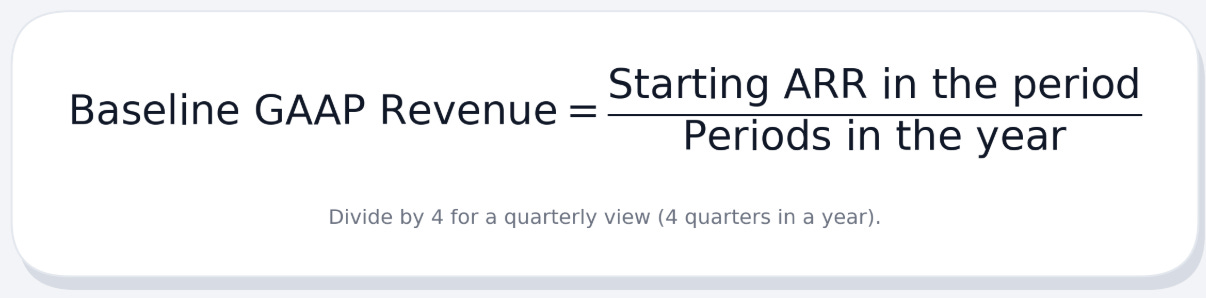

How ARR Should Convert to Billings, Revenue and Cash

Let’s look at a single customer that closed an annual deal on Jan 1st for $1,200. In January there is $1,200 of ARR for that customer. If we billed upfront then we would bill them once for $1,200 and then maybe collect the cash the subsequent month. And then we should recognize $100 per month for the next 12 months.

ARR → Billings → Cash → Revenue

The expectation is that ARR is the baseline of what GAAP revenue should be over the next 12 months. And that should be billed/cash collected for that same amount.

How Being Aggressive on ARR Backfires

Lose investors’ or prospective investors’ trust, obviously.

Metrics all look much better than they are. Maybe good for tricking investors for fundraising, but bad for building long-term trust (which you need). Plus once “ARR” growth slows down (and it will), the metrics are going to look much worse than they should since you pulled ARR forward into earlier periods.

Hiring and spending on inflated metrics. Related to the above. A lot of companies make spending decisions based on ARR-related metrics (new ARR, NRR, GTM efficiency metrics, etc). If those are wrong, then bad decisions will be made.

If ARR is aggressive then churn will be higher as well. If you are aggressive on what gets counted as ARR then you must realize that the only way off the ARR waterfall is churn… High churn numbers are going to make your business look like it’s not durable (AI product is fake or your product is being commoditized by the AI models).

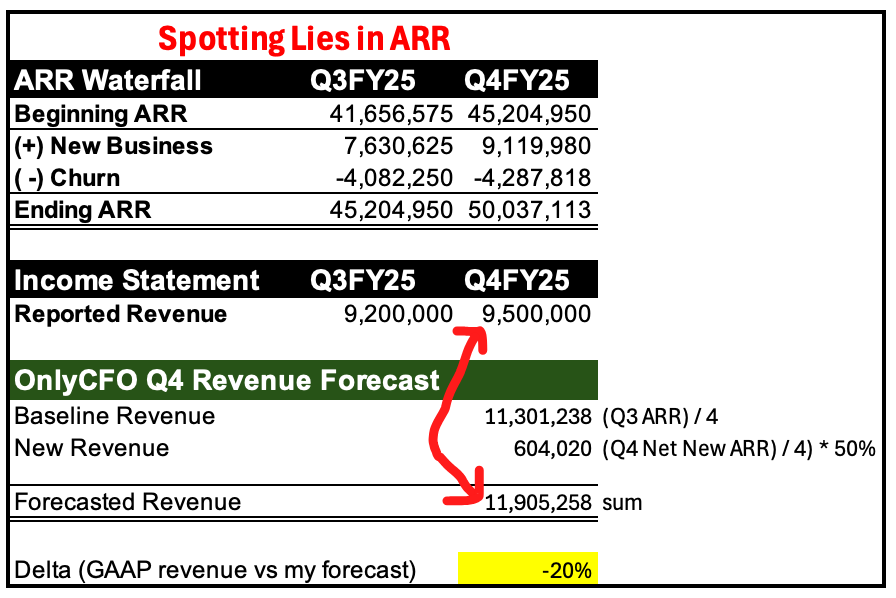

Spotting ARR Lies

If I want to quickly check for ARR deception, then I will compare their ARR number to a simple GAAP revenue estimate that I perform based on ARR.

It won’t be exact, but if the difference is too large and it isn’t clear why, then that will be a major red flag for me.

There are two primary components of my estimate:

Baseline GAAP Revenue: the expected revenue from starting ARR. This is what revenue theoretically should be if there were no changes (no new business, expansion, or churn)

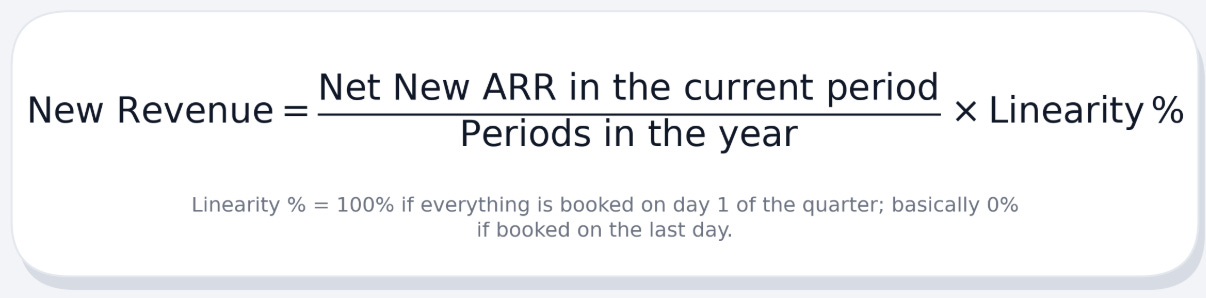

New Revenue: revenue derived from new deals

The example below illustrates how I would estimate revenue from ARR and why it may be a red flag:

If a company provided me the above ARR and revenue numbers and gave me no further context, I would be very skeptical.

There are a lot of reasons that my simple forecast might be materially off, but most of them mean that there are lies/fraud/aggressiveness in ARR definitions.

Linearity/Seasonality

This is a valid reason to have a difference, especially if the company is growing crazy fast relative to its base ARR.

Revenue is recognized over time so if 90% of deals are closed in the last quarter, last month in the quarter, or last day in the month then ARR will diverge from a simple ARR forecast. But you could put some basic assumptions in here as well if you have the detail.

Counting Bad Deals

Every company has some bad deals that should have never been booked, but these can get large if the company is super aggressive. And they will show up in the gap between ARR and revenue.

If a customer invoice (“billings”) isn’t paid, then it shows up in one of two ways on the company’s financials

Reversal of revenue (e.g. CSM says “don’t pay we made mistakes”)

Bad debt expense is recorded (e.g. customer goes out of business)

There are accounting rules that supposedly determine which one should occur based on the scenario, but it can certainly be grey.

So if the company has a lot of #1, then there is going to be a large gap between ARR and revenue. And large revenue reversals likely mean a lot of ARR is fake.

But also…even if ARR lines up with revenue you may have a problem if bad debt expense is massive. It just means the company is burying the problem in expenses because they want revenue to be higher (since investors care more about revenue than some G&A expense)

Cash don’t lie so if ARR isn’t converting to cash then that’s an ARR definition problem.

Gap between ARR Date and Rev Rec Start Date

My general rule is if the time between contract closing and revenue recognition start date is <14 days then it can be ARR on contract close. If >14 days then wait to count the ARR until the revenue recognition start date (which is often the start date of the contract).

I have seen companies start counting ARR immediately when they had a 6-month delay in contract start date because the company wasn’t ready to move forward yet.

That contract will get $0 in revenue, billings, and cash for 6 months…

Ramping Deals

Just count this ARR when the ramp starts. It’s contracted upsells. Why count that upfront before the upsell and related costs kick in? It screws up your metrics.

A lot of companies just average it into ARR (TCV/contracted # of months) but that would recognize too much ARR upfront and not enough at the end of the contract.

Contracted ARR (CARR) vs ARR

This is the “fraud” that many people refer to in regard to ARR at hot new AI companies. They are reporting a very inflated number.

Contracted ARR = future contracted value

If you have a deal that is $50K in year 1 and $150K in year 2, then contracted ARR would be $150K. That is a 3x reality distortion from whatever an investor assumes “ARR” is. And that $100K extra ARR in year 1 won’t convert to revenue or cash.

I think “contracted ARR” can be an interesting data point, but do not mix it with ARR…disclose it completely separately if you want.

“Experimental ARR”

An existing product that has 1+ year contracts is very different than a new product with new technology that is charged month-to-month or on a pure usage basis.

A lot of new AI products have a high churn rate.

Maybe this can get included in the “ARR” bucket, but you should at least report it separately in your ARR waterfall to your board if the characteristics are materially different than the rest of ARR (see reporting section below).

Usage Overages

I only include overages in ARR if I am confident the overages will reoccur for the foreseeable future. Spikes in usage happen and then customers figure out how to control them.

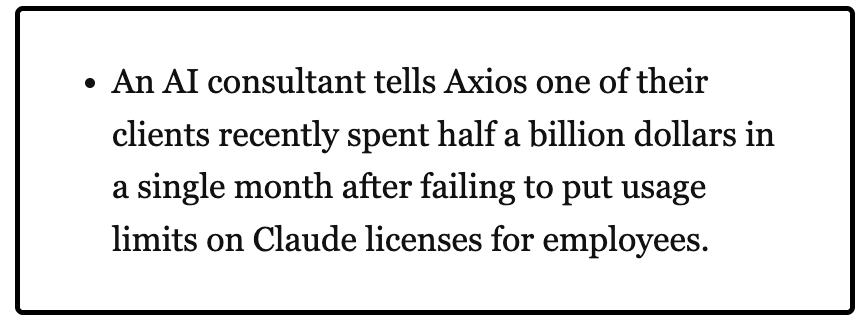

An AI consultant told Axios that one customer accidentally spent $500M in a single month after they forgot to put usage limits in place. That would be…6 billion dollars that Anthropic could have counted as “ARR” 🤣. If $500M is accurate (big if), then certainly the entire thing wasn’t “accidental”. Likely some portion was a min commitment or had a trended growth over the past few months. And then the rest was a one-time spike. That spike certainly won’t reoccur so hopefully Anthropic didn’t book $6B in ARR related to that customer…

Trials/POC

Not ARR. Please don’t count free trials as ARR based on some estimate or contractual amount that the customer has to opt in to at the end of the trial period.

What about paid trials?

This can be somewhat grey in my opinion…If fully paid and you have a history that 90%+ convert then maybe I would be OK with it as long as the ARR amount tied to it is separately disclosed.

Because guess what? You have to be comfortable with the other side of the double-edged sword. Are you willing to add it to ARR and then recognize a high amount of churn soon after?

One-Time Stuff

Not ARR. Duh. Surprising how often people try to sneak some of this stuff into ARR though…

Other Red Flags That Your ARR Definition is Broken

Lots of debookings. If you have a lot of debookings (i.e. you reduce net new ARR in the current period for prior period booked), then you probably have an ARR definition problem.

High churn <6 months after deals close. This usually just means the sales leader bullies the CS leader to count it as churn so it doesn’t impact his/her team’s numbers. If lots of stuff is being marked as churn, expected to churn, and/or is not paying then you got a problem.

Previously reported ARR numbers constantly change. Have seen several times where companies go back and adjust prior ARR numbers and expect me to not notice. They don’t want to count it as churn or debooking in the current period and impact growth rates so they adjust prior period numbers to make it look like the ARR was never recognized.

2. How to Report ARR

How you report ARR is important for decision making and preventing misunderstanding of what ARR is.

My Big Rule: Always define ARR wherever it’s presented. Changes should be infrequent.

In traditional SaaS, we could usually report ARR as one number because the characteristics of all revenue were mostly the same - highly predictable, durable revenue.

But ARR ain’t what it used to be….

Pricing models are much more complicated: lots of flavors of usage-based pricing (pure usage, hybrid, etc), dealing with overages, etc

Contractual terms create more variability - pure usage-based billing, min commitments, etc

Gross margins across products (particularly AI) can vary widely. An 80% SaaS gross margin product obviously has very different unit economics than a 40% AI product.

High retention is often no longer expected. And this is reinforced by shorter contract durations. Old software was 1+ year contracts (often longer) with fixed pricing… This made using ARR as a starting baseline for next year’s billing/revenue easy.

This increased complexity requires more detail in your ARR waterfall. I have never heard a board member or investor complain about too much ARR detail.

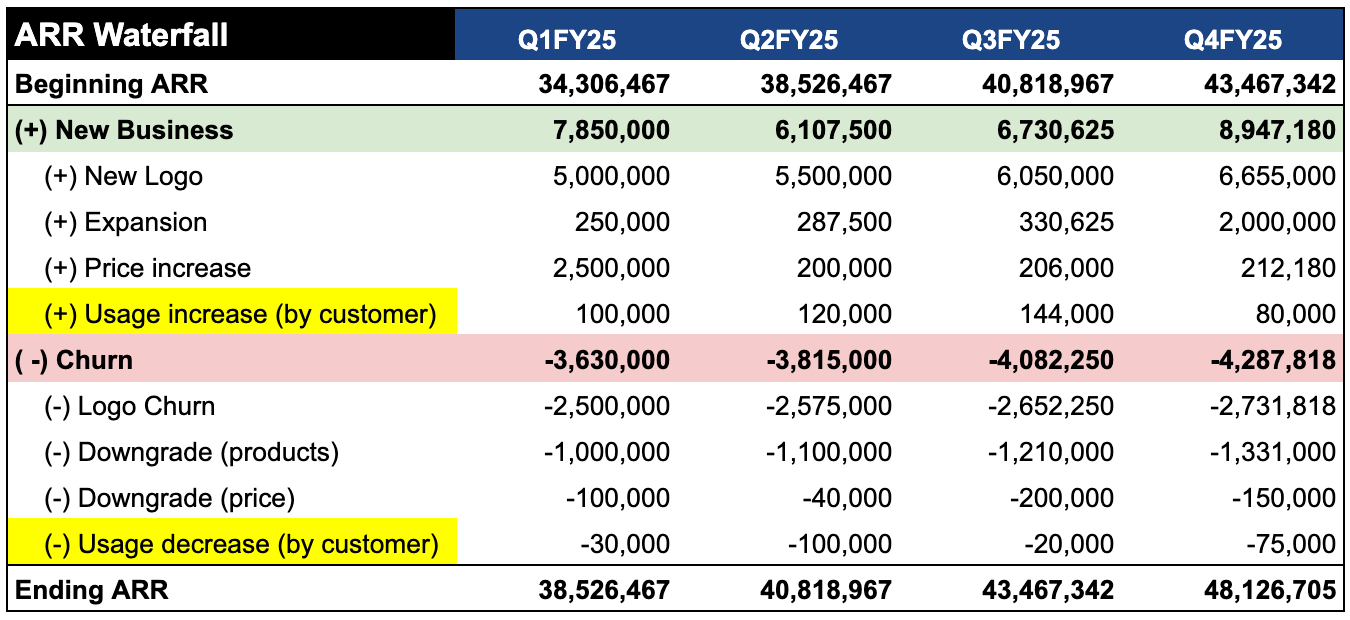

Example: Mostly Seat/Platform Fixed Pricing with Some Usage

You should break out usage-based ARR from contractually fixed so it’s clear how much unpredictability exists in ARR.

The table below breaks out usage-based increases and decreases. You could then further break that out by committed usage vs pure usage-based, by product if gross margins vary wildly, etc.

3. How to Calculate ARR

If you read this far hoping I would tell you exactly how to calculate ARR, you are going to be disappointed.

There are lots of different ARR calculation methodologies that companies may adopt. And often companies will have different calculations depending on the product and how it is priced and contracted. Below are a few common ways.

MRR * 12

Last month’s GAAP revenue * 12

Trailing [X] month average MRR * 12

TCV/contract length x 12

Variation of one of the above less [some portion of variable revenue not expected to reoccur]

I don’t think any of these are necessarily wrong and if you follow the principles I laid out in the previous two steps then you will likely land on a decent ARR calculation.

TLDR: Please Don’t Lie on ARR

If you learned nothing else, then at least do these two things:

Clearly define ARR every time you report it

Be consistent in your definition

I know there is a lot of pressure to show growth right now, but cheating with your numbers is not the way to do it. Be honest and transparent.

If you want to show the ARR potential with trials, future expected ARR with ramping deals, or something like that….great! Make a separate slide that shows those numbers. But make sure you’re clear with what you are presenting.

Footnotes:

See how Agentic Finance can transform your finance department (today’s sponsor is Brex).

Subscribe and share the OnlyCFO newsletter with your teams

Trailing Twelve Month (TTM) revenue is going to become a much more critical measurement than the current bastardization of ARR, especially for investors (IMHO)

Trailing Twelve Month (TTM) revenue is going to become a much more critical measurement than the current bastardization of ARR, especially for investors (IMHO)