Asana vs monday.com | When The Market Gets It Wrong

Why monday.com was always the winner despite Asana’s prior valuation premium

Today’s Sponsor: Xero

Managing your startup's accounting doesn’t have to be complicated. Xero’s cloud-based accounting software allows you to simplify and streamline your business finances. Manage cash flow, track expenses, accept payments online, and much more – all without leaving Xero. Plus, Xero offers unlimited user seats and integrates with over 1000 business apps to ensure you spend less time on accounting admin and more time doing what you do best - growing your business!

Try out Xero today – OnlyCFO readers save 90% on the first 6 months of their Xero subscription using this link.

Asana vs monday.com

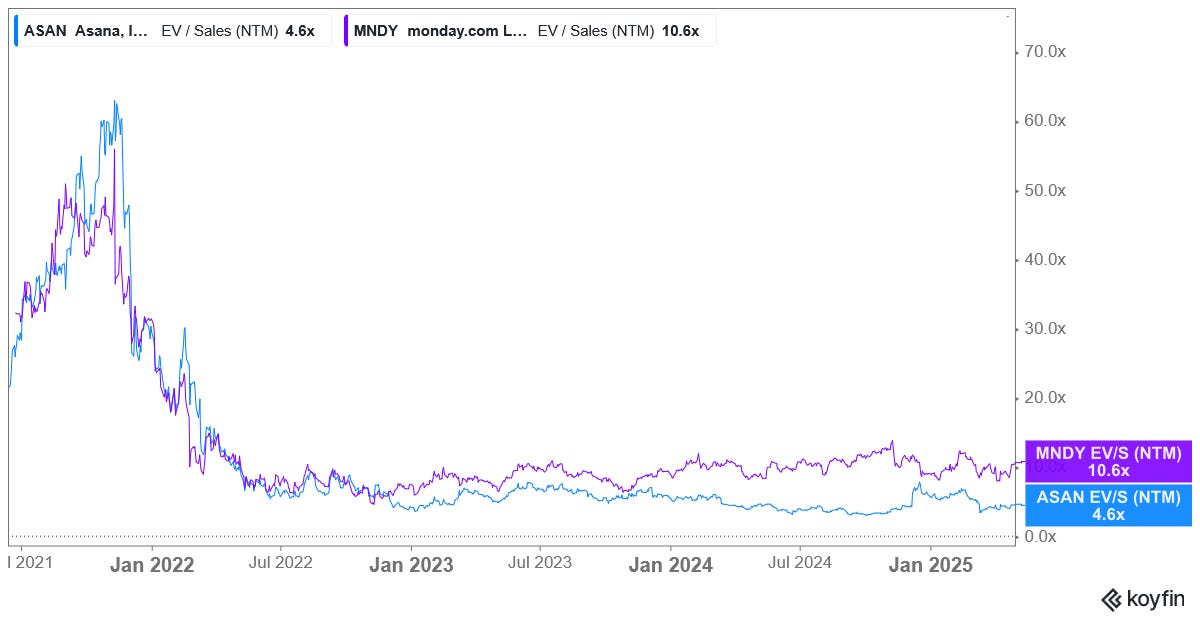

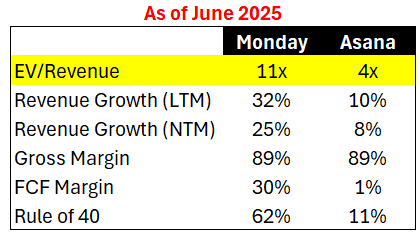

During the good times of 2021, Asana received a higher revenue multiple than monday.com (Asana at 62x vs monday.con at 55x NTM revenue).

Fast forward to today and monday.com’s revenue multiple is more than double that of Asana.

What happened…?

Is Asana undervalued relative to monday.com?

Or is monday.com just the better company?

In this post, I am going to dive into the financial and non-financial differences between these two companies that enabled monday.com to emerge as the winner. And what investors got wrong in 2021.

Blast from the Past

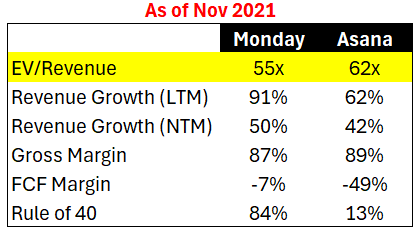

If we go back to November 2021 and look at these two companies’ financials, you would think that the numbers told a story for why Asana received a higher valuation premium than monday.com

Well…you would be wrong.

In retrospect it made no sense…

monday.com had higher revenue growth, burned much less cash and had a MUCH higher Rule of 40 Score than Asana….

So why did Asana trade at a higher multiple?

The short answer is distorted future expectations and hype.

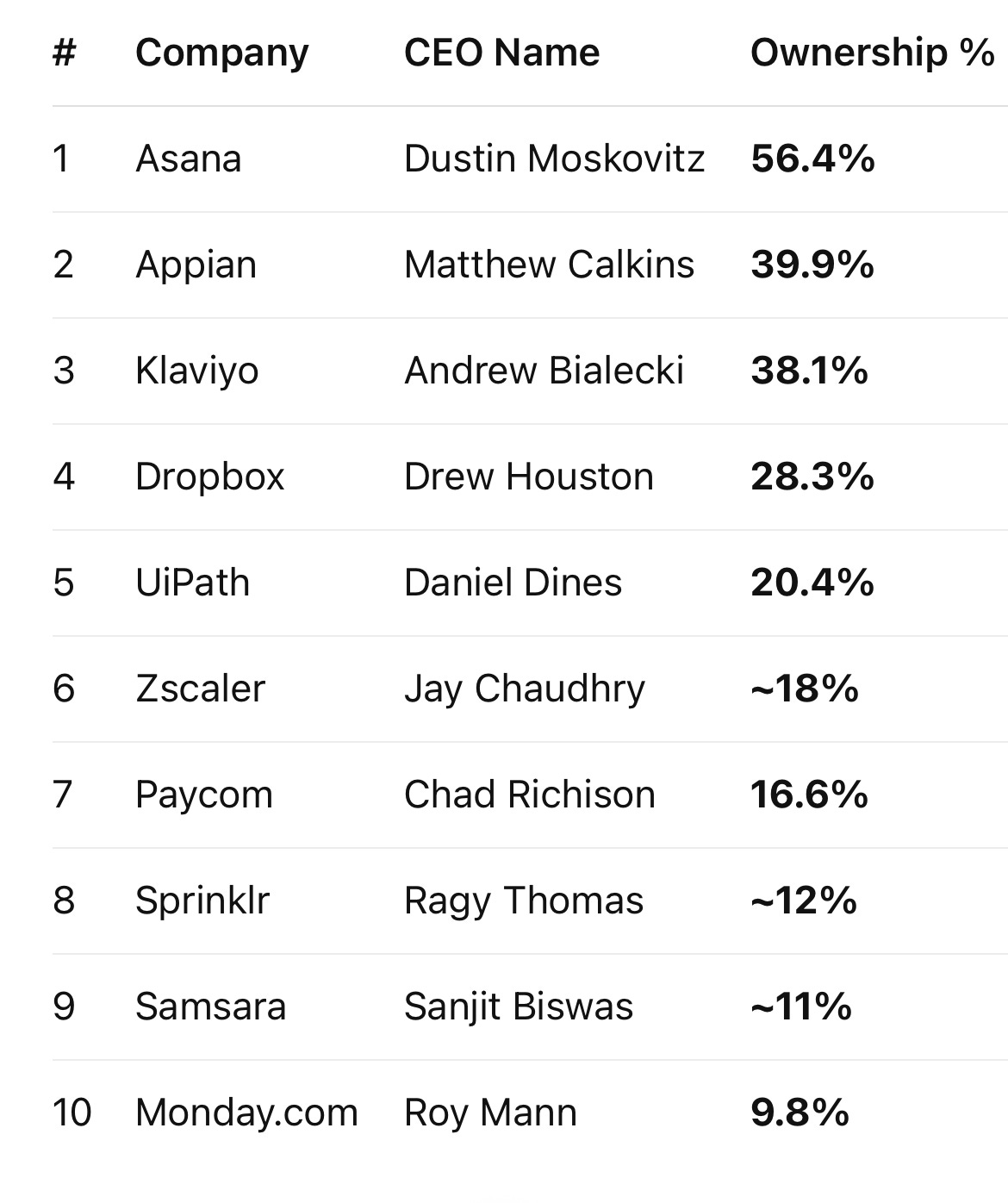

Asana’s CEO is Dustin Moskovitz, a Facebook co-founder. He is a very influential and charismatic CEO. Asana was creating the “future of work” and he was the visionary founder that would lead Asana to be the best.

Moskovitz used the billions of dollars he made from Facebook to buy over $1B of Asana stock since it went public - which bid up Asana’s stock price and gave other investors confidence to buy it as well. Moskovitz is one of the most aggressive corporate insider buyers in history. He has also never sold a share…retail investors took this as a big bullish signal.

Also…Moskovitz owns 56% of Asana 🤯 which is WAY more than any other public cloud CEO (according to ChatGPT below)! This also means the true tradable float is really small for Asana since most of it is owned by a single person who isn’t selling. A small float means the stock price can do weird things in the short-term.

The Wall Street coverage was also very positive for Asana because of the above factors. This created a self-reinforcing loop of hype and investor confidence.

On the other hand, the Co-CEOs of monday.com have literally done nothing. No buys or sells. Is that bad? Not necessarily…

Insider buying (and share buybacks) are done for one of two reasons:

Belief that the shares are undervalued

Desire to show confidence in the stock

My guess is Moskovitz bought a lot of Asana shares for both of these reasons. Plus he had a TON of money so the buys were kinda insignificant to him.

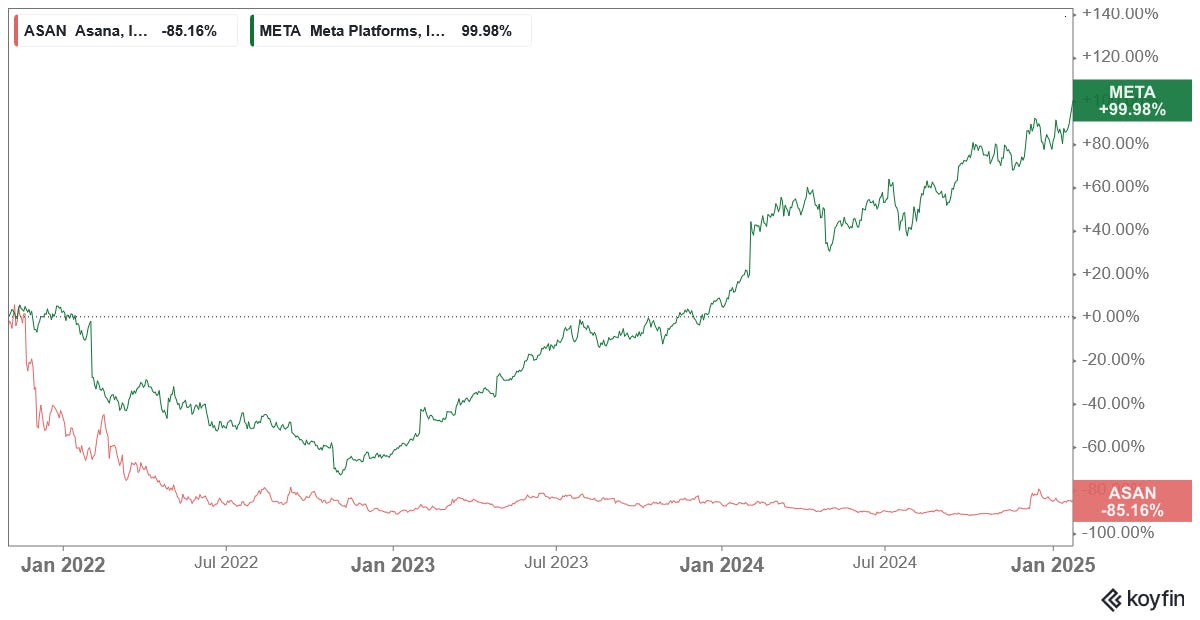

But selling Meta to buy Asana was a REALLY bad financial move…He was selling Meta at low points and continued to buy Asana all the way down. If he just kept his Meta stock, and didn’t buy more Asana, he would probably be at least a few billion richer today…

Either way, Moskovitz’s huge purchases of Asana stock inflated the stock price because of the relative heavy buying and low actual tradable float of Asana given he owns over 50% of the company.

Fast Forward to Today

Eventually the actual financial numbers always win. And in this case, monday.com is clearly the winner today.

monday.com has nearly a 3x higher revenue multiple than Asana — a major shift since 2021.

monday.com’s revenue growth has been MUCH more durable and is now growing 3x faster than Asana.

Despite similar gross margins, Monday.com is radically more efficient than Asana — 30% FCF margins versus 1% at Asana. monday.com seems to have always been more efficient but Asana has completely failed to improve efficiency while revenue growth has come to a sudden halt.

As a result of the above, monday.com’s Rule of 40 Score is more than 5x that of Asana!

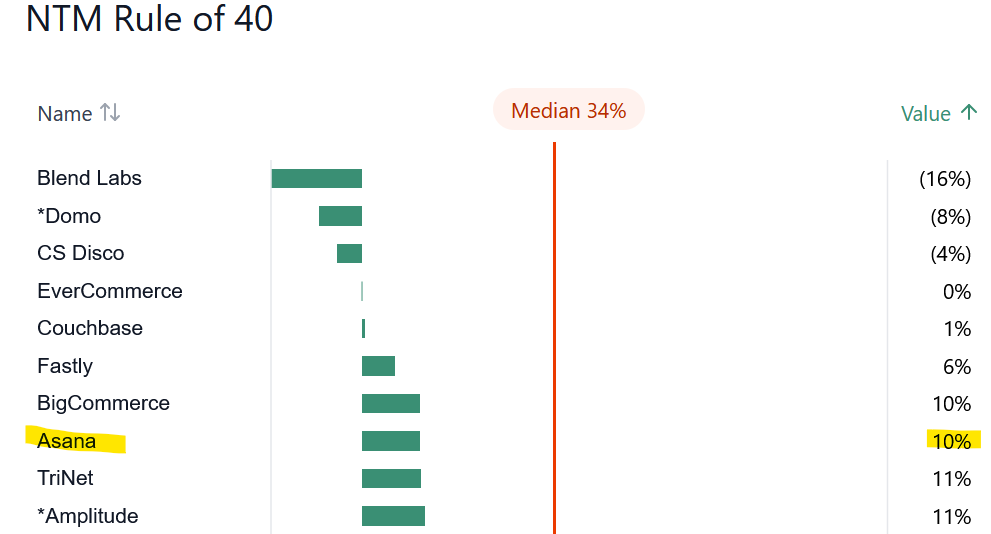

Asana’s Rule of 40 Score is the 8th worst of all public cloud companies…

**Quick Plug: Get my financial health dashboard template and keep everyone honest on the financial health of the business so you can make the right decision timely.

Is Asana Broken?

I don’t trust a software company that is barely growing and still can’t turn much of a profit. And that is Asana today…

Besides the core financials above, there are several things working against Asana:

Founder/CEO Resigning

In March 2025, Moskovitz announced his intention to resign and he is currently looking for his replacement. So a major reason why Asana received a valuation premium is going away…

AI hurting Asana?

Asana is failing to produce AI benefits for revenue growth. In fact…AI seems to be hurting Asana. Which is a bad place to be in 2025.

Customer Churn Problem

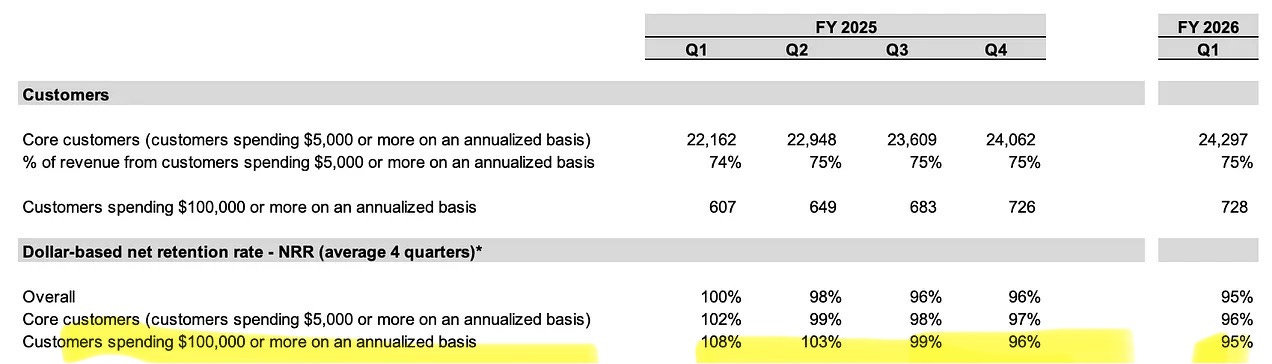

Asana’s customer retention (NRR) continues to fall.

Below is what Asana shared in their recent investor deck. Asana’s previous bright star NRR with large customers has fallen from 108% to just 95% in only 5 quarters. That is bad…

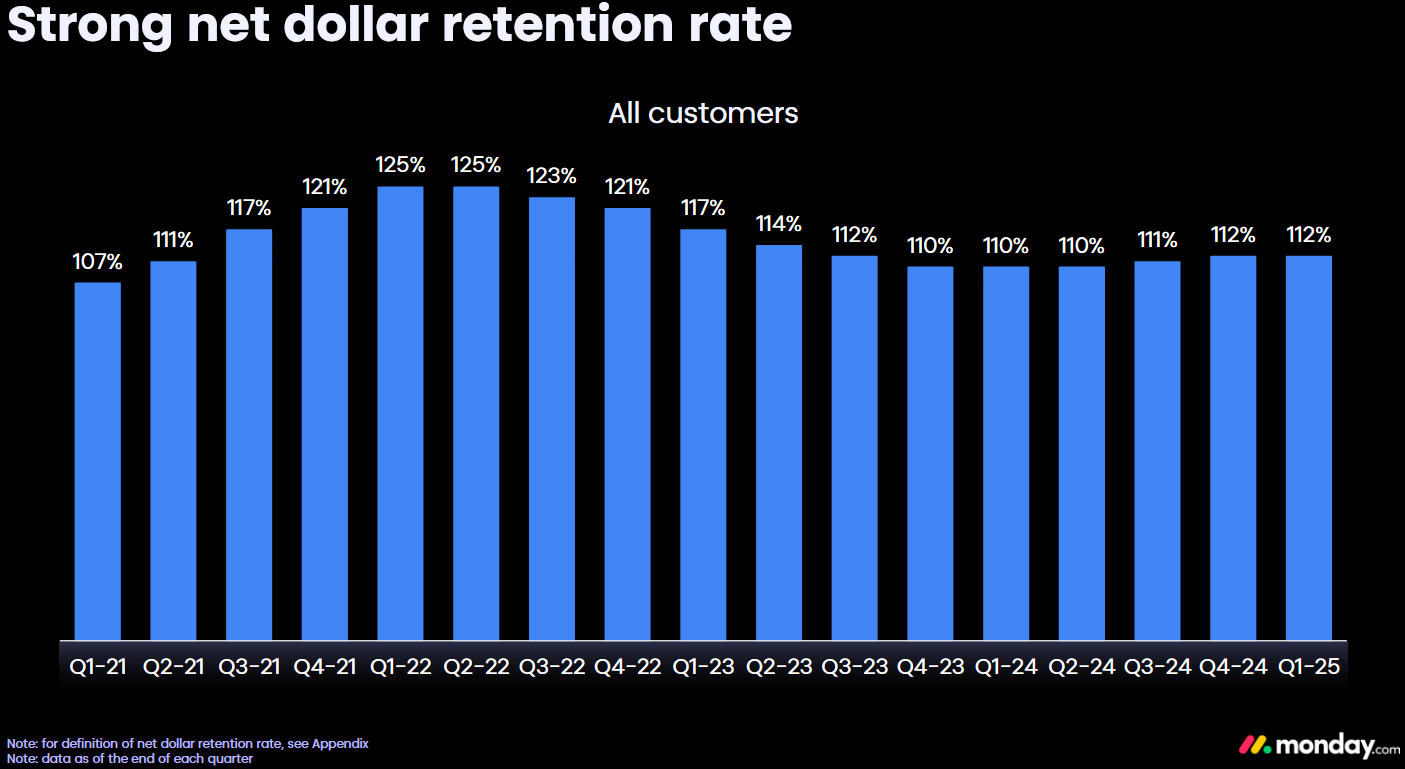

monday.com on the other hand…reported 112% NRR on their $50K+ customers, which improved since last quarter by 2 percentage points.

This means monday.com is getting an extra 18 percentage points of revenue growth compared to Asana just on their ability to better retain and expand customers. Which also helps explain the major efficiency gap between these two companies.

That is 18% of additional growth that might cost <20% of new logo growth. It is REALLY hard to be efficient with low NRR (especially when selling to the enterprise).

GTM Efficiency

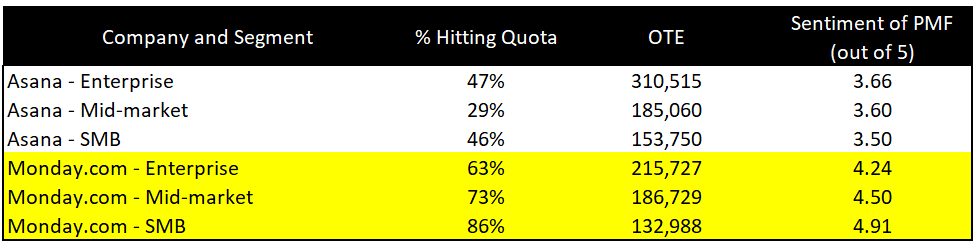

The below data comes from RepVue, which is a company that surveys sales reps at cloud companies.

The big red flag here is the difference in the percentage of reps hitting quota — monday.com has a ton more reps hitting quota. Which makes Asana’s already higher OTE (particularly in the enterprise segment) significantly more expensive and less efficient.

RepVue also tracks sales rep sentiment about product market-fit (PMF). monday.com reps are much more bullish on their product than Asana as you can see above…

Location Matters

Asana is based in San Francisco while monday.com is based in Israel. This created two important differences:

There are significant payroll differences in Israel vs San Francisco (probably 2x+ the cost in SF vs Israel)

monday.com attracted a much more diverse customer base than Asana — both location and industry. monday.com has A LOT more non-tech customers (~70%) which meant a lot more resilient and durable revenue.

San Francisco is the center of tech, but there are benefits to companies who are able to succeed on the outside.

Final Thoughts

While Asana isn’t necessarily doomed, I think there is A LOT to fix. They need to hire a new CEO quickly that can really get growth accelerating again.

Don’t trust a software company that is growing slowly and still can’t be meaningfully profitable.

monday.com, on the other hand, has executed at another level. They have dramatically improved efficiency while keeping revenue growth relatively high.

monday.com continues to have a top 5 NTM revenue growth and Rule of 40 Score but have the 15th highest revenue multiple. Why? Because investors keep thinking their revenue/margins are less durable. But…so far monday.com keeps executing and proving investors wrong.

Footnotes:

Want to see the best ARR guides/benchmarks? I am building a website called CFOPilot that will have all of them at your fingertips…Get on the list to receive updates on all the stuff being added

Get 90% on the first 6 months of their Xero subscription using this link.

Check out OnlyExperts to find offshore accounting resources. They have some amazing talent for 20% the cost of a U.S. hire

Monday is just a better product than Asana. Asana is just project and task management. Monday can do just about anything, and has grown to doing service management, CRM, dev management, and continues to make new use cases.

I really can’t think of a reason to buy Asana over Monday in the real world, and the rest of the market is figuring that out as well.

Asana is my favorite when it comes to managing my personal life's to dos.