Cloud Unit Economics in 2024

What operators and investors need to understand to be successful in 2024

Today’s newsletter is brought to you by Brex.

AI is everywhere in finance, but CFOs rarely reveal their playbook: how they secured funding, chose vendors, and maximized ROI. The CFO’s guide to building an AI strategy tells you how to plan and budget for AI today, the key evaluation criteria, and strategies to reap the AI benefits faster.

Cloud Unit Economics

A company’s valuation is ultimately determined by a company’s future cash flow potential, which hinges on its unit economics. Understanding unit economics will drive better decisions for both operators and investors. Too many people become blinded by short-hand valuation multiples or metrics that they don’t understand how will impact profit potential.

And 2024 is just a different, so people should focus on today versus what was true in the past. The fundamentals are the same though and that’s where people should focus.

I agree with Jason…

The stories of the good times of ZIRP and 2021 aren’t super useful today (even if fun to talk about). Let’s sum up the countless blogs and podcasts about peak ZIRP era:

We over rotated on growth and forgot about efficiency

We burned too much

Capital was too abundant

Valuations were too high

That’s really all you need to know…

So what should companies do today?

Understand unit economics and focus on balancing high growth with efficiency.

The reason cloud companies can get high valuation multiples is because they have been able to scale quickly (high growth) and print money at scale (high profit margins). If company leaders and investors truly understand unit economics then they will know what they need to do when the math changes.

Whether the VC money valve gets shut off, AI changes the economics, or anything else….if you understand the basics then you will know how to react to changing situations.

Unit Economics Foundation

What has made high-growth cloud companies great targets for VC money is that they usually had to front load a lot of cost to build the product and acquire new customers. And then these companies would continue to lose money for a long time if they were growing fast and then only as growth slowed would they maybe get to breakeven. So they needed VC money to fund the cash burning period of high growth.

When people talk about “unit economics” in software they are typically referring to how adding an additional customer or $1 of revenue impacts the financials over the life of the customer.

Unit economics answers the following: How much money can a company make from selling its product to a customer.

Acquiring Customers

The Customer Acquisition Cost (CAC) Payback Period shows how long it takes for a company to recoup its customer acquisition costs (sales & marketing spend).

There are plenty of potential nuances with how you calculate the payback period (lagging S&M costs, including expansion, including churn), but that is not the purpose of this post. Just understand it is supposed to represent how long it takes to breakeven on the sales & marketing (S&M) costs it took to acquire a customer.

Below is a great chart from Lenny Rachitsky on historical rules-of-thumb for good payback periods.

I say “historical” because you need to decide if these should still be true today and if they are true for your company — “can AI make you more efficient?”, “does less VC money mean you need to do things differently?”, etc

Here are some things you should understand about payback period:

Payback period is not an efficiency metric. Rather it’s a risk metric that shows how long it takes to get your money back (h/t Dave Kellogg for driving home this point). The unit economics can be terrible on a company with a 6 month payback period if customers typically churn in month 7.

Longer payback periods are acceptable as a company moves up market to the enterprise segment because those companies typically stay customers longer and have bigger wallets to expand. BUT…the proliferation of SaaS and now AI will make switching SaaS tools much easier so long CAC paybacks will become much more dangerous.

Payment terms can have a significant impact on the cash flow trough discussed below. While you shouldn’t change the CAC payback period calculation based on payment terms, it does impact cash runway planning.

Payback period only shows time to breakeven on sales & marketing costs. It doesn’t speak to research & development (R&D) or general & administrative (G&A). For companies heavily investing in R&D it will take even longer to get to cash flow breakeven.

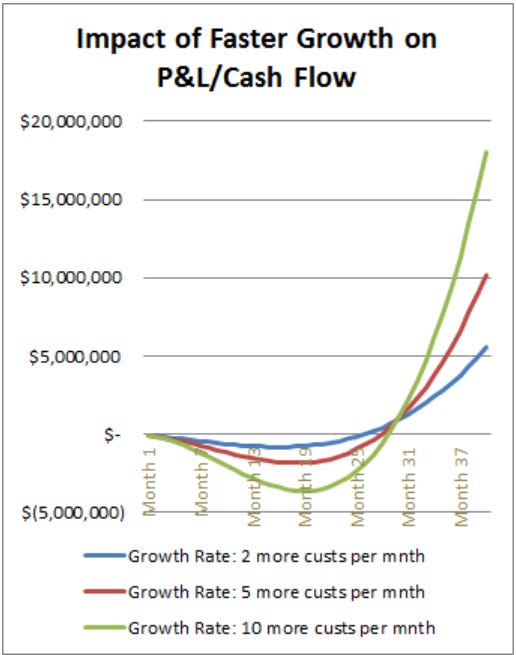

The Cash Flow Trough

The CAC payback period explains why fast growing SaaS companies are burning large amounts of cash and the cash flow trough illustrates how this impacts cash burn.

I first saw the visualization of the SaaS cash flow trough from David Skok. The faster a company is growing the larger the cash flow trough because of the individual customer CAC payback periods being stacked on top of each other faster than profits accumulate from customers on the other side of the cash trough.

But as growth rates start to slow those companies see faster and larger cash inflows. The trick is balancing the cash flow trough with a company’s cash runway and fundraising timing.

If the unit economics are great then companies will want to hit the gas and grab as many customers as possible. However, this means the cash flow trough gets deeper and the company will burn lots of money initially (in hopes that lots more money comes later). Companies need to carefully manage their cash position and timing for raising more money.

The visualization above shows why good unit economics is critical. If the unit economics are terrible then you will never get out of the cash flow trough…

The Burn Multiple

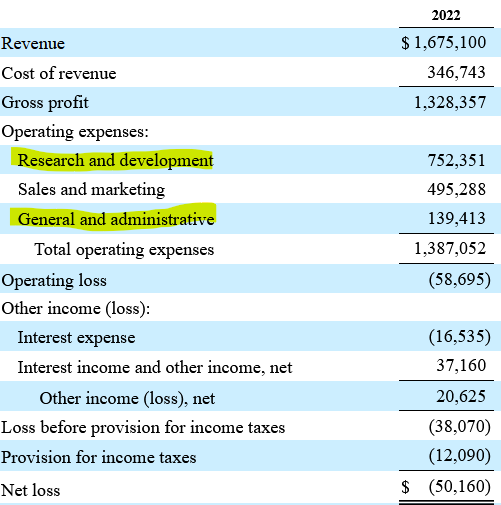

There are more costs to recoup then just S&M. Using the example income statement below there are three things covered in CAC payback:

Gross profit, which is made up of:

Revenue

Cost of revenue

Sales & marketing (S&M)

But after S&M is recouped, the aggregate profits must also recoup costs from the below items before a company is cash flow positive:

Research & development (R&D)

General & administrative (G&A)

If the unit economics are bad, then you won’t generate enough cash flow from customers to recoup the investments in these areas.

This leads to another important metric: The Burn Multiple. The burn multiple shows how much cash a company burns to generate $1 of net new annual recurring revenue (ARR).

The burn multiple is important because companies can’t easily manipulate it or hide anything since it is includes all cash burn. Many companies (particularly private ones) play accounting games to move costs around to make their metrics that investors care about better - dumping expenses in G&A or R&D, capitalizing too much, etc. But it is much harder to hide stuff with the burn multiple.

Good/bad burn multiples are a function of:

growth rates

stage of company

company specific circumstances (like complexity of product)

Below is a 2024 survey from ICONIQ portfolio companies and their burn multiples by ARR stage. As ARR increases the burn multiple should decrease because growth rates are slower (meaning more customers are exiting the cash flow trough and driving profits) and more operating leverage is being built. Around $150M+ in ARR companies should stop talking about the burn multiple because they should be getting close to breakeven and burn multiples loses meaning…

While the burn multiple can be a great high-level overview of capital efficiency, it doesn’t tell you how good the unit economics are. Even if a company has a great burn multiple the business can still be garbage if the unit economics are bad (burning only a little money isn’t good if you will always burn a little money :)

Eventually the ARR per employee must surpass the expenses per employee for a company to be profitable. And most companies have been making improvements in this metric over the last several years.

The magic of SaaS is that if customers renew (high retention rate) then the marginal cost in the outer years is relatively small and you therefore have incredible profits each additional year you keep customers, which is the real power of SaaS unit economics.

Unit Economic Metrics

Up until this point I have covered why SaaS companies lose money for so long and provided some metrics that may indirectly speak to unit economics.

Unit economics is like an income statement at the individual customer level. In theory one of the best ways to understand the unit economics is to look at the LTV/CAC ratio. The LTV/CAC ratio is like a discounted cash flow (DCF) model, in theory it is perfect but there are so many inputs/guesses that it can be fairly meaningless (especially for early stage companies).

But the idea behind LTV/CAC ratio is still important to understand:

Lifetime value of a customer (LTV)

Customer acquisition Cost (CAC)

I have already defined CAC above. LTV is defined below and represents the total money brought in from the customer over their lifetime after reducing for the direct ongoing costs to manage the software (reflected below by gross margin %).

Adjusting LTV with gross margin % standardizes LTV amongst cloud companies that have a wide range of gross margin percentages — making comparisons easier.

You can now use LTV to tell how much dollars a customer provides to pay down operating expenses: R&D, S&M, and G&A.

The direct and incremental costs associated with acquiring a customer is S&M (or CAC) while R&D and G&A should decrease as a % of revenue as companies build operating leverage.

Common rule of thumb: A good LTV/CAC >= 3

First off, an LTV/CAC ratio of 3 is actually kind of a low bar. Most great companies are something closer to >6.

Example: A company sold a deal with an LTV of $120K and CAC of $40K — LTV/CAC of 3. This means there is $80K left over to pay for the R&D and G&A costs and then hopefully lots leftover for the company in actual profits.

Context is critical with all metrics. What makes a good LTV/CAC ratio also depends on the other expenses. For example, product-led growth (PLG) companies tend to spend a lot more on R&D. Theoretically, CAC could be low because a company is spending a crazy high amount in R&D. In this case a high LTV/CAC ratio is not as attractive because there is extra R&D costs to pay down before profits accrue to the company.

Expansion

Another aspect of a customer’s LTV is expansion opportunities that happen over the customer life. Companies that can expand a customer over time increase the actual LTV. This is typically not reflected in the LTV/CAC ratio so companies with higher expansion potential should be looked at more favorably. Expansion potential is reflected in a company’s net revenue retention (NRR) metric. NRR is similar to compound interest…

One of the reason expansion revenue is so great is that it has a lower cost than new business revenue so it provides more dollars to the bottom line. So businesses with more expansion opportunity will have much more favorable unit economics. Based on a KeyBanc survey, expansion dollars are about 1/3rd the cost of new business.

Word of Caution Using LTV

LTV:CAC is in theory a fantastic metric to understand unit economics but it comes with one major flaw…churn assumptions. To get to the customer life we use 1/churn rate. So if a company has an annual churn rate of 10% then there is an assumed 10 year customer life.

Very early stage companies have no idea what their actual customer life will be so anything is just a wild guess. Also, a lot of companies are still using benchmarks and churn history from the last decade of boom times. The future likely looks different — especially with increasing competition, generative AI, etc. Most companies should be more conservative with LTV calculations.

Stacking S-Curves

The idea of “stacking S-curves” is to find the next lever for growth before the current one flattens and falls.

Companies in the process of stacking an S-curve will likely require a sacrifice for a time of the unit economics and cash burn. But if successful then it will generate higher and faster cash flows in the future. If unsuccessful though then the rest of the business with good unit economics will subsidize the bad one until it improves or is killed. This is why unit economics should be segmented.

Final Thoughts

Companies are ultimately valued by their future cash flows. Understanding a company’s unit economics is critical in determining how profitable a company can eventually become at scale.

The cloud dream is that at scale you can have 25%+ free cash flow margins and then sustain that free cash flow level over a long period of time. This is why SaaS companies can have very high valuations relative to their current revenue levels — fast growth combined with incredibly high future cash flows.

Understanding unit economics can help a company understand how profitable it can become and it also helps inform important decisions to drive more growth/profits:

Helping discover good/bad investments

Guide pricing strategy /optimizations

Discover high ROI sales channels

Determine best performing customer segments, products, geography, etc.

CEO and operators must understand unit economics so they can make better long-term decisions based on what matters - maximizing future cash flow potential.

Footnotes:

IDC says AI can bring you more cash flow predictability. check out the report courtesy of Brex (today's sponsor)

Reply to this email if you need a fractional CFO and/or bookkeeping for your company. I partner with a great group.

Check out OnlyExperts for to find offshore accounting resources. They have some amazing talent for 20% the cost of a U.S. hire.

Best post yet! The one metric I would have added is R&D payback as a way of unpacking burn multiples and whether all that money going into R&D is generating a positive impact to the business.