Confluent's Valuation Plunge | A Cautionary Tale for High-Growth Companies

Lessons from Confluent's most recent earnings release

Confluent reported earnings after hours on November 1st and then saw its stock price drop nearly 50% the next day! While the stock recovered a bit and was “only” down 42% by end of day, a single day drop this large should be unusual for a software company that should be fairly predictable.

However, when a high-growth stock rapidly decelerates to the moderate-growth bucket and is still unprofitable both growth and value investors no longer want it. So there is no one to catch it from falling.

Confluent is a great company and has (and will continue to have) a ton of success. If a company like Confluent trades at below average revenue multiples, then there are many other company valuations waiting to get chopped and TONS of private companies that also look incredibly expensive.

Outline:

Making of a successful quarter (free)

What happened to Confluent (free)

Reaction to Confluent’s earnings (paid)

Implications for other companies (paid)

Thoughts on Confluent (paid)

Making of a successful quarter

A successful quarter for a public (and a private company) is made up of two main parts:

Beating current quarter consensus estimates

Raising forecasts above estimates

This is referred to as a “beat and raise”.

The estimates are created by the equity research analysts that cover the stock. The consensus estimate is the average of these analyst estimates. The expectation is that companies will usually beat these estimates because companies guide analysts to the lower end of their internal projections so they can be confident in beating it. Private companies do a similar thing with their boards — create a plan that they are 90% confident they can beat.

The main metrics that make up the “beat and raise” are:

Revenue

Profitability

There are also a lot of other software metrics that help investors understand revenue growth and profitability —helping understand both current results and long-term potential. Many metrics from the actual results can help inform the forecas. So even if future guidance wasn’t provided, investors can look at other leading indicators of future revenue growth and profitability from current results.

You can not have a successful quarter without both a beat and a raise of revenue and profitability. But the “raise” (forecast) part has an outsized impact to stock price performance because of the importance of future revenue and profitability for valuations.

If high-growth companies turn into moderate/slow growers too soon then the company lifetime cash flow generation potential becomes significantly smaller…and therefore their valuation should get slashed.

What happened to Confluent?

Confluent must have reported a disastrous earnings report to see its valuation almost cut in half, right?

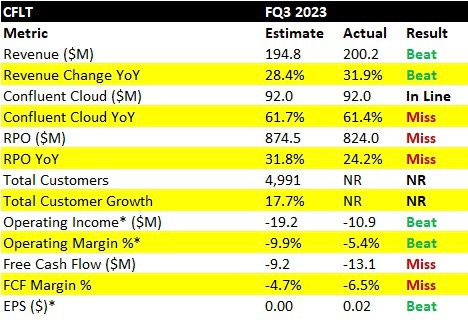

Beating Q3 Results

At first glance, Q3 results were actually pretty good. Confluent exceeded expectations on revenue (3% beat) and had a slight beat on earning per share (EPS), which measures profitability. Looking at just these, Confluent “beat” current quarter expectations, but if you look at the other metrics it was a bit mixed.

FCF margin:

Confluent missed FCF margin expectations by $4M (or 2 percentage points).

FCF is another measure of profitability, similar to EPS. The difference between EPS and FCF is that FCF is based on cash while EPS is based on accounting rules. There are pros and cons to looking at both of these metrics, but missing on one hurts investor confidence in long-term profitability potential since either one can be manipulated. One reason EPS might beat expectations while FCF margin misses is due to weaker than expected customer billings and RPO (see below).

Remaining performance obligations (RPO):

Confluent missed RPO expectations by $50M (or 7 percentage points). This is the bigger concern and directly impacts analyst future estimates.

RPO is a required accounting disclosure that captures a revenue backlog metrics: RPO is calculated by:

Customer invoices

PLUS future contractual amounts to be invoiced

LESS revenue recognized.

in other words RPO is the total amount contracted with customers less revenue recognized. RPO is driven by 1) amount of the contract bookings and 2) contract length.

Investors look at RPO as a leading indicator for revenue growth because it can tell you how a company’s customers contracts are growing, which is more forward looking than revenue accounting. I don’t love RPO as a metric though because of all the things that could cause it to be misleading but it can be an OK high-level indicator. Changes in contract length, consumption patterns, seasonality, pricing model changes, etc can cause RPO to be misleading.

For Confluent, the RPO is impacted by 1) missed bookings, 2) lower contract lengths as customers are more cautious about long-term commitments and 3) smaller contract sizes as they focus more on the consumption model and just landing the deal.

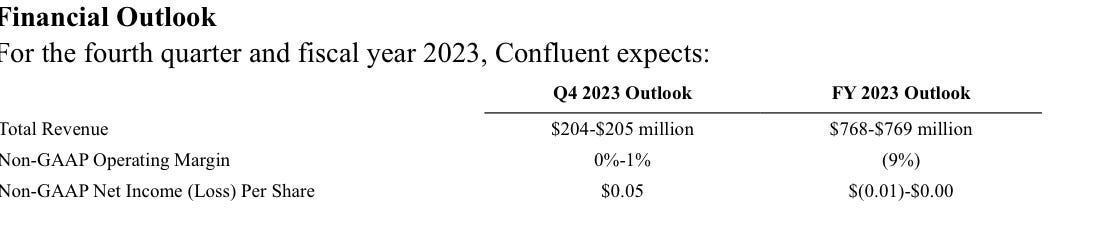

Missed Guidance Expectations

Confluent missed analyst expectations on its guidance. Company guidance is typically provided in their 8-K filings of earnings with additional information sometimes provided on the earnings call.

Q4 Revenue:

Confluent provided guidance of $204.5 at the midpoint while consensus estimates we’re at $212.3M (a 3.7% miss). This represents 21% - 22% year-over-year growth — down fairly significantly from the 32% growth in Q3.

Q4 Earnings Per Share (EPS)

Earnings per share guidance is in line with previous analyst expectations for Q4.

Reaction to Confluent’s Earnings

Keep reading with a 7-day free trial

Subscribe to OnlyCFO's Newsletter to keep reading this post and get 7 days of free access to the full post archives.