Drivers of Valuation

Discounted cash flow models are perfect but also always wrong

👋 Hey, welcome to a subscriber-only edition of my newsletter. Each week I cover topics about the software industry to help operators and investors. My focus is on finance, accounting, and operations of software companies.

A discounted cash flow (DCF) is theoretically a perfect way to value a company, but it is always wrong because of all the assumptions used to derive cash inflows and outflows. Most software companies (and investors) can’t accurately predict 2 years into the future so how are investors supposed to accurately predict 10+ years into the future for a DCF?

In the Theory of Investment Value, written over 50 years ago, John Burr Williams set forth the equation for value, which we condense here: The value of any stock, bond or business today is determined by the cash inflows and outflows – discounted at an appropriate interest rate – that can be expected to occur during the remaining life of the asset.

— Warren Buffett, 1992 Berkshire Hathaway Annual Report

Because of the difficulty of using a DCF, many software investors default to relative valuation multiples — the most common being a multiple of revenue. Boiling it down to a simple valuation multiple helps easily compare companies and estimate valuation. But…they can also be very dangerous because it is a simple shorthand method for what a DCF should theoretically determine the valuation to be. And then we use that multiple and compare it across dissimilar companies.

Valuation multiples attempt to accomplish a similar thing as a DCF. While professional investors are likely putting together a full DCF, many are just looking at valuation multiples and trying to draw conclusions.

One benefit of the DCF is that it forces you to explicitly consider the drivers of a company’s valuation. While a revenue multiple allows you to lazily compare companies without the same consideration. A major error frequently made in software valuation multiples is that software companies are very comparable. However, long-term growth and profitability of software companies can be wildly different (as many have recently discovered).

While you can make adjustments to the revenue multiple for differences in the business, this becomes even more subjective than a DCF. The fundamental drivers of valuations should be considered in both a DCF and valuation multiples, but in a DCF they are explicit while in multiples they are implied.

It is popular to hate on DCF models because of all the impossible assumptions that must be made. Yet these same people are also quick to talk about revenue multiples which just pack all of the DCF assumptions into a single number.

I am not saying revenue multiples are bad. They are useful for quick comparisons across companies and quick shorthand valuations, but investors need to remember the real valuation drivers and the limitations of using a relative multiple for valuations.

Software companies have the majority of their value tied in the outer years of a company’s life. They are hopefully growing rapidly for a long-time and investing cash flows into sustained growth until they reach a certain maturity where they can become cash printing machines. But revenue multiples typically only consider the next twelve months of revenue….

Below I analyze the largest revenue multiple changes over the past year and what investors got wrong or how business fundamentals that drive valuation changed.

Top 10 Revenue Multiple Increases

Looking at the relative revenue multiple changes above, you can conclude that the long-term revenue growth and profitability expectations of these companies should have improved a lot more relative to other public software companies.

Regardless of what I personally think about C3, investors are obviously now expecting that its potential revenue growth and profit potential is MUCH larger than it was last year (and better relative to most other software companies). In October, 2022 C3 traded at 1.8x revenue which was one the lowest software revenue multiples. Consensus was that revenue growth would only grow 1%….it actually grew 3% (not that much better) and expectations are for revenue to grow 17% over the next 12 months. Still now very high revenue growth, but there are obviously some expectations (hope) that revenue growth and profits can continue to accelerate long-term because of the artificial intelligence story.

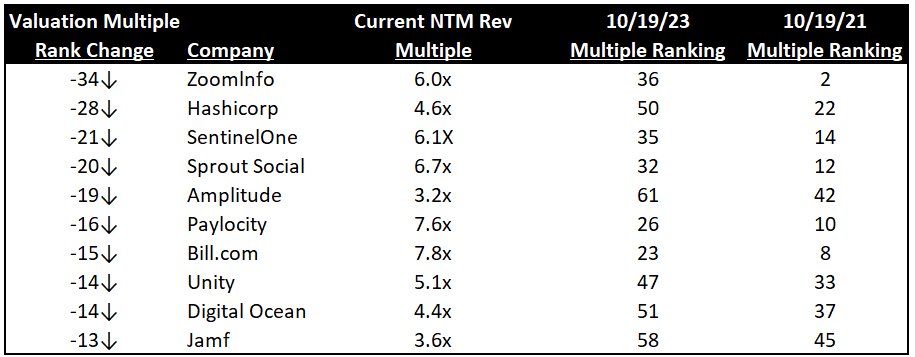

Top 10 Revenue Multiple Decreases

ZoomInfo was riding high this time last year at the second most richly valued company based on its revenue multiple, but since then it has dropped 34 spots which represents the largest relative revenue multiple drop amongst software companies.

What happened to ZoomInfo?

Keep reading with a 7-day free trial

Subscribe to OnlyCFO's Newsletter to keep reading this post and get 7 days of free access to the full post archives.