Entrata S-1 | An Actual Software IPO?!

How do Entrata's financials stack up, and will it pave the way for more software IPOs?

Brought to you by…Brex

AI agents in finance are really powerful when they have the right context, controls, and operating environment.

I (OnlyCFO) have been working closely with Brex for over 2 years, and what they’ve built for agentic finance (AF) is incredible. With Brex, agents handle all the tedious stuff, like expense reports, policy enforcement, and month-end close, so your team doesn’t have to. Check out Brex AF!

Entrata Files to IPO

Entrata filed their S-1 this past week and folks were surprised that they hadn’t heard of this hot new AI company before. Oh wait, Entrata is property management software…

There has been A LOT of excitement around the hot AI IPOs (SpaceX, OpenAI, Anthropic, etc), but most of us didn’t have Entrata on our list of companies to lead out the massive backlog of software IPOs. We have been constantly told over the last year that software is dead…

But Entrata seems alive and well! Not incredible metrics (particularly compared to all the AI stuff we constantly hear about), but really strong metrics compared to most software companies at their scale.

I know that a lot of software companies will be anxiously watching to see if Entrata will open the IPO floodgates for the hundreds of other “pretty good” private companies hoping to IPO in the near future.

Let’s dig into Entrata…the financials and story are really interesting.

Entrata’s Financial & Metrics

Estimating Entrata’s Valuation

Entrata’s Unique Fundraising History

How Does Entrata’s Financials Stack Up?

Entrata is a great business. They scaled without real venture capital money so they have always been efficient. So like most bootstrapped businesses, their growth rates have been more modest.

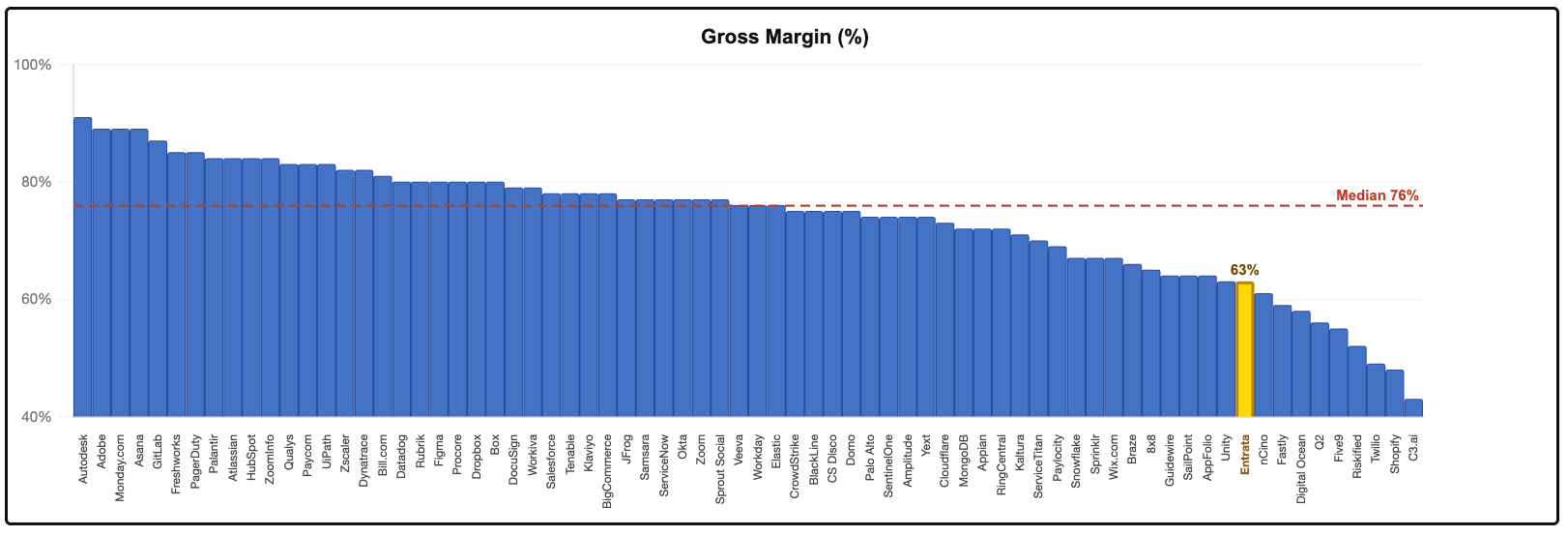

*Yellow bars are Entrata

Revenue

Revenue Scale

Revenue scale is important context. I see too many people say we are growing just as fast as X company but they are 10% the revenue scale…

Revenue Growth Rate

Entrata has a good growth rate (21st out of 73 companies). The market has definitely shifted to being more growth-focused again.

The general sentiment is that if growth isn’t strong, durable, and maybe even accelerating, then you are an AI loser. And AI losers have a terminal value of near $0.

Revenue Endurance

Revenue endurance measures how persistent revenue growth rates year-over-year. It is calculated as follows:

Entrata may not have had rocket ship levels of growth, but it has consistently just kept growing revenue at a good rate for a really long time. Entrata has a better growth endurance rate than almost any public software company over the past 5 years…

Profitability

Gross Margins

Entrata has bottom-quartile gross margins. Since they represent the ceiling of profitability, gross margins is a key metric.

While Entrata has lower gross margins, the improvement over the past couple of years has been incredible. From 54% GAAP gross margins in Q1’24 to 63% in Q1’26….

Increasing gross margins that much is hard to do. I believe a lot of it is a higher mix of customers with higher gross margin products, but also from continued product additions.

GAAP Profits

According to Alex Clayton at Meritech, Entrata is the largest software IPO to be GAAP profitable while growing 20%+. Not to diminish that record, but a lot of that is because most software IPOs were growing faster so they were trading profitability for growth (at least that was the idea…)

Regardless, Entrata is very efficient. Especially after considering their lower than average gross margins. Their OpEx is very efficient.

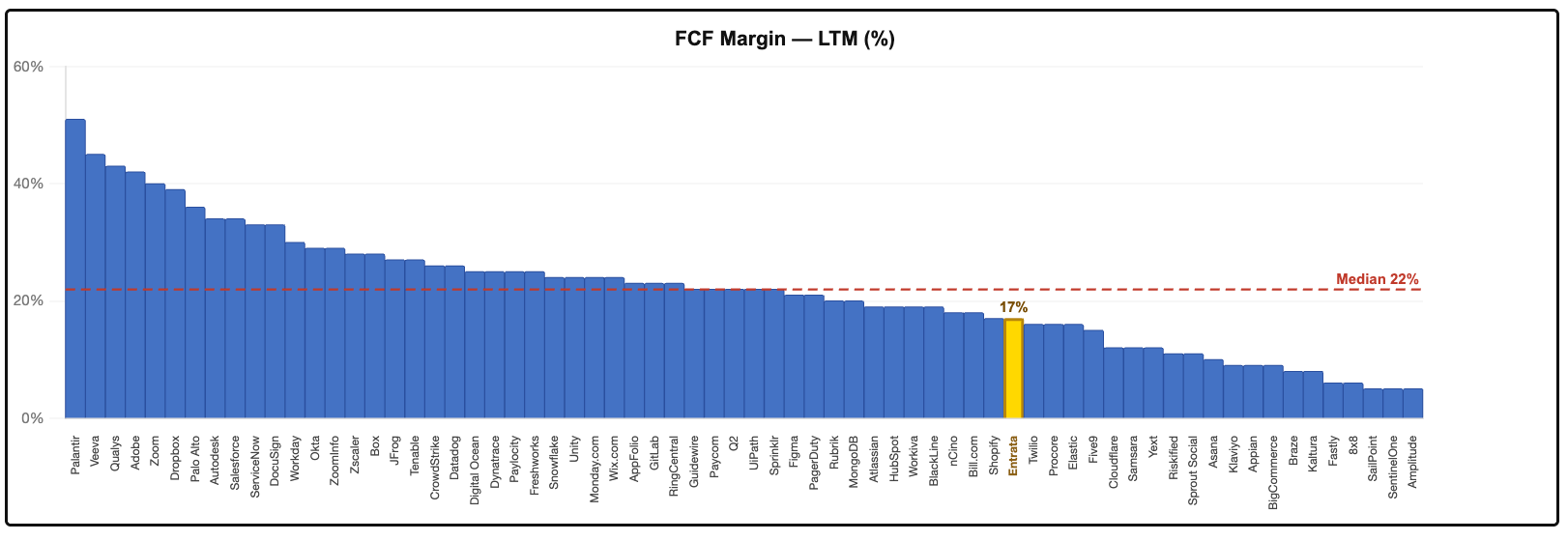

Free Cash Flow Margins

They have to be FCF positive for a long time given their [mostly] bootstrapped history. Entrata’s good (not great) FCF margins.

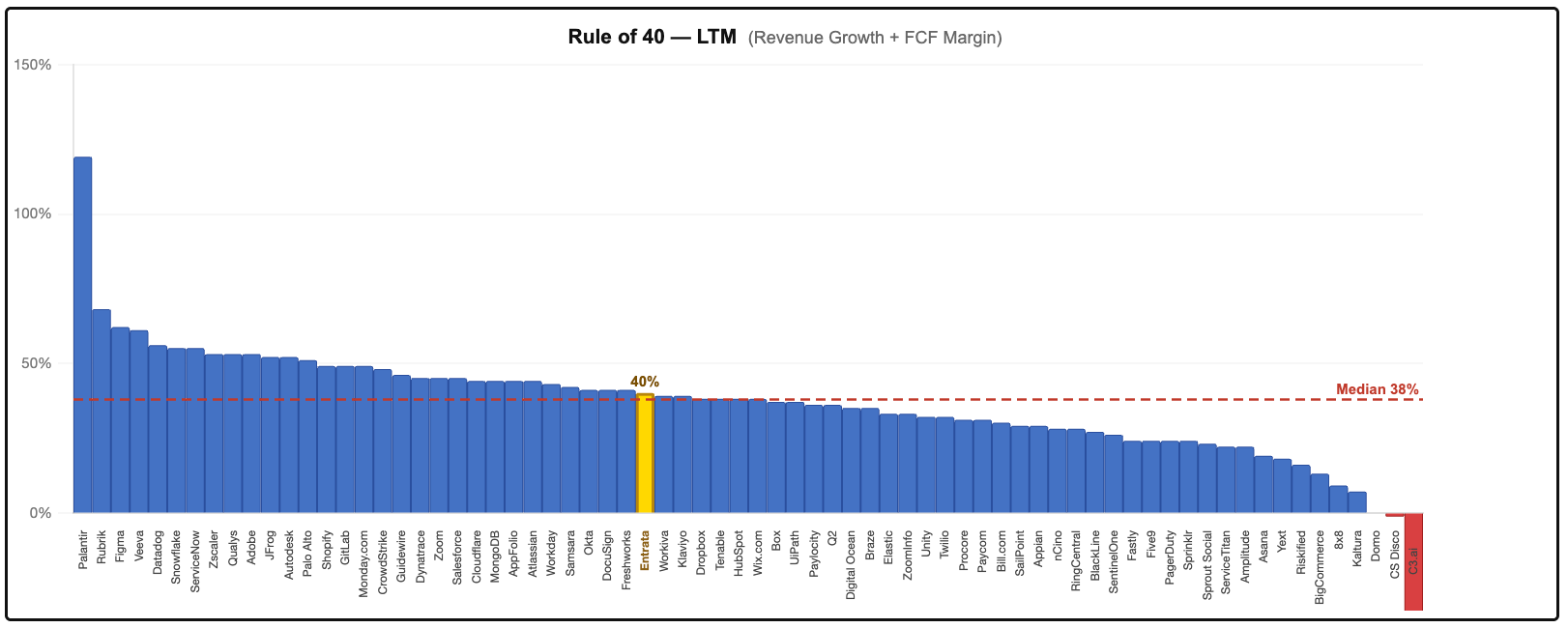

Rule of 40

The median software company has a Rule of 40 Score of 38. Entrata is just slightly better than that at 40.

Retention

Entrata also has great customer retention metrics:

GRR: 99% in 2024 and 97% in 2025

NRR: 117% for 2024 and 2025

Customers just don’t leave Entrata…And that is exactly what every software investor is trying to assess right now. “How durable will revenue growth be over the next 5 to 10 years?”

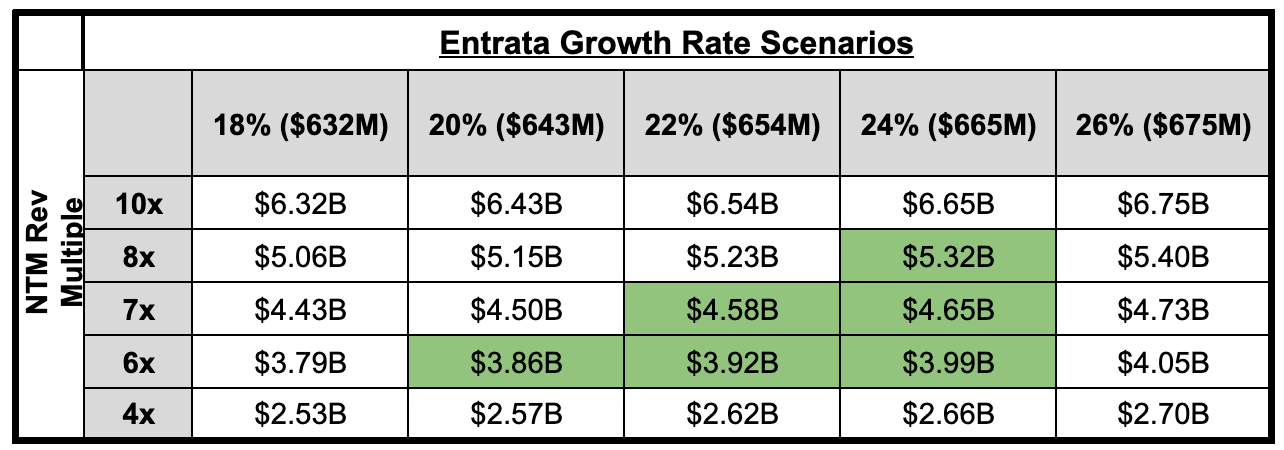

What Will Entrata’s Valuation Be?

Entrata’s last fundraising in May 2025 valued them at $4.3B. They also did a tender offer a couple of months later at the same price where employees and former employees sold $37M worth of shares.

It’s worth noting the public cloud stocks are down on average by 8% and their closest comp (AppFolio) is down 23% over the same period.

There isn’t going to be irrational exuberance around the Entrata IPO given all investors’ attention being on AI and other IPOs, but MANY folks will be paying close attention to it as a signal for the broader software IPO market.

Below is how I would expect Entrata to price at IPO.

Bootstrapping, Magic Mushrooms, CEO Forced Exit, & PE Takeover

Entrata (property management software) was founded in Utah 23 years ago when vertical software was a lot less sexy than it is today. Being in Utah and in vertical software at the time meant they didn’t follow the traditional VC path.

Two Early Investments (2005-2006)

Despite almost all reporting saying they bootstrapped for 18 years, Entrata did raise a couple of small early rounds (not institutional money though) in the early days.

In 2005 Entrata raised $125K at a $1M valuation. And then not too much longer after that they raised another small round at a $2M valuation (amount unknown but probably around $200K-300K)

Between these two rounds, Entrata was diluted by ~25% (my best guess)

Bateman recently said that the $125K investor/s made a 1,100x return on their investment (probably exited in the next round below). Not bad!

Founder Takes Magic Mushrooms (2018)

Bateman went to some magic mushroom retreat and decided he was done running Entrata. Bateman wanted to keep his equity but was done with the day-to-day. So Entrata hired a new CEO to run things.

1st Institutional Capital (2021):

PE Firm, Silver Lake, led a $507M round in 2021 (the largest private round in Utah history). The valuation was never disclosed, but I have a guess…

The Silver Lake investment was not all primary capital. There was likely a large amount of founder and early investor liquidity. Much of the details were never disclosed, but Bateman has said that he owned ~60% after the Silver Lake investment, which likely means a lot of the $507M bought out those early investors.

Based on some triangulation of the numbers above, I would guess the valuation was ~$1.5B.

CEO Forced to Sell 100% of His Holding Due to Unhinged Email (Early 2022)

Bateman sent a conspiracy-filled, racist email about COVID-19 to the most prominent figures in Utah.

Bateman was kicked off the board and they forced him to sell 100% of his holdings, which was led by Silver Lake. If Silver Lake acquired Bateman’s ~60% shares at the previously estimated round price of ~$1.5B, then he would have walked away with ~$0.9B, but maybe Silver Lake got to buy his shares at a bit of a discount given the circumstances….

After the sales of Bateman’s shares, Silver Lake became the majority shareholder of Entrata.

Blackstone Invests $200M at $4.3B (May 2025)

In May 2025, Blackstone invested $200M at a $4.3B valuation. A big increase in valuation from a few years earlier. The average public cloud company’s stock price fell by ~30% over that same period of time.

Debt and Dividend Recap

Entrata had $200M of debt on the books by 2024, but then in 2025 they refinanced and took on $400M of total debt. They used almost all of that to pay a dividend of $356M….

Entrata got good debt terms on it though.

They only have to pay $1M per quarter with a bullet payment at the end and a rate of 3% + SOFR.

Will Entrata Have A Successful IPO?

I really hope so because maybe that means Entrata will start to open up the IPO window for the hundreds of others waiting for their turn.

The timing is pretty good from both a market perspective (public software is up nearly 40% from the lows last month) and Entrata continues to execute strongly.

While not some sexy AI company, Entrata is a solid business. The big question is what valuation will investors give them when it seems like the only thing folks are excited about are all the potential hot AI IPOs (OpenAI, Anthropic, SpaceX, etc). And investors remain nervous about software, despite the recent bounce in stock prices.

Entrata seems like a great company with a lot going for it. We all just need to be able to answer one question: “How durable is revenue over the next few years?”

Congrats to the Entrata team! I am rooting for you.

Footnotes:

See how Agentic Finance can transform your finance department (today’s sponsor is Brex).

I wrote about how to significantly cut your ChatGPT/Claude spend on my new AI-focused newsletter. Check it out and subscribe

Subscribe and share the OnlyCFO newsletter with your teams

*nothing in this post should be considered investment, legal, or tax advice