Founder’s $125M Equity Mistake

How the founder of Klaviyo personally lost $125M to the government

Having someone with the right experience and ability to ask the right questions can save companies and individuals lots of money. Andrew Bialecki, founder of the latest software IPO (Klaviyo), found this out the hard way with a mistake (or potentially choice) that may cost him $125M!

When I read Klaviyo’s S-1 (IPO document) there was one thing that really caught my attention…

The CEO had ~$800M worth of stock sitting in early unexercised stock options🤯

These stock options were granted to Andrew immediately following their first raise of outside capital of $1.5M in 2015. For the three years prior to the first raise Klaviyo was bootstrapped (no outside capital), but then raised a total $778M before going public this year at a $8B valuation.

This enormous valuation and potentially bad tax planning means Andrew may have to owe an extra $125M to the government! Keep reading to find out why…

The $125M Mistake

The mistake Andrew made was one of omission. He didn’t early exercise his enormous amount of stock options when the company’s valuation was tiny. Perhaps this was an informed decision to not exercise because he determined that the $268K exercise price wasn’t worth the risk, but the tax impact remains the same.

Since these stock options were issued during the very early days of Klaviyo, they would have “only” cost him $268K to exercise in 2015. But as Klaviyo’s valuation skyrocketed over the next few years it became increasingly difficult to exercise because of the tax implications.

Early exercising means to exercise stock options before they are vested/earned. Typically stock options given to founders/employees have to be earned before exercised and they are typically earned over several years (4 years being the most common).

Executives (and almost always CEOs) are typically given an “early exercise” provision that allows them to exercise their stock options before they vest so they can lock in the favorable tax benefits. While there is risk involved of paying for shares of a very early startup, if the company valuation is small (with a small exercise price) then the cost will be small and the payoff potentially HUGE.

Even if Andrew didn’t have the $268k of cash to early exercise companies loan money to their CEO all the time so they can early exercise without fronting the cash (company loans also have their own set of risks). So Andrew could have received the favorable tax benefits with no upfront cash impact.

There is two tax benefits Andrew could have received from early exercising:

QSBS treatment

Taxed as long-term capital gains vs short-term

The result of these two tax benefits may cost Andrew nearly $125M in lost money to the IRS.

What is QSBS?

QSBS stands for “qualified small business stock” and is a U.S. tax benefit that applies to eligible shareholders of a qualified small business (QSB).

QSBS allows qualifying shareholders an exclusion from paying capital gains tax when the QSBS is sold. The gain exclusion is the greater of 1) $10m or 2) 10x the invested amount.

The most important rules for qualifying for QSBS:

Incorporated as a U.S. C-corporation.

Must have had gross assets of <$50M when shares are acquired

A key qualification that some people don’t understand is that in order to qualify for QSBS treatment you must own shares during the time the company is a qualified small business, NOT stock options.

QSBS protects founders/employees up to $10M from federal capital gains (and some states also follow QSBS federal rules). This would result in tax saving of >$2M! Andrew was granted stock options right after their seed round of $1.5M so Klaviyo should have been a qualified small business at that time.

For investors QSBS can be extremely meaningful and should factor into their ROI calculations. QSBS can protect up to 10x their investment from long-term capital gains taxes, up to $10M invested. For example, an investor who invested $10M could avoid paying federal capital gains tax up to $100M!

Word of Caution: Certain events can screw up QSBS and disqualify it. One such event is company repurchases of stock. I once saw a company screw up QSBS on accident because of the way money flowed for a secondary transaction being purchased by a VC firm — it was structured as a repurchase by the company and then sale to the VC firm rather than directly between the 3rd parties. The company was using a 2nd tier law firm and it caused the early investors to lose millions of dollars to the IRS!

Long-Term vs Short-Term Capital Gains

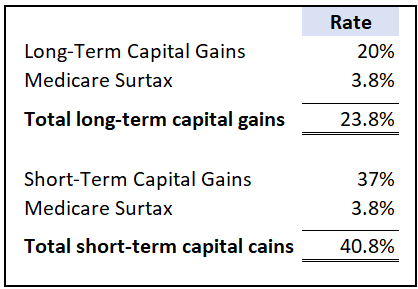

Andrew will likely be hit with short-term capital gains tax on the gains on these unexercised stock options. In order to qualify for long-term capital gains treatment, the stock options must be exercised and held for at least one year. The difference between these tax rates is huge.

If Andrew had early exercised his stock options in 2015 then he could sell all of those shares immediately and get the much more favorable long-term capital gains tax treatment.

The Math Behind the $125M Mistake

Let’s start with the exercise price. It will cost Andrew $268K to exercise his options today.

The implied gain based on Klaviyo’s stock price today of $33.50 is $717.6M. Calculated by taking the # of shares multiplied by the change in share price. This is the amount subject to income taxes.

As I said earlier, had Andrew early exercised he would benefit from 1) QSBS and 2) long-term capital gains. Since Andrew didn’t early exercise then he will likely have short-term capital gains treatment for all of the gains on these stock options, which is taxed at the ordinary income tax rate.

The tax rate for Andrew will be 45.8% after adding the medicare surtax and Massachusetts tax rate (where is lives). $329M is a lot of taxes…..

Now…had Andrew early exercised in 2015 then things would have turned out much differently. $10M of his gain would have been protected from both federal and state income taxes (Massachusetts follows federal QSBS rules). The remaining $707M gain is then taxed at the much more favorable long-term capital gain tax rate.

While the $10M gain exclusion from QSBS for Andrew seems relatively small, for most founders and early stage employees it can be a relatively huge life-changing amount.

The difference of what Andrew will likely pay in taxes from these unexercised options and what he would have paid if he early exercised is $125M!!!

Also, Massachusetts just passed a "Millionaire Tax" this year which is a 4% surtax on income exceeding $1M, which then makes the effective tax rate 9% for Massachusetts for income above $1M! Four percent will be a lot of taxes for Andrew…

Concluding Thoughts

Early stage founders and employees need to be aware of these tax differences because they can result in life changing amounts of money. I know taxes are not what you are focused on when you are building a company, but taking time to understand this stuff is important because there are limited windows of time to make these decisions.

Every situation is different with complex pros/cons. These are not easy decisions with straightforward answers and hindsight is always 20/20. I always recommend assuming your private company stock options will be worthless and never to risk more than you can afford.

Luckily, there are a lot of smart people and services now that help founders and employees navigate these complex decisions — I would guess that Andrew wish he had access to them back in 2015. Companies like Secfi offer self-serve equity planning tools, equity financing for exercising and liquidity, and equity-focused wealth management services

But for those of you concerned about how Andrew will be able to survive with losing that much money to the government…He owns 38% of a $9B company so he will probably be OK. Still stings though!

Side Note - Andrew could theoretically exercise now and hold for a year to get long-term capital gains treatment and save on some of these taxes but there is significant risk with that approach that is beyond the scope of this article. Risks include AMT implications and the risk of the stock price plummeting after the fact. Every situation is different so talk to a tax advisor!

Special discount on paid plans: For those loyal readers who made it this far, below is a special discount of the OnlyCFO paid tier for both monthly and annual subscriptions. Good until October 20th.

***This is not tax or investment advice. There are a lot of nuances to QSBS, tax holding periods, and how tax rates are calculated. I am not a tax expert. If you are looking into these things then I strongly recommend consulting with an experienced tax advisor.**

Great article. To your side note - Yes Andrew could theoretically exercise now, but he would have to come up with $328MM in cash in order to do it. Banks won't lend against unexercised stock options, even for public companies. So the only way for him to get that much money (other than robbing the bank) would be to "cashlessly exercise" or sell stock to get the funds he needs to exercise his remaining stock. Depending on the 10B5-1 trading plan, they may force everyone to do this anyways. If he could rewind the clock (hindsight being 20/20), another option to fund his original $268k bill would be through private stock financing. In addition to SecFi, there's also Quid (my employer), LiquidStock, and ESO Fund who specialize in these types of financings.

In fairness, there are two other considerations:

1. This is a very easy post-facto analysis. If he had had the company loan himself the money in 2015, and the growth had not provided a billion-dollar exit, or if preferences from further fundraising plus a weaker outcome had made his stock valueless, he would be on the hook for the loan. Even if the company forgave the loan, that would be considered income and he would have owed taxes on the forgiven loan.

2. The idea that it is "a loss" to pay taxes is a deeply selfish message.

I have been on both sides of this issue - exercising early and ending up with worthless shares or exercising late and having a big tax bill. And I know people who have lost or are losing their homes because they exercised options during the COVID ecom boom and now the shares are essentially valueless.

Not to say he made the right choice, but at least tell the whole story. Maybe "$125M choice" instead of "$125M mistake"