How to Read Balance Sheets - Software Edition

People often talk about the income statement, but most people don’t really understand how to properly read a balance sheet. A balance sheet is a snapshot at a point in time of a company’s financial health. This is in contrast to an income statement which is for a specific period of time (monthly, quarterly, annually, etc).

A balance sheet includes three main sections:

Assets: What a company OWNS

Liabilities: What a company OWES

Equity: Value attributable stockholders

If you have taken an accounting 101 course then you have heard of the formula that assets must equal liabilities plus stockholders’ equity. What many people don’t understand is that the income statement (represented by “net income (loss)” below) is a part of the balance sheet.

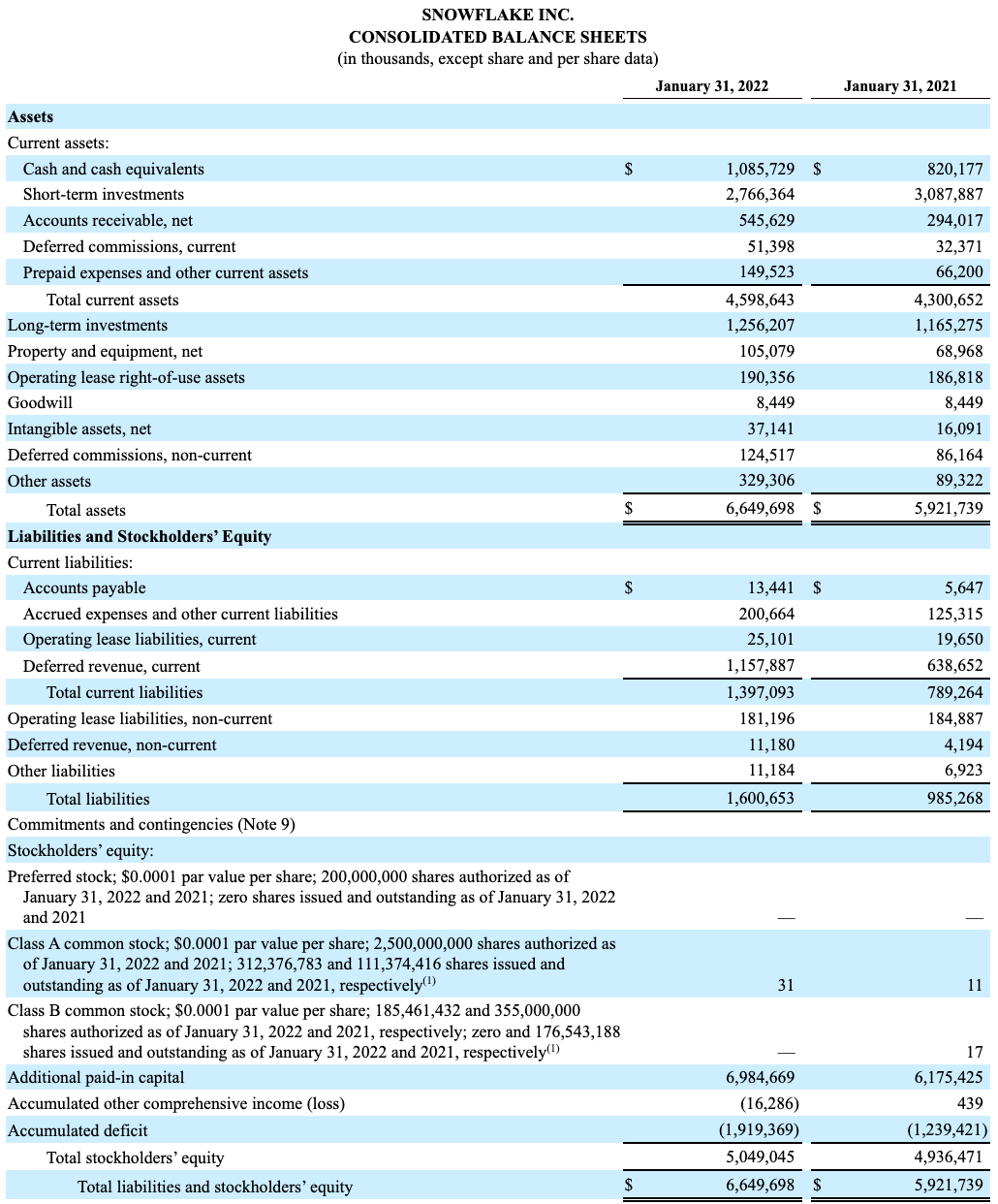

I am going to walk through the sections of a balance sheet using Snowflake as an example.

Sections of the balance sheet

Assets

The first section on a balance sheet is assets. Assets are what the company OWNS. Assets are things that can be sold for money if liquidated or used to generate future monetary benefits.

Assets are typically presented in order of liquidity (i.e. how readily they can be converted to cash or used to generate cash).

Below are the main sections of a SaaS company’s asset section:

Current Assets - the company expects to be able to convert to cash OR consumed within one year. Current assets include things such as the below.

Cash and cash equivalents

Money in the bank or in very short-term (< 90 days) maturity, liquid investments such as T-bills, CDs, and money market funds.

Short-term investments

Investments in debt securities with maturities greater than 90 days (but typically less than 1 year) when purchased.

Accounts receivable

Money currently owed from customers. This is the amount invoiced to customers or contractually owed based on services performed.

Most B2B SaaS companies have annual upfront invoicing terms, which means that immediately as an invoice is issued the entire amount becomes part of accounts receivable (even though it is for future services).

Deferred commissions

Accounting rules require SaaS companies to almost always capitalize a large portion of sales commissions and recognize the expense over time (typically between 3 and 5 years).

If a commission is earned solely based on closing a deal, then it is likely capitalizable on the balance sheet. This would typically include commissions for AEs, AE managers, SEs, etc. Commissions for most SDRs though is based on some metric before a deal is close (like meetings set) so those costs are expensed on the income statement as incurred and not capitalized.

Deferred commissions example: Sales rep earns $10k on January 1st, 2022 for selling a SaaS widget. Instead of expensing the $10k on the income statement on January 1st, it is put on the balance sheet as an asset and then expensed evenly each month for the next few years (depending on the company’s accounting policy). For SaaS companies, this is usually between 3 and 5 years.

Because commissions are capitalized certain SaaS metrics can get messed up and become misleading.

Prepaid expenses and other current assets

This can include a variety of things but some major items for SaaS companies include: software (we love to buy lots of other SaaS products), marketing events & programs, rent, insurance, etc.

Non-Current Assets - not expected to be converted to cash OR used within one year. Some items here include:

Long-term investments

These are investments with maturities greater than one year.

Property and equipment

Most SaaS companies are not very capital intensive. Typical items included in this section include:

Computer equipment

Furniture

Office improvements

Internal use software - these are costs used to develop software for internal purposes.

For SaaS companies, internal use software includes a portion of the costs used to develop the SaaS solution, which is typically a small percentage (< 5%) of engineering costs.

Operating lease right-of-use assets

This represents the company’s right to use a leased item over the lease term. The asset is recognized based on the present value of all lease payments over the lease term. The most common leases included here are office leases, but there could be others.

Goodwill

Premium amount paid over what is determined to be the fair value of an acquired company. Goodwill frequently results when a company buys another company.

Intangible assets

These are assets that are not physical, but frequently very valuable. These assets generally are a result of business/asset acquisitions because under accounting rules a company can’t typically create an intangible asset. There are two types of intangible assets: 1) finite-lived assets and 2) infinite-lived assets.

Below is the intangible asset breakdown for Snowflake.

Deferred commissions, non-current

This is the amount of deferred commissions that will be expensed after one year. See the deferred commission explanation under the current section for more detail.

Other assets

There is often some miscellaneous stuff in here, but larger companies like Snowflake may also have equity investments in both public and private companies also included in this section.

Liabilities

Liabilities are what the company OWES.

Liabilities are presented in order of when the they are due, with the most current showing first. Similar to assets, liabilities are presented in two main sections (current and non-current).

Current liabilities - obligations expected to be settled in <1 year

Accounts payable

Vendor bills that are due for payment

Accrued expenses and other current liabilities

These occur when expenses are incurred that haven’t been paid. If they relate to vendor expenses then if a vendor bill is received then it is transferred to accounts payable until paid.

Operating lease liabilities

This is the other side of “operating lease right-of-use assets” mentioned above. It is the amount owed over the contract term of the lease.

Deferred revenue

For SaaS companies, once an invoice is sent to a customer then the amount of the invoice is added to deferred revenue. Deferred revenue is decreased when revenue is recognized.

SaaS companies want their deferred revenue to be continually increasing because that implies that customer invoicing is increasing which implies that the company is growing by closing more deals.

Does the below joke make sense now?

Liabilities are generally viewed as a negative, but SaaS companies typically want their deferred revenue liability to always be increasing.

Non-current liabilities - obligations expected to be settled in 1+ years

Operating lease liabilities, non-current

This is the long-term portion ( 1+ years) of the operating lease liabilities noted in the section above.

Deferred revenue, non-current

This represents the portion of deferred revenue that won’t be recognized as revenue for 1+ years.

Debt

While most VC-backed SaaS companies are primarily funded via preferred equity from venture capital firms, some companies will also use debt to help finance operations or acquisitions.

Other liabilities

This is for other miscellaneous liabilities that don’t fit into one of the previous buckets. If anything becomes big enough in this section then it will need to be broken out separately.

Stockholders’ Equity

Stockholders’ equity is the value attributable to the business owners (aka stockholders).

Some people think of this section as the company’s net worth after netting the company’s assets and liabilities, but remember that a lot of the company’s value is not represented on the balance sheet. This is because companies build up significant value in their brand name, customer relationships, technology, etc that the accounting rules prevent from being recognized on the balance sheet for accounting purposes.

The main sections of stockholders’ equity include:

Common stock & Additional Paid-in Capital

These two sections primarily refer to all the money invested in the company by shareholders.

Retained earnings (or accumulated deficit)

This represents the net profits from the income statement that are reinvested in the business. There are two things that impact retained earnings:

Net income / (loss) adds or subtracts from it

Dividends paid out decrease it

Given most SaaS companies are not profitable for a long time, they will typically use the caption “accumulated deficit”. Once a company is profitable and digs itself out of the hole, then the caption will switch to “retained earnings”.

How the Balance Sheet Balances

The balance sheet equation MUST always be true. If it ever doesn’t, then an accountant isn’t doing their job right.

Let’s take an example and see how it flows through the balance sheet.

Example: A SaaS company sells a $100k deal for its SaaS solution with a subscription term of 12 months and upfront payment terms.

As you can see above, at each point in the process assets = liabilities + equity.

Remember that everything that flows through the income statement ends up hitting the equity section.

Concluding Thoughts

The income statement is more intuitive and more commonly understood, but understanding the balance sheet is critical for understanding the health of a business.

In a subsequent post, I will cover how to analyze the balance sheet to determine the health of a business.

If you want to keep learning then you better subscribe!

Much needed breakdown. Loved the real life examples.

Great breakdown, very valuable as a reference!