Is Klaviyo Richly Valued? | Power of Growth Endurance

Niches get riches but is the growth and efficiency durable?

👋 Hey, I’m OnlyCFO and welcome to a subscriber-only edition 🔒 of my newsletter. Each week I cover topics about the software industry to help operators and investors. My focus is on finance, accounting, and operations of software companies.

Klaviyo is the first software IPO in almost 2 years so there has been a lot of excitement around its public market debut three weeks ago. While a bit volatile in its first few weeks of trading (the broader market volatility hasn’t helped), Klaviyo’s stock has held up pretty well — its IPO price was $30 and closed trading yesterday at $33.50 (12% above IPO price).

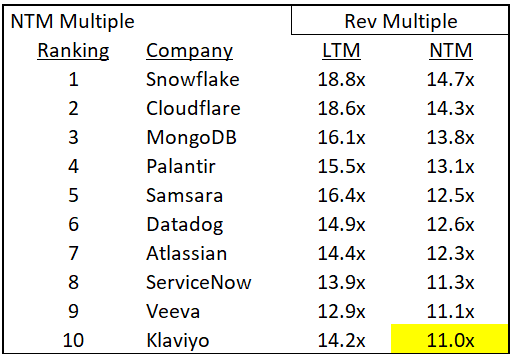

Klaviyo trades at a valuation multiple of 14.2x on a last twelve month (LTM) basis, which is the 8th highest amongst public software companies. While consensus estimates are not out yet for the next twelve months (NTM) growth expectations, based on yesterday’s stock price it may be somewhere around a 11x multiple on a NTM basis which is around spot #10 for the highest NTM valuation multiples.

Revenue multiples are a valuation shortcut to quickly compare and analyze software companies, but the simplicity and overuse of these multiples can cause bad decision making because they don’t look at all the other factors that create long-term shareholder value.

Revenue multiples disregard two key components of a potential long-term outlier company that will have an outsized investment return:

Profitability

Endurance of performance

Profitability

By now everyone should know that the days of growth at all costs are dead. In 2021 software companies could IPO while still losing enormous amounts of money. The next class of IPOs will need to be close to cash flow breakeven or even profitable before going public to have successful public market debuts.

The first software company to IPO in almost 2 years, Klaviyo, definitely fits this description:

24% free cash flow (FCF) margin in its most recent quarter

77% gross margin

Positive GAAP and non-GAAP operating margin

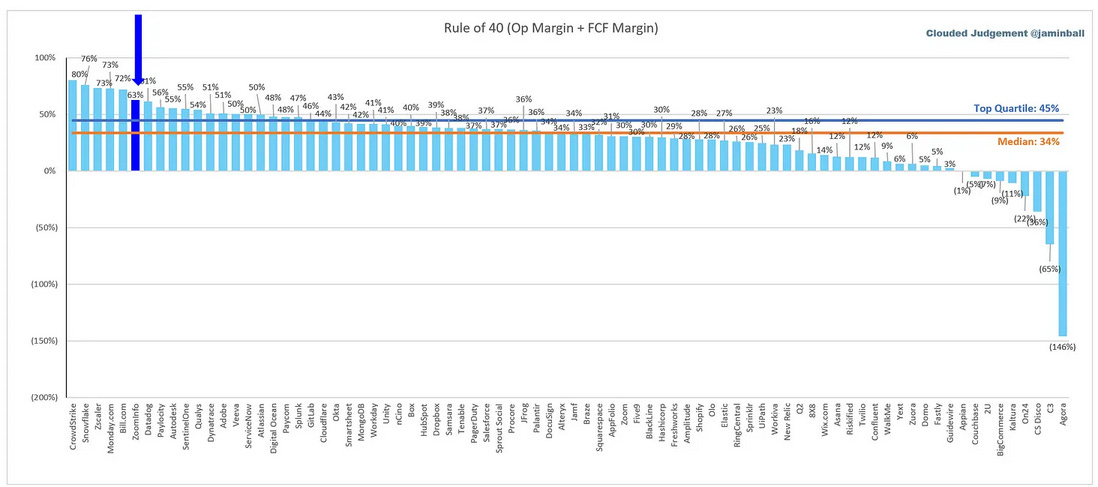

Klaviyo has one of the highest Rule of 40 scores (see chart below). Rule of 40 looks at the balance between revenue growth and profitability. Klaviyo has a Rule of 75 (51% growth and 24% FCF margins) in its most recent quarter. Klaviyo is growing very efficiently!

Klaviyo appears to be checking all the boxes on an efficiently run company that is on track to generate the profit margins that we were promised with software companies.

Endurance of Performance

The question for Klaviyo and all other growing software companies is the durability of their performance. This is where MANY software companies have gotten in trouble. Growth was a rocket ship and then seemingly out of nowhere it fell off a cliff and never really came back.

The reason software valuations can be such a high multiple of revenue is because of an assumption of both 1) continually improving profitability and 2) high revenue growth endurance.

A potential concern with Klaviyo is that the IPO was perfectly timed to reflect peak revenue growth/profitability but the durability of that will be weak.

Improving Profit Margins

Software companies can be cash printing machines at scale given their power in distribution, high gross margins, and continually shrinking marginal cost for each new customer.

There is an expectation that software companies can get to 25%+ FCF margins and be able to maintain that profitability over a long period of time.

Below are the public software companies with the highest FCF margins.

Veeva holds the #1 spot with a 44% FCF 🤯! Veeva’s revenue multiple does not tell you about profitability — although it theoretically is baked into the multiple because it’s valuation *should* receive a big premium for how profitable it is today (versus promises of future high profitability).

Klaviyo’s FCF margin of 24% in its most recent quarter certainly looks great given its smaller scale and high growth rate. But can it get to 30%+ FCF margins and maintain that profitability level?

Klaviyo’s Profitability Outlook and Considerations:

Keep reading with a 7-day free trial

Subscribe to OnlyCFO's Newsletter to keep reading this post and get 7 days of free access to the full post archives.