Lies, Damned Lies and Recurring Revenue

A guest post with the Godfather of Customer Success (Nick Mehta)

OnlyCFO is brought to you by… Deel

Global payroll costs extend far beyond salaries. This guide breaks down international payroll expenses, compliance costs, and hidden fees so you can forecast accurately, reduce risk, and improve cost efficiency as you scale. Built for finance leaders managing multi-country operations.

The 8th Wonder of the World Is Crumbling

Einstein allegedly once said that compound interest was the 8th wonder of the world. Einstein was wrong. At least there was something that took its place for the last 20 years…

Annual recurring software revenue was the 8th wonder of the world. But now AI seems to be destroying such a beautiful thing that so many of us were able to witness (and profit from…)

There are two questions that every company needs to answer in 2026:

How recurring is your revenue, really? Not based on historical retention metrics. Those aren’t nearly as meaningful right now. But based on AI today and your current products.

If it isn’t truly recurring, what does that mean for your company?

To help answer these questions, I went to the person who understands the value of retention and recurring revenue better than anyone else I know…

Nick Mehta (former CEO of Gainsight) is the Godfather of Customer Success, which largely exists because of the concept of recurring revenue. As such, few people understand this topic better.

So you should read what he has to say…

Lies, Damned Lies and Recurring Revenue

-A guest post by Nick Mehta

Games, Golf and Gartner

In 5th grade, I co-founded a tech company, if you use the term “tech” loosely. My co-founder and I would solve PC video games (“King’s Quest”-types, to completely date me) and print up a guide to solving the game. We sold them in the cafeteria at lunchtime for a whopping $5 a pop! Alas, our empire came crashing down whenever Sierra Online issued a new title. All of that work (work being playing video games) had to be done again.

In college, our golf dot com startup had to convince you to misguidedly buy new clubs each season. Beyond demand for golf balls, customers had no need to come back.

And for my first job, we sold backup software that you paid for one time per server, plus a small annual maintenance fee. All that mattered was getting analyst firm Gartner to like your product.

Romancing Recurring Revenue

As such, when I ran my first SaaS company, I had to google this idea of “recurring revenue.” I learned from the master, as I tore through Marc Benioff’s classic, Behind the Cloud.

From my last startup’s launch in 2013 to its sale to private equity firm Vista Equity Partners in 2021, Annual Recurring Revenue (ARR) became Awesomely Reliable Religion.

To state the obvious, the beauty of the SaaS business model was:

Invest Research & Development (R&D) upfront to build a product

Deliver it at good Gross Margins at scale (70%)

Spend one time dollars to acquire customers

Capture revenue annually with a high rate of retention

In the mature phase, you can cut Sales and Marketing and R&D and drink from the fountain of ARR

You could even raise prices, since customers couldn’t leave

In this way, some companies with sticky businesses eventually got to operating margins over 50%. Alternatively, if TAMs were big, companies could defer monetization and keep growing R&D and S&M, with the comfort that the tap of recurring revenue will be there when they need it.

Times were good!

A Tale of Two Cities: AI and SaaS ARR

It certainly is the best of times and the worst of times.

For AI startups, ARR is more of a “concept of a plan.” Don’t be a buzzkill and ask questions!

The A isn’t always really annual (since most revenue is consumption-based). The first R is certainly not contractually recurring. It’s unclear how much will recur but for now, there is so much top down pressure from companies to buy AI technologies that growth is off the charts. And the last R? Let’s just make sure the auditors don’t ask any questions yet.

For SaaS incumbents, to paraphrase another Dickens tale, ARR feels like the ghost of Christmas past. Just 4 years ago, investors drooled over recurring revenue. A few months ago, I was at a charity event with mostly hedge fund types and every time I told them I worked in software, they shouted out “software sucks!” Nice to meet you too?

Death of Terminal Value

On the surface, it looks like investors simply irrationally corrected SaaS stocks. Under the covers, the truth is harsher. If we go back to SaaS playbook from a few sections back:

Invest Research & Development (R&D) upfront to build a product

Deliver it at good Gross Margins at scale (70%)=> unclear if margins hold given inference costsSpend one time dollars to acquire customers

Capture revenue annually with a high rate of retention=> huge concern that customers attrit quickly given ease of competitive offerings being built with agentic codingIn the mature phase, you can cut Sales and Marketing and R&D and drink from the fountain of ARR=> as such, it’s not obvious you can cut ongoing costs and radically increase profitsYou could even raise prices, since customers couldn’t leave=> raising prices seems almost impossible in this climate

Welcome to the Annual Recurring Restart

In the most depressing version of this story, SaaS companies now have to have the following strategy:

Invest significant R&D every year to keep up as the market evolves at light speed

Accept the risk of lower Gross Margins

Think of customer acquisition and retention as more similar than not - every “renewal” is a new sale

Forget about price increases

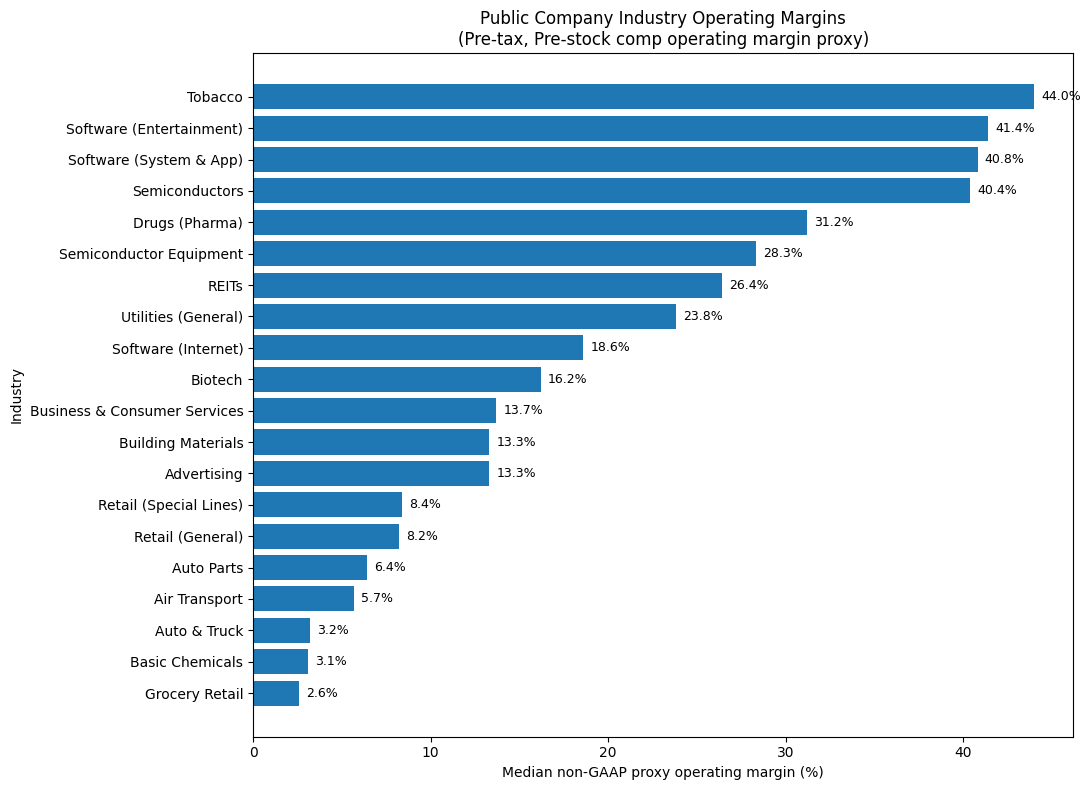

As such, if we assume 60% Gross Margins, 15% G&A (better at scale but scale might be tough), 15% R&D and 20% S&M, we might be looking at well-run companies having 10% Operating Margins (and we haven’t even touched Stock-Based Comp yet!)

Think that’s crazy? Most businesses don’t have the historical stickiness and moats of the high-margin software industry:

Unfortunately, if we assume a 4.3% 10-year US Treasury risk-free yield and the current 5% equity risk premium from Kroll (as of March 2026), we get a discount rate of 9.3%.

While SaaS companies can still grow, investors are skeptical. So a 10% operating margin SaaS business with 5% perpetual growth and a 9.3% discount rate (it would probably be higher since there are concerns about SaaS) would be valued at 2.33x revenue.

What are your options beyond that ridiculous plan? I see 2 at this point for SaaS companies.

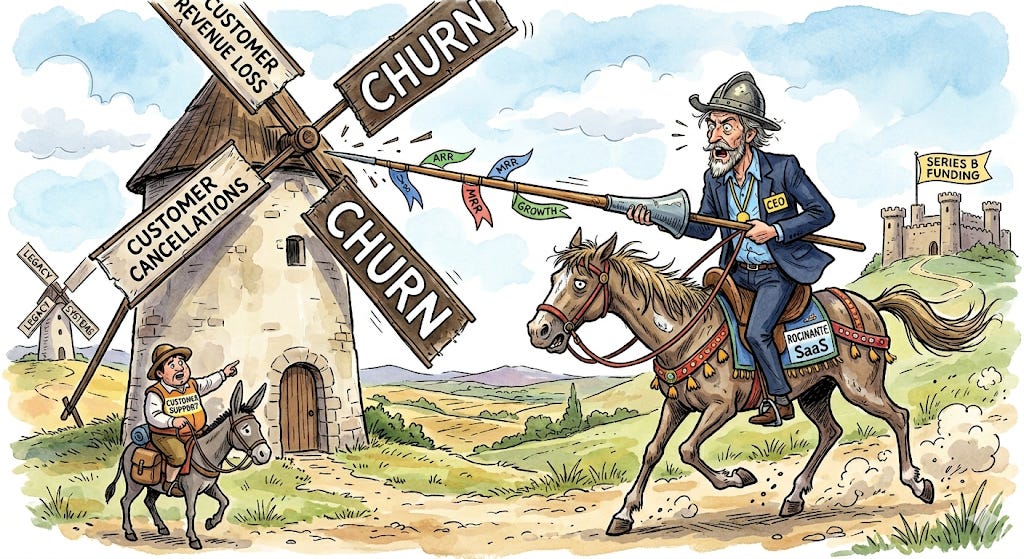

Option 1: Man of La Mancha

Perhaps the critics are wrong. Maybe the current storm is temporary. Some CEOs are clearly trying to fight the good fight, to badly stretch Cervantes.

They might take growth expectations down and take a big hit. But they use that money to invest in the current R&D, Sales and Customer Success motions. They batten down the hatches during this current craziness. Wow I’m mixing metaphors.

Option 2: Eternal Sunshine of the Spotless Mind

One advantage of terminal values being so low is that many companies have very little to lose. It’s hard because these businesses have been built with a leadership team that was used to the classic model. It’s incredibly difficult to pull off, but the best move for most SaaS companies is to find the Lacuna mind-erasing machine from the Charlie Kaufman classic and wipe out their old way of thinking.

One of the few successful examples of this approach is Intercom. Intercom was able to stare its core business in the face and sacrifice short term results to go all in on agents. Today, Intercom is one of the fastest growing private incumbent SaaS companies around. I’ll let their founder Eoghan McCabe tell the story, because no one else can do it justice:

Tip Your Wait Staff!

I’ll admit this wasn’t the most cheery post. I hope you take away that:

The concept of ARR was fun while it lasted.

We no longer can take it for granted.

One approach is to fight in the old world.

Another is to “burn the boats,” Intercom-style, and go to the new world.

In short, software isn’t dead. But it’s no longer recurring.

OnlyCFO Final Thoughts

Recurring revenue didn’t just mean that customers stuck around (although that was an important piece!). It also implied that there were only small, incremental costs required to keep them as customers. That’s what enabled software companies to become so profitable (and valuable).

If you have to substantially reinvent each year, then the current model doesn’t work…

That doesn’t mean all hope is lost, but you do have to adapt. It means more refactoring for AI in order to survive and probably leaner teams as well.

Nick’s definition, “Annual Recurring Restart”, might be the most truthful version of ARR for most companies in 2026.

Footnotes:

*Thanks Nick for sharing your insights!

Want to know the cost of offshoring by country? Check out this International Payroll Guide that breaks down all the costs you should be considering.

Reply to this email if you want to sponsor OnlyCFO

I love this post… as depressing as it is. And must say that I feel some jealous pangs as Nick beat me to the punch of guest posting for OnlyCFO this year.

Nick- you are of course spot on in your observations. But I do think we all need to take a deep breath. Sure let’s lament the end of the gravy train we got with high gross margins, 120% ARR and 10X+ ARR multiples in unicorn VC valuations.

Always with the deus ex machina of a PE buyer (or even better a strategic) at the end of the yellow brick road.

But - even today, I still believe there are great businesses to be saved (or started) that are “recurring” and high margin with good growth, even if not based on seat -based subscriptions. I believe that if you optimize for the new economics (far fewer people, rapid iteration of products, etc) and leverage available due to AI and agentic workflows - well there is still gold in them hills!

Orlando Bravo said it well. AI is a tailwind for software. How can it not be?! And Anthropic and Nvidia don’t get to keep all the economics. The application layer requires specialization. Someone’s going to win in each category. Buck up!

Nick nailed it—ARR was the 8th wonder of the world and indeed fun while it lasted. 'Annual Recurring Restart' is a much more accurate term going forward, but it completely upends the economic and investment model everyone's been riding for years. No more 'set it and forget it' renewal or margin assumptions - now it's constant and ongoing reinvention just to stay relevant. The SaaS industry has no option other than to cross this bridge, but it's a bumpy road ahead.