Lies of ARR vs GAAP Revenue Growth

Understand the differences so you don't get fooled

SaaS companies love their financial metrics and various acronyms, but the problem is that there are no standard definitions that are used consistently across the industry. This creates a lack of comparability when analyzing metrics and comparing investment opportunities. There are dozens of definitions that folks may be referring to when they say “revenue”, but the only one with a standardized definition is GAAP (Generally Accepted Accounting Principles) revenue.

Understanding the differences in all of these “revenue” definitions is important for both operators and investors to make appropriate conclusions about the financial health and trajectory of a business.

If I wanted to trick investors, I would be shifting focus right now from ARR to GAAP revenue growth rates….read on to learn why.

Ledge just released a new solution that gives finance teams that are managing multiple banks and accounts a single platform for real-time cash visibility, alerting, and transfers so that they can minimize risks while staying in control of their cash. It’s easy and simple to set up.

OnlyCFO - with everyone now setting up multiple bank accounts, it’s not a bad idea to have real-time visibility and consolidated reporting.

Check out Ledge’s solution here

What is “Revenue”?

There are tons of “revenue” terms that get thrown around and the worst part is that each company may calculate them slightly differently.

ARR, MRR, ACV, Contracted ARR, Committed ARR, GAAP Revenue, TCV, RPO, and the list goes on…

The two most common top-line metrics talked about though are ARR (annual recurring revenue) and GAAP revenue.

What is ARR and can we agree on the definition?

ARR typically refers to “annual recurring revenue”, but there are lots of creative alternative names (see below). Not sure how RingCentral gets “ARR” from “Annualized Exit Monthly Recurring Subscriptions”…

Ray Rike's SaaS Metrics Standard Board is a great resource created by smarter folks than me trying to standardize a lot of SaaS metric definitions. But…I don’t 100% agree that every definition/rule that they have defined is right for every company. If I don’t agree with everything, then I assume there will be others that disagree as well, so we won’t have truly standard definitions anytime soon. There are just too many judgments or company-specific circumstances that will push companies to do something slightly different since there is no regulatory body enforcing standardization (like GAAP revenue).

Annual Recurring Revenue (ARR) - the current annual recurring revenue of subscription agreements from all customers at a point in time.

ARR = ARR at the beginning of the Year + ARR gained from new customers + ARR gained from expansion – ARR lost to downgrades – ARR lost to customer churn

ARR = MRR (monthly recurring revenue) * 12

The above calculations are fairly standard, but what goes into ARR/MRR or how they are defined is the primary source of disagreement. While I am not going to try to define what goes into ARR here, below are some potential things that might be debated:

Does contract length matter? Does short-term count?

Late but anticipated renewals count?

Pricing model? Does usage-based pricing count? How about consistent overages?

Do professional services (i.e. managed services) that are recurring get counted?

Do you count contracted but not yet live customers? What if the gap between contracted and live is really short?

There are lots of questions like the above, that causes companies to calculate ARR differently.

ARR drives valuation multiples, internal compensation targets, and a lot of SaaS metrics are based on it. Operators and investors need to make sure they understand what is being included so they make appropriate conclusions, comparisons, and take the right actions.

ARR is a typical north star metric for most SaaS companies because it’s a more leading indicator of growth. But not all public companies report ARR. Ordway reported that only half of public SaaS companies reference ARR and only about half of those reported ARR as a key business metric.

GAAP Revenue

GAAP revenue is the number reported on all income statements. Every company must report GAAP revenue. Both private and public companies follow the same accounting principles to determine the amount of revenue to recognize. In order to pass a financial audit, GAAP revenue must abide by the accounting rules. There are no such rules or regulating bodies for ARR.

GAAP revenue is recognized when a customer “obtains control of promised services”. In a SaaS agreement that delivers value throughout the term of the contract, this typically means that revenue is spread ratably over the contracted term.

Example of a $120K SaaS contract for 12 months: You would recognize the $120K ratable over the 12 months. Roughly $10k/month - I say roughly because it should be recognized on a daily basis.

Trust me when I say that the above overview is a major simplification of how revenue recognition works. There are thousands of pages written on the topic. Larger software companies have 50+ page memos and technical revenue recognition accountants in order to recognize revenue…

GAAP Revenue vs ARR

There are pros and cons to both of these top-line metrics, but most folks look at ARR given it’s more of a leading metric. But since a lot of public companies don’t report ARR, investors are left looking at revenue. Also, since not every company reports ARR, investors sometimes just use GAAP revenue in all of their SaaS metrics and analysis for comparability.

Example: Difference between Revenue and ARR

In the example below, a company closes a 12-month $120K SaaS contract that requires no implementation and has a fixed amount of user seats throughout the contract term.

On the day the contract is signed, they have $120K in ARR because that is the annualized contract amount. They continue to have $120K in ARR for that customer throughout the contract term (assuming no expansion or contraction).

GAAP revenue, on the other hand, is recognized over time and represents the amount of value delivered over the period of the contract.

When Growth Rates Shift Significantly

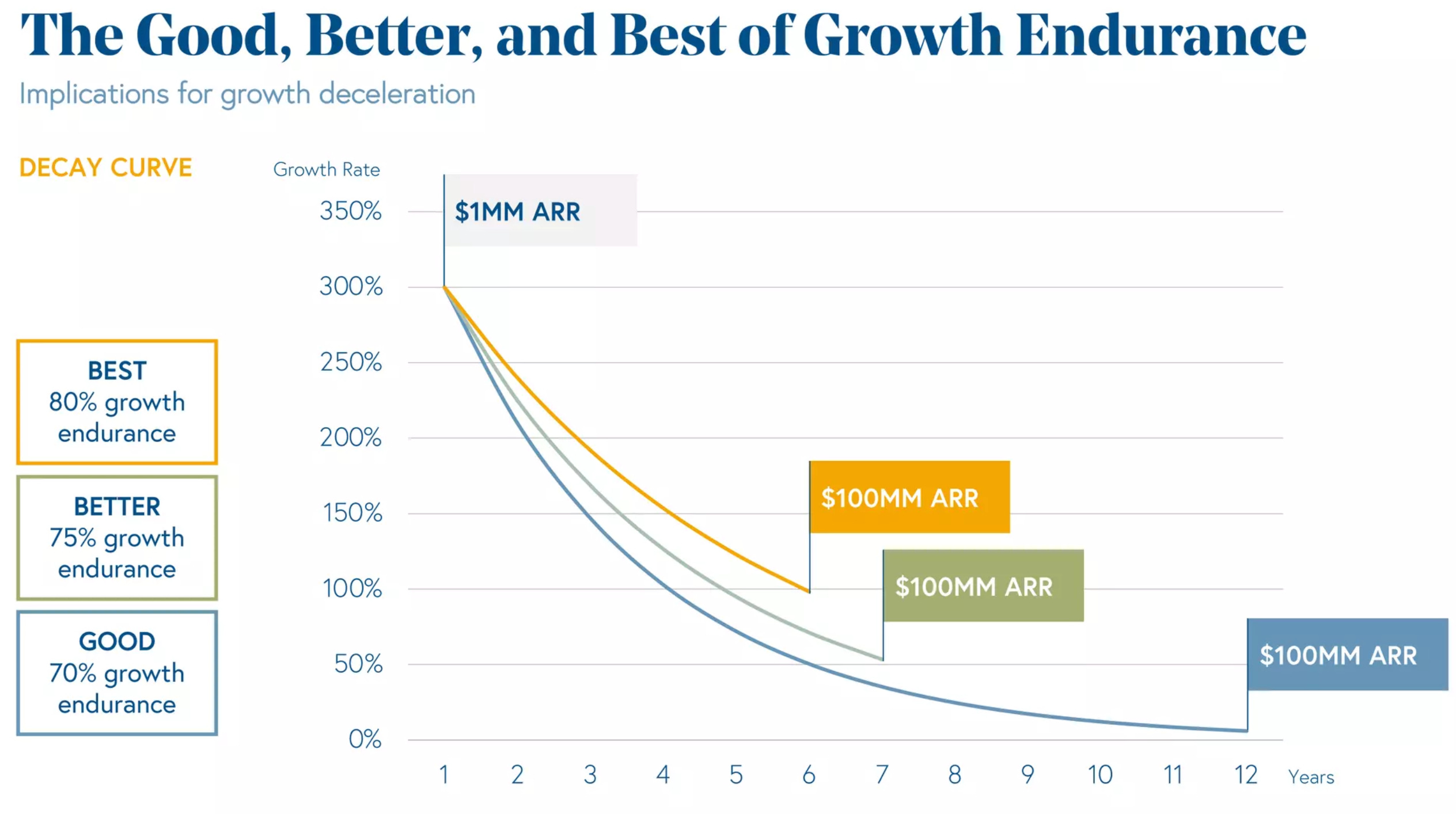

High growth rates have come relatively easy for a lot of SaaS companies for many years. And the durability of that growth has been consistently strong. The best companies have growth endurance rates of 80%+. This means if a company grew ARR by 100% this year, then next year’s ARR growth would be 80%. During the covid boost for SaaS, some companies even accelerated growth.

For most public software companies, the ARR growth durability has stayed within a fairly tight range year-over-year. But that is changing for a lot of companies right now as the new economic reality takes hold. Growth is hitting a wall and growth rates are falling.

When the growth rates shift dramatically, then the spread between ARR growth % and revenue growth % becomes large, which can cause other SaaS metrics that rely on growth rates to be misleading depending on which one you use and the direction growth is going.

Differences in growth rates during times of volatility

Here is a company that has strong ARR growth and even accelerates in year 2 from 90% to 120%. Then things normalize and it grows 100% the following year (83% growth endurance). But then growth hits a wall and is expected to only grow 50% in year 4 (this is 2023 for a lot of companies)

The growth rate difference of 17% between ARR and GAAP revenue in year 4 is caused by:

Revenue is a lagging metric compared to ARR

SaaS companies don’t typically close deals linearly throughout the year

Because GAAP revenue is a lagging metric compared to ARR, the GAAP revenue growth in year 4 lags the steep deceleration of ARR growth. Similarly, the revenue growth % doesn’t accelerate as fast as ARR in year 2 because most of the revenue recognized in year 2 comes from the previous year’s ARR growth.

Linearity of sales (i.e. how evenly are sales spread throughout the year) can also cause a major divergence between ARR vs revenue growth rates. The linearity I used in the example above (and likely not too far off from a lot of SaaS companies) is below.

Most SaaS companies have the largest amount of deals being closed in Q4. These deals contribute completely to ARR growth for the year, but very little to revenue growth. On the extreme, if a significant portion of deals were closed during the last week of Q4 (not as uncommon as you might think), then essentially no GAAP revenue would be recognized that year from those deals but all of the ARR growth would be reported.

Concluding Thoughts

Be careful with using different top-line definitions interchangeably, particularly as they are used within other SaaS metrics. For example, if you are looking at an efficiency score (i.e. Rule of 40) then the 17 percentage point difference in the example above is huge and can change how you evaluate the health of a company.

If high-growth companies previously focused on ARR growth but are magically shifting focus to revenue growth because of slowing growth (and GAAP revenue growth looks better) then beware…

For more tips on how NOT to get tricked check out my previous article below:

Didn’t expect the divergence between ARR and Revenue growth could become so wide.

Thanks for sharing this amazing article!

Great explanation of the differences between GAAP revenue growth and ARR and its various forms. This is very helpful for investors as we review reported earnings growth in different forms.