Most Common Accounting Mistakes

How accounting mistakes can screw up your annual plan

Sponsor: Redefine planning with Abacum’s AI-native FP&A platform.

Check out this guide for how the best CFOs more accurately forecast cash flow, runway, revenue, and expenses. It’s packed with practical examples and the details that software/AI companies need to forecast better.

Accounting Mistakes

Annual planning has a funny way of surfacing accounting issues.

Why are those costs hitting my budget?

Why is G&A so high?

Are we sure those costs should hit gross margins?

This vendor is used by the whole company…why is it only hitting my department?

The start of a new year (and your new annual plan) is a great time to fix these issues. No one wants to discover an accounting issue right after the annual plan is approved by the Board and then there is a variance with Plan for the rest of the year that has to be explained…

I am going to walk through the most common accounting issues I see. Some of these are accounting errors (not compliant with GAAP) while others are diversity in practice, which are also important to know when comparing to your peers.

Most Common Accounting Mistakes

There are LOTS of potential revenue mistakes that can be made so I will save most of those for another post, but I will cover a few below since many also impact expenses.

G&A Dumping Ground

I see this all the time. Even large companies. Why? Because G&A is the least scrutinized category since everyone just assumes it will eventually get to the right amount with scale.

Also, G&A is the default place to throw expenses if inexperienced accounting teams don’t really know where they should go. And then it’s hard to move it out after the expenses grow.

Don’t bury expenses in G&A…

What shouldn’t go in G&A?

There is a lot of stuff I’ve seen companies try to sneak into G&A, but below are a few usual suspects.

Stuff that should be allocated (more on this further below)

Facilities used by everyone

Software used by everyone

Large IT team that has lots of team members directly supporting other categories (like S&M)

Bad debt expense that should have been a revenue reduction

Company keeps recognizing revenue after the customer is clearly not going to pay (or there is significant doubt). Example: Six months into an annual contract the customer still hasn’t paid but the company keeps recognizing revenue for the entire year. What should happen is the company should put revenue on hold once there is substantial doubt about collectibility.

Company gives “concessions” on contracts because the customer is unhappy. This should be contra-revenue but they record it as bad debt expense.

What should go in G&A?

Finance, legal, HR, and other executive payroll-related costs

Corporate insurance

Financial audits

Charitable contributions

Protecting COGS

Show me the incentive and I’ll show you the outcome - Charlie Munger

Everyone wants to protect COGS so gross margins are higher given its importance in long-term valuations.

Here is what is generally included in COGS:

Hosting costs - AWS, GCP, inference, etc. for serving customers

Support team - Responding to customer support tickets

DevOps - People ensuring uptime and reliability of customer accounts

Customer success management (maybe?) - See below

Software and other costs for above teams

What are common mistakes?

DevOps - this is often just a part-time job in the early days so it’s in R&D and then it gets left there even as the team grows. This team is focused on maintaining customer uptime and reliability so it should be COGS.

Delivering services - Some of this is obvious, but it’s the more shadow services that often get misclassified. There is someone behind processes/software making it work. These people are often expensed to R&D and occasionally in S&M.

Customer Success Manager - see below

Customer Success Managers

I have written long posts about the categorization of these folks. Ultimately it comes down to what they are doing.

If they are just glorified support, then COGS. If they are driving retention, upsells, cross-sells, etc., then that sounds like S&M to me.

A great way to think about it is with the following question:

If you fired your entire CSM function, then who would take over their responsibilities?

Answer honestly.

If it’s your support or professional services team, then it’s probably COGS. If it’s your sales reps (or someone else in sales), then it’s likely S&M.

And often times the answer is a little bit of both. 50% in COGS and 50% in S&M (or something like that).

Infrastructure Costs

This is primarily costs like AWS, GCP, Azure, AI inference, etc…

These costs usually belong in the following 3 buckets:

COGS - Hosting and delivering services to customers

R&D - For the R&D team’s internal development work

S&M - Hosting and delivering services to prospects for free trials

Companies (especially earlier-stage) often dump this all in COGS or fail to allocate it properly across the above categories. Set up separate environments for each type so it’s easy to categorize.

Allocated Departments

There are certain expenses and teams that are generally allocated across all expense groups (COGS, R&D, S&M, and G&A) based on relative headcount or some other reasonable allocation methodology.

IT - People and software the entire company uses

Recruiting - Internal recruiting resources (sometimes this is just put in G&A)

General - Facilities, company offsites, etc.

This is one of the most common accounting issues. Even companies that get audited aren’t necessarily doing this fully right. I often see this come up during IPO preparation or M&A due diligence.

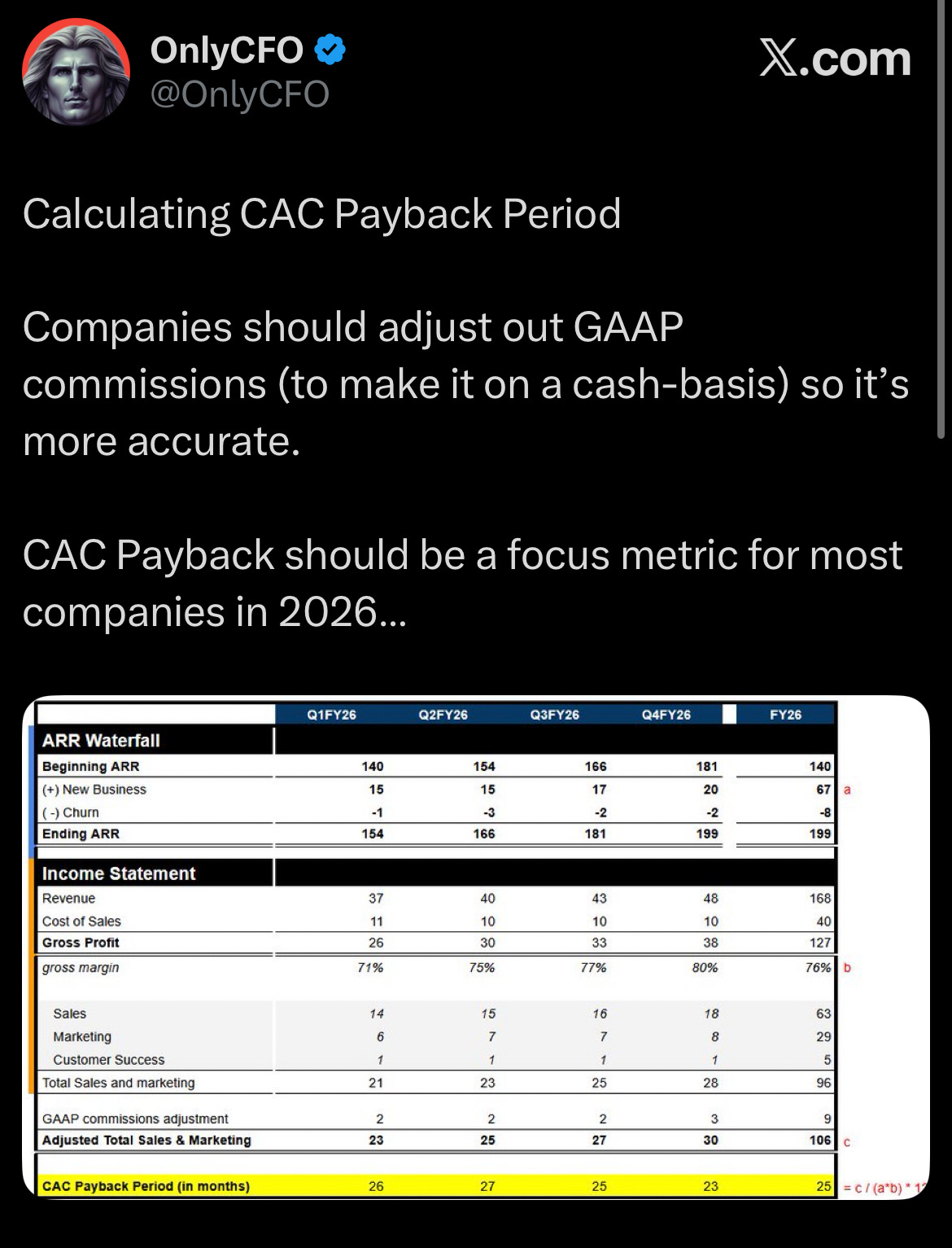

Sales Commissions

Most software companies are required under GAAP rules to capitalize sales commissions and then expense them over 3 - 5 years.

Many early-stage companies don’t do this. And large companies can have different amortization periods than their peers (3 versus 5 years can make a material difference).

Make sure to think about these differences when comparing to benchmarks.

Also, I always adjust GAAP commissions so they’re equal to commissions earned when I calculate financial metrics.

Final Thoughts

There are a lot of accounting mistakes (and diversity in practice) that can make benchmarking an apples-to-oranges comparison. This will also cause department leader fights in annual planning in FP&A.

Make sure your accounting is clean, or your leaders and board won’t trust you.

Correct these issues now for 2026.

Tell folks that it’s important to continue to improve accounting as you scale and that these changes are required under GAAP.

Don’t wait until you are deep in M&A diligence or prepping for an IPO…You will lose trust and it may materially impact the metrics.

Footnotes:

Download this guide (from Abacum) to better forecast and partner across departments.

Check out OnlyLawyer’s latest post. Are Legal AI companies toast?

Below is my cheat sheet for reading income statements of software companies.

The duplicate entry problem is way more common than people think. One trick: before every month-end close, paste your transaction list into ChatGPT or Copilot and ask 'find any duplicate or near-duplicate transactions.' Takes 30 seconds, catches errors that take hours to find manually. Prevention beats correction every time.