RIP Software? | Worst Sentiment Ever

The bears are coming out in full force and they are hating on SaaS!

Today’s Sponsor: Mesh Payments

Join OCFO and Mesh Payments CFO for a webinar on June 26th on the new CFO rules for fueling efficient growth. Sign up today.

This past week was one of the highest bearish investor sentiments toward software companies that I have ever seen.

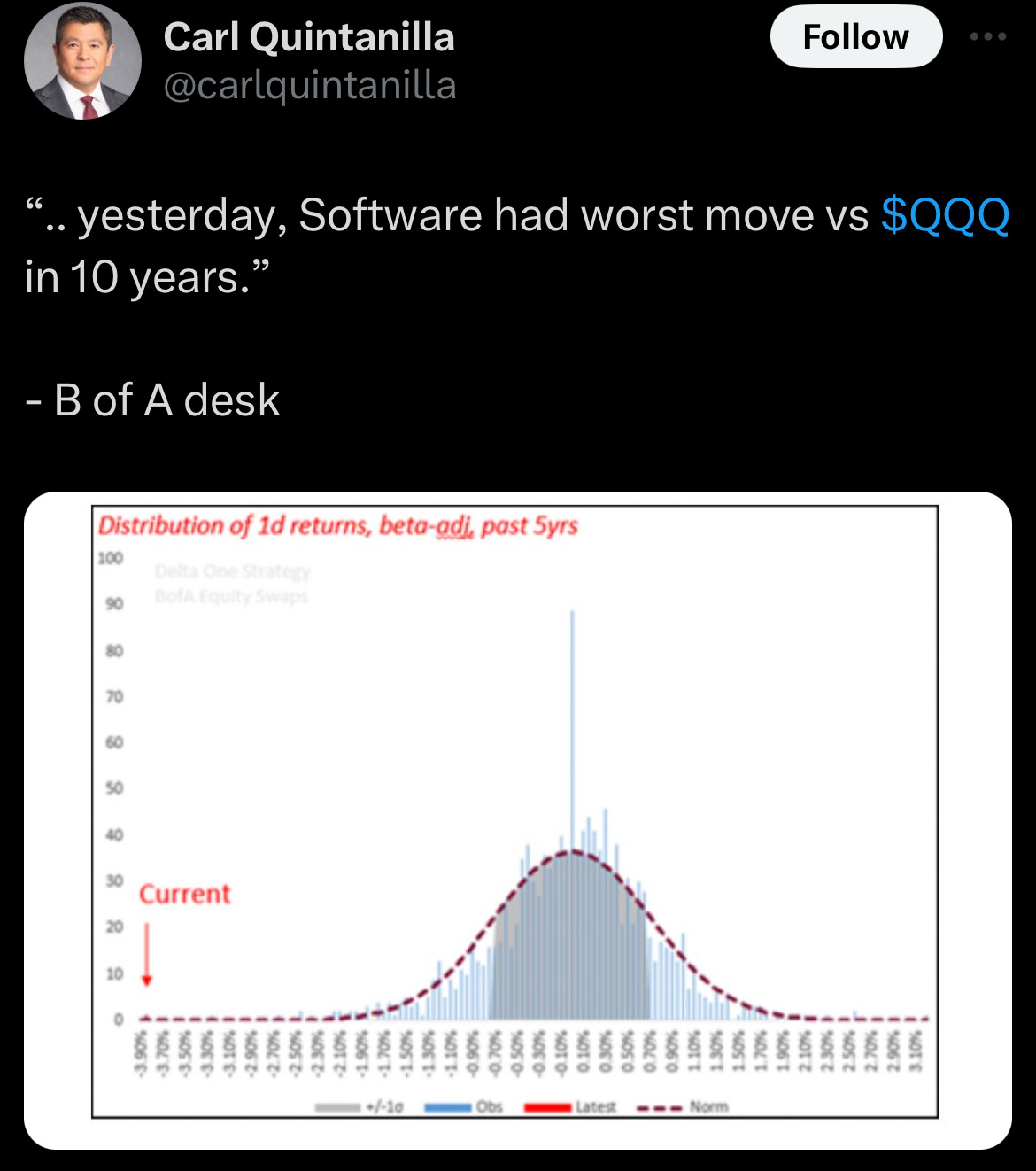

Thursday (May 30th) public software companies had the worst move versus the tech ETF QQQ in 10 years! In other words, software companies continue to struggle relative to the rest of the stock market.

QQQ is up 13% since the peak in 2021 and just recently hit all-time highs.

But the story is pretty different for cloud specific stocks. Public cloud stocks (using Bessemer’s cloud index) are still down 50% from the peak in 2021 and not that much higher before things went crazy in 2020/2021.

This past week a lot of big cloud names had massive stock price crashes following their earnings reports. Below are a few…

Salesforce fell 20% (first quarterly revenue miss in 18 years!)

MongoDB fell 24%

UiPath fell 34%

Veeva fell 15%

There have also been a lot of people on social media in the last week writing about all the things currently wrong with the software industry. Many were doom and gloom...

Why So Bearish?

Hopes of growth a strong reacceleration fading

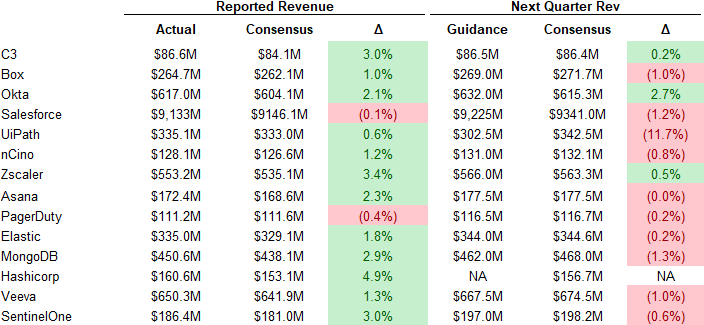

The companies with April 30th quarter ends starting reporting and things got uglier. As you can see below, most companies missed next quarter’s revenue guidance. UiPath missed expectations by a massive 11.7%.

There are still hopes of some revenue growth reacceleration for many software companies, but each quarter of flat or missed expectations puts that dream further out of reach.

A lot of software companies still appear expensive based on current growth estimates, so investors are expecting (hoping) that revenue growth will reaccelerate.

Fear of AI disruption killing the software model

The premise of software investing is that it can scale quickly and be extremely profitable at scale as a result of the premium that can be charged due to the difficulty of software creation. And that these companies can maintain those high margins over a longer period of time.

Generative AI may disrupt this though.

The fear for a lot of software companies is that AI will take the cost of software generation to essentially zero and therefore the premium charged will be wiped away over time as competition intensifies. This will be truer in some areas than others.

The higher software revenue multiples only make sense if companies can sustain high growth and high profits. If they get competed away in a couple of years then it is worth A LOT less.

Investing in AI

While there has been a lot of talk about efficiency gains that can come AI, we haven’t really seen it in the numbers of public software companies yet.

Everyone is investing in AI right now, which isn’t cheap. AI employees, Nvidia chips, compute resources, etc are all expensive. And all software companies don’t won’t to be slow to innovate in the new platform shift so they are all investing.

But…so far most companies are spending a lot on AI without meaningful revenue yet, which is keeping margins lower than expected given the slow revenue growth.

Big questions include: 1) will these investments pay off, 2) how durable is the revenue, and 3) how profitable that revenue will be (versus traditional software revenue).

Exit paths drying up?

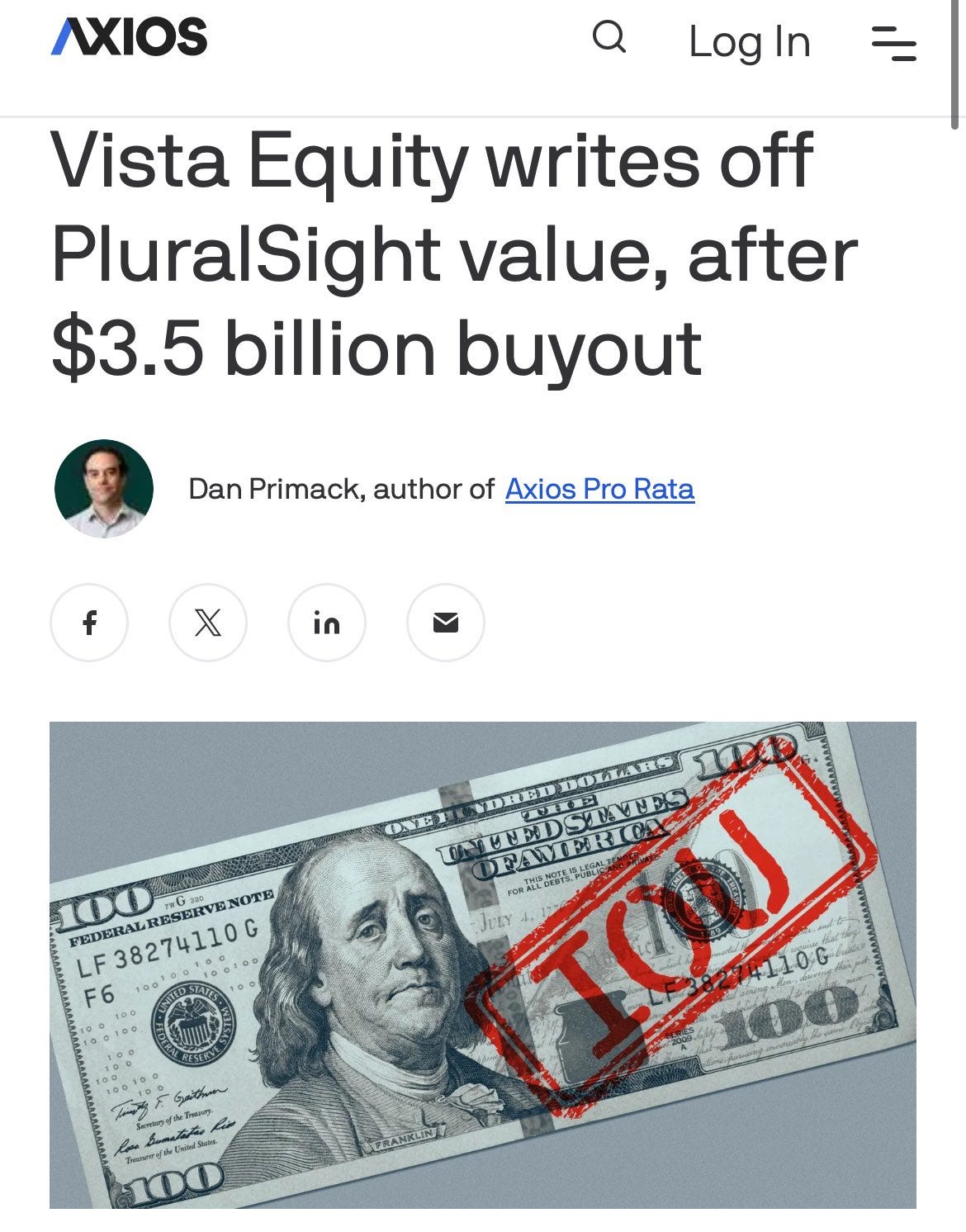

Private equity (PE) has been an important exit path for software companies. But the increased risk seen in headlines like the below from last week will slow these PE firms down.

PluralSight has some unique issues. EdTech is tough. But similar to many other software companies, disruption from GenAI continues to be a major concern. Also, PluralSight’s cash flow wasn’t enough to service its high amount of interest on its debt.

Final Thoughts

Software is not dead. But it certainly isn’t as easy as it once was.

Software companies across the board are getting punished right now. But it could be a good buying opportunity for some cloud companies that can adapt to the new environment quickly that you are bullish on.

Many software companies will continue to fail or be so upside down on their valuation that investors will never make money. The companies that are quick to adapt and innovate will still win though.

During times of high disruption and innovation, historical truths and benchmarks become less true. Those that don’t properly adjust will be disrupted.

*not investment, tax, or legal advice.

Footnotes:

Reply to this email if you are looking for bookkeepers or fractional CFOs that focus on tech.

My sponsorship slots are almost full for this year! Grab one of the last spots

I wonder how ChatGPT would have done relative to the analyst community with these names.

Not sure if you read this paper yet, but it was a good one: https://bfi.uchicago.edu/wp-content/uploads/2024/05/BFI_WP_2024-65.pdf

tl;dr the humans need the machines and the machines need the humans

It is isn’t dead it’s just going to the mature phase of the lifecycle of any industry. The end of the S curve - some will be able to jump to the next S curve (AI?) and continue but is still not clear how, when and who.