Software Buying Trends & Insights

Data from Vendr and a Q&A with their CEO, Ryan Neu

It is budget season for software companies so teams are coming together to build their financial plans for 2024. The past few years have been a roller coaster ride for forecasting revenue growth:

Early 2020 - we are all doomed 😱

Late 2020 - everyone needs software!

All of 2021 - party like it’s 1999! 🥳

Most of 2022 - maybe let’s party less and be efficient

2023 - AI will save us all. Maybe software buyers are ready to spend again?

Most of us have done at least one replan of our financial model in the past couple of years because our original plan was no longer reasonable. Replans that revise revenue growth down are hard. While you obviously expect less revenue, it also means you can spend less so you can manage efficiency and cash burn. This also means that the expected software purchases, new hires, offsites, etc gets cut (or pushed) from the budget as well.

As companies are going through 2024 planning right now most are being cautiously optimistic. Many software companies feel the pressure to show reaccelerating revenue growth to potential raise another round of financing. But no one wants to be inefficient or shorten their quickly diminishing cash runway unnecessarily.

The two cost areas that get the most attention:

People costs — typically account for ~70% of spend

Software costs - ~15-20% of spend

While I am not covering the people cost part of today, people are clearly the largest drivers of spend and where most of the efficiency and cost savings are located. But people and software aren’t totally separate decisions. The right software at the appropriate time can reduce people costs. Similarly the right people at the right time can best utilize the software and make the best spend decisions.

The remaining post will cover:

Vendr’s software purchasing trends/insights and commentary from me

My Q&A with Vendr CEO (Ryan Neu)

Software Purchasing Trends

The below Q3 software purchasing data comes from Vendr which is a popular procurement platform with a strong small to mid-market customer base so the data below may be biased toward those segments.

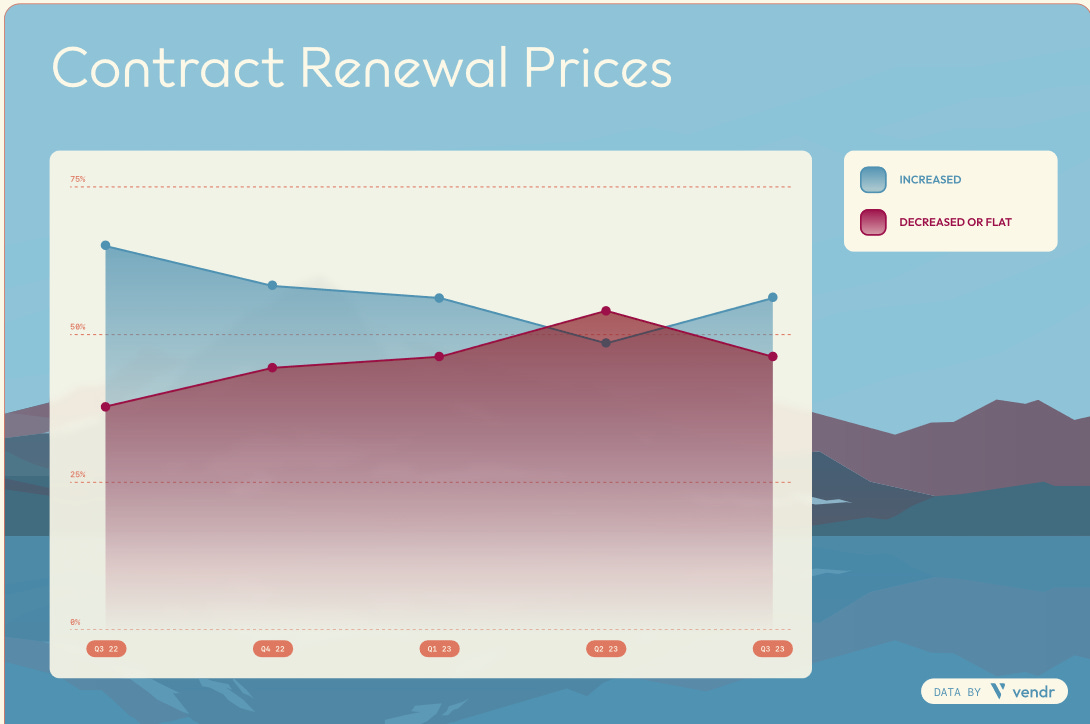

Contract Renewal Prices

The below image is a fairly zoomed out view on Q3 software renewals as it includes everything in the renewal price (price hikes, upsells, downgrades, etc), but what is clear is that companies are spending more on renewals.

Some of the bigger trends I am seeing that may explain these renewal prices are:

There is less room for optimization in existing software because a lot of the work to optimize has been done (processes fixed, layoffs slowed, and some hiring picking up again)

Renewal prices are increasing. Vendors are looking for ways to minimize the impact of churn so are raising prices

Consolidation plays are increasing renewals at larger companies with multiple products to upsell or expand across organization that are consolidating tools.

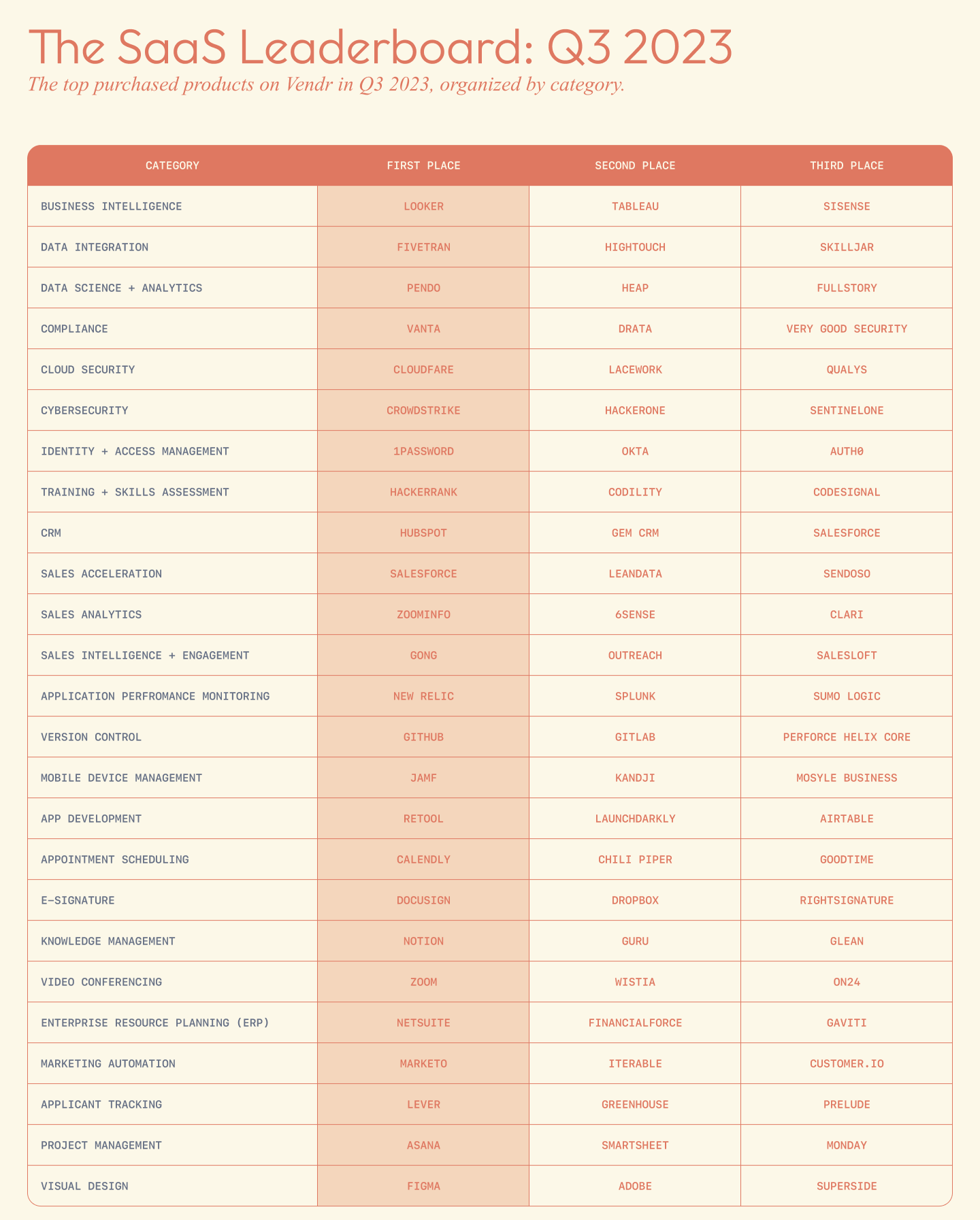

The SaaS Leaderboard: Q3 2023

The below image shows interesting data points on leading software purchases by category and the runner ups. With efficiency continually in focus, no renewal should be guaranteed. During the planning process for 2024, each team should scrutinize their software spend and consider things like:

Do we even need this software?

Our business and processes are much different from when we bought it

The tool was a nice-to-have and doesn’t add much value

We bought the software expecting we would eventually need it given prior growth, but the need is now 1+ years away

Is it worth consolidating tools to save money and complexity?

Do we have duplicative software used by various teams because of preference or small feature differences?

Can one vendor replace multiple tools? If it does 80%+ of what the current tools do then it may be worth the savings from consolidation

Can we cut software seats or usage?

Is there another vendor that does the same thing (or better) for less cost (or allows for more efficiency)?

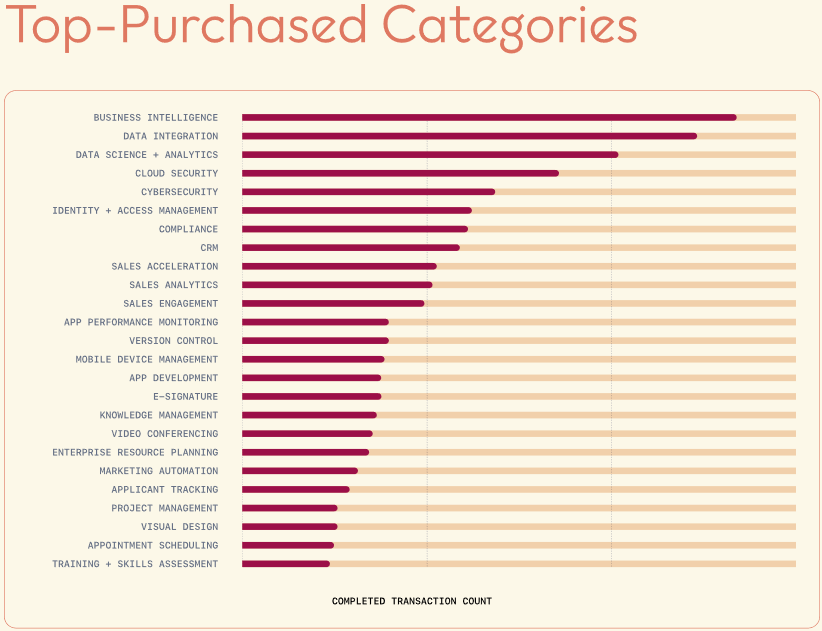

Top-Purchased Categories

While not necessarily a ranking of mission critical software vs nice-to-haves, there are some interesting trends here.

Full Vendr Q3 SaaS Trend Report here

Q&A with CEO of Vendr

I sat down (figuratively speaking) with the CEO of Vendr, Ryan Neu, to discuss Vendr’s business and trends he is seeing in the software procurement space.

Vendr helps companies save on SaaS. They accomplish that with some of the world’s best access to SaaS data, one-click access to negotiation experts, and an intake-to-procure platform to manage business approvals. They recently announced their Vender Intelligence Platform that uses their vast amount of software purchasing data to help customers save on spend.

Time for the Q&A…

You announced a huge $150M Series B in June 2022 at a $1B valuation. The fundraising market had started to shift at this point. Why were investors willing to make a big bet on Vendr?

Our investors recognized the consistent value we've been delivering, evident in the $300 million+ SaaS savings we've helped achieve with our customers.

While our valuation is indeed a milestone, it's more a testament to the immense potential we see ahead. Our core mission at Vendr has always been to ‘fix sales’, facilitating a transparent exchange of trusted data between software buyers and sellers. The result is straightforward: buyers access quality products without breaking the bank, and sellers acquire loyal customers without exorbitant customer acquisition costs. That's the holy grail in SaaS.

Like everyone else, Vendr has probably faced headwinds in 2023. What are you doing today and planning for FY24 to ensure you not only survive but come out stronger?

My dad's wisdom, "control your own destiny," rings true for Vendr now more than ever. 2023's macro challenges have made us double down on our strengths. In a world where every business is hunting for savings, we've carved a niche. And, tough times don't just bring challenges; they spotlight opportunities. Our approach is simple: do more with less, focus on our customers' most pressing needs, and ensure that the foundation of the business is strong — providing us with the time to accomplish Vendr’s mission.

As CEO of a high-growth company, what are the top financial metrics you review?

Metrics, for me, are twofold:

Scoreboard metrics

Play-calling metrics.

The scoreboard reveals our past moves' outcomes. It displays lagging indicators like MoM growth, NRR, GRR, and efficiency metrics, like gross margin. On a scoreboard, there's the clock, or free cash flow. If unprofitable, your runway. This clock ensures we have the time to make pivotal decisions to change the score.

That’s where play-calling comes in. We use leading indicators, like the number of workflows launched week over week, in order to gauge the pulse of the business. These are proactive metrics that allow us to zig and zag to change outcomes, rapidly. The strategy? Manage the clock, monitor the score, and make the calls. Repeat.

What's one finance related thing you wish you knew when you started Vendr?

If I could go back in time, I would double-down on customer cohorts. Imagine starting a farm where you initially only grow one crop. At first, it’s simple: you know what that crop needs and when. That was Vendr in 2018: a single product, negotiation-as-a-service. Treating every customer the same was natural.

But imagine if your farm started growing a variety of crops, each with unique needs. That's Vendr now. The key isn’t just knowing when each crop was planted, but understanding its specific needs. In the same vein, deeply understanding customers — not just by size or sign-up date but by their unique motivations and expectations — allows you to cultivate each relationship perfectly.

What are the top mistakes you see in procurement processes?

One major misstep in procurement is the reactive approach, particularly noticeable with the surge in SaaS purchases. Companies often engage procurement after a buying decision, missing out on valuable negotiation leverage. This reactionary stance adds stress, reduces efficiency, and hampers savings potential.

A shift towards proactive procurement is vital. When procurement is involved early, it not only ensures better deals but also allows security, finance, and legal teams to work cohesively. Early involvement means better decisions, streamlined reviews, and overall improved efficiency.

Vendr Insights

Multi-year deals: What data can you share on number of multi-year deals being done now vs 1 or 2 years ago. A lot of these are biting folks in the butt now. How does your team weigh the discount vs the commit? Any general advice on how to navigate?

Multi-year deals are on the decline, as CFO’s prioritize optionality. Vendr’s data shows that software buyers are 14% less likely to choose a multi-year agreement at time of initial purchase and 28% less likely to opt for a multi-year agreement at time of renewal, in 2023 compared to 202l.

In 2023, multi-year agreements offer an additional 13% average savings on net new purchases and a 26% increased savings upon renewal.

Where do you find the most software waste?

In identifying software savings, Vendr primarily examines two central metrics:

Pricing variability

Savings variability.

Pricing variability measures the inconsistency we see in SKU pricing across different contracts. To illustrate, our data has shown notable pricing fluctuations for platforms like Workday and Databricks.

On the flip side, savings variability provides insights into the potential savings one might expect with contracts from particular suppliers. For example, our data suggests that negotiations with LinkedIn tend to yield limited savings. In contrast, engagements with Netsuite often present a higher opportunity for cost reductions.

Any insight on consolidation trends?

SaaS consolidation is on the upswing. Our Q3 data indicates that only 17% of all transactions were new purchases, a decrease from 30% in 2022. This trend is largely fueled by two factors.

First, in competitive markets, there's a noticeable movement towards established, dominant incumbents.

Second, companies are trimming "nice-to-have" tools, even if they're feature-rich. Organizations are increasingly comfortable aligning with incumbents that might cover 80% of their needs, rather than juggling multiple suppliers. The message is clear: a surplus of features doesn't guarantee success in today's SaaS landscape.

What do you think (or hear) about what 2024 looks like for software buying? Are we at or near a bottom?

We didn't just predict 2023 as the year of the price hike — we nailed it. And this upward trend isn’t slowing down; expect it to dominate 2024. When growth dips, the cost doesn't vanish; it shifts. And the supplier won't bear it, the buyer will. This stark reality is driving software buyers straight to Vendr. We're their shield against surging SaaS prices.