Software Investors: Shoot First, Ask Questions Later

Just “pretty good” will get you killed in 2026

Brought to you by…Deel

For finance leaders, managing international payroll and compliance requires expertise. Our ‘Guide to EOR for Startups’ offers a detailed look at efficient global payroll management & compliance.

This guide will help you:

Manage cross-border payroll easily

Navigate tax implications across jurisdictions

Reduce financial risks associated with global growth

Take control of your financial strategy today.

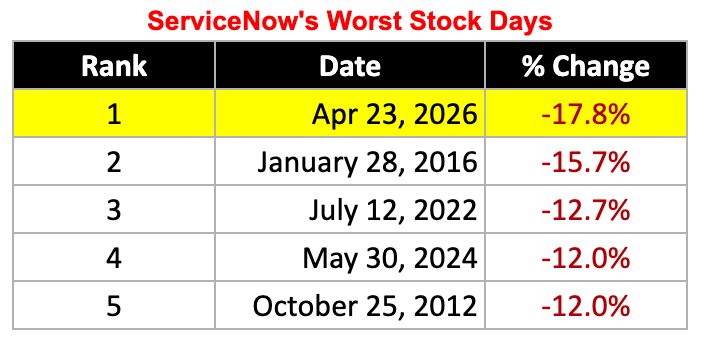

ServiceNow’s Worst Day…Ever

Three days ago, ServiceNow experienced the largest single-day stock price crash in its history (-18%). And it took the entire software industry down with it (software ETFs were down ~6%).

ServiceNow’s Q1 results must have been disastrous to send the stock down ~18%, right?

Nope. They were actually pretty good with a “beat and raise” quarter.

Quarterly Revenue: $3.770B (22% YoY growth) vs $3.745B consensus (+0.7% beat)

Adjusted EPS: $0.97 vs. $0.96–$0.97 consensus (in line to slight beat)

Q2 Revenue Guidance: $3.818B guidance vs $3.748B consensus (1.8% beat)

AI Momentum: Raised 2026 AI-related revenue target to $1.5B (from $1B).

In more ordinary times, you’d think the stock might be up (or at least flat) with those results. Certainly not down 18%.

But that is not the environment software is in today. ServiceNow’s results were just “pretty good” and the story wasn’t super clean…

Software Investors in 2026: Shoot First, Ask Questions Later

The stock market is not always rational (especially in the short term). While ServiceNow was down nearly 18% on Thursday, some investors realized on Friday that maybe this was a buying opportunity and sent the stock back up 6.5%.

Every software investor has their finger on the sell button and is just looking for a reason to press it. Any reason…

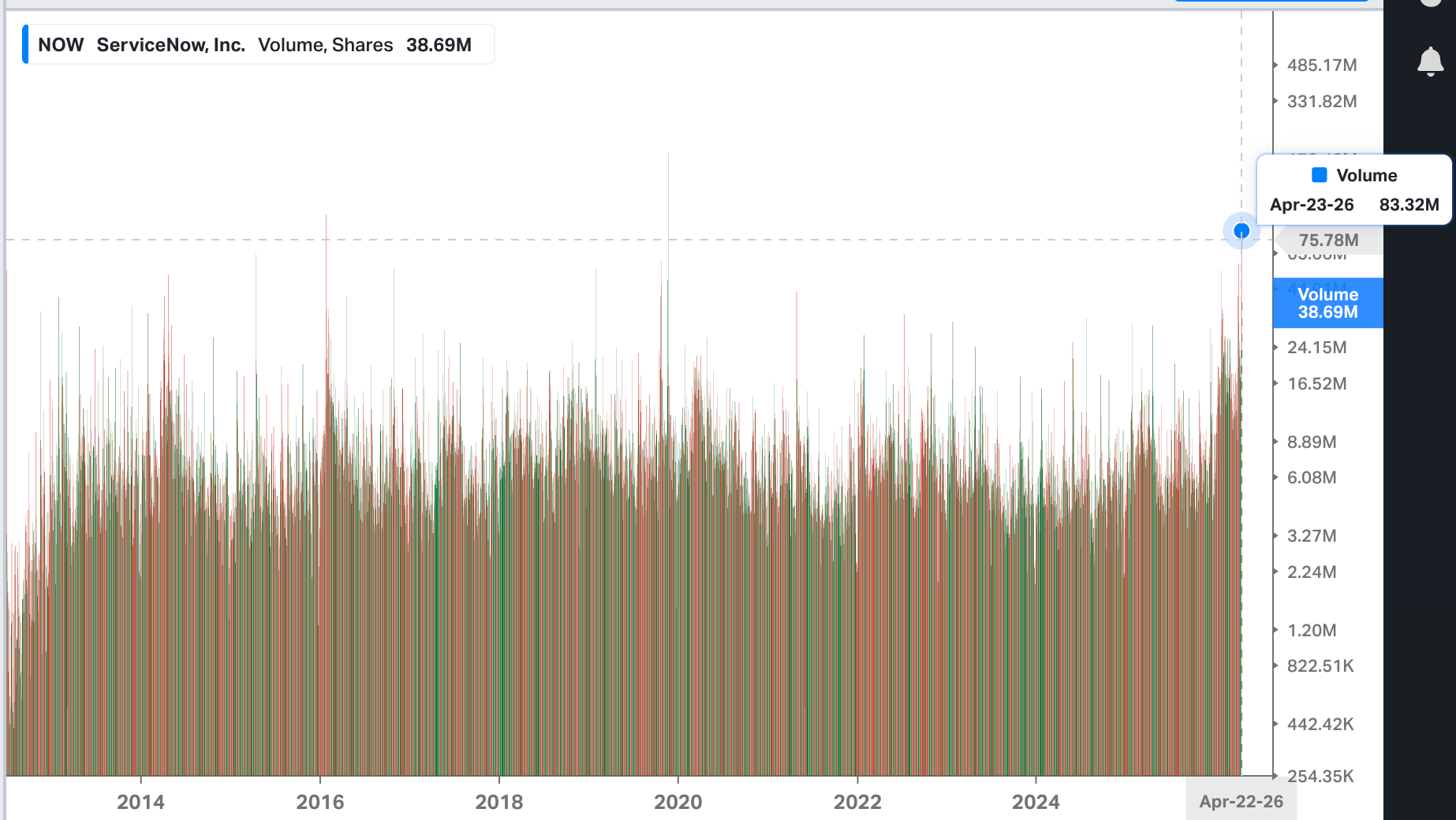

On Thursday, there were 83M ServiceNow shares traded, which has only happened a couple of times prior in the history of the company.

There are two related things that got ServiceNow shot by investors:

“Pretty good” doesn’t cut it in 2026

There was noise in the financials/story

Anything other than clean, stellar performance is interpreted as “AI is killing the business”. Software investors are looking for reasons to say you are going to get wiped out by AI. And if you look for something hard enough, you will find stuff that supports the “AI just wiped out [X] segment of software” thesis.

And ServiceNow’s results and story definitely gave the thesis room to grow:

Is AI destroying their pricing power? Q2 non-GAAP operating margin guided at ~26.5% (well below Street expectations of ~30–31%)

Is there really just a timing issue or is growth just slowing? Management said there was a ~75 bp headwind to subscription revenue growth from delayed on-prem deals in the Middle East due to the conflict in Iran.

Are they truly winning with AI or mostly just cannibalizing their legacy revenue? Q2 revenue guide was disappointing given the Q1 beat. If they are a major AI beneficiary then why is overall growth not stronger?

Is ServiceNow buying growth via M&A because organic is quickly weakening? ServiceNow’s $7.8B acquisition of cybersecurity company Armis closed in Q1 and had a noisy impact on results and forecasts.

Bill McDermott, ServiceNow CEO, mentioned their “beat and raise” a couple of times on the earnings call. Below is how I heard it in my head, lol.

C’mon guys…We just beat and raised. Why are you giving us such a hard time!

In the Q4 earnings call Bill actually said the below in response to ServiceNow supposedly dispelling organic growth fears:

I noticed that we lost about $10 billion in market cap on that because of the worry. So now the worry is gone, you can give us back the market cap. — Bill McDermott

Moral of the story?

By default, software investors want to sell. They are looking for a reason. They are practically begging for it. And it’s causing all software names to take a hit.

Not all software or their AI story is created equal, though. For instance, the ones that win in the long term may see earlier short-term pain as they aggressively rebuild for the AI world.

The broad-based fear selling might create some buying opportunities…

Is ServiceNow Cheap Yet?

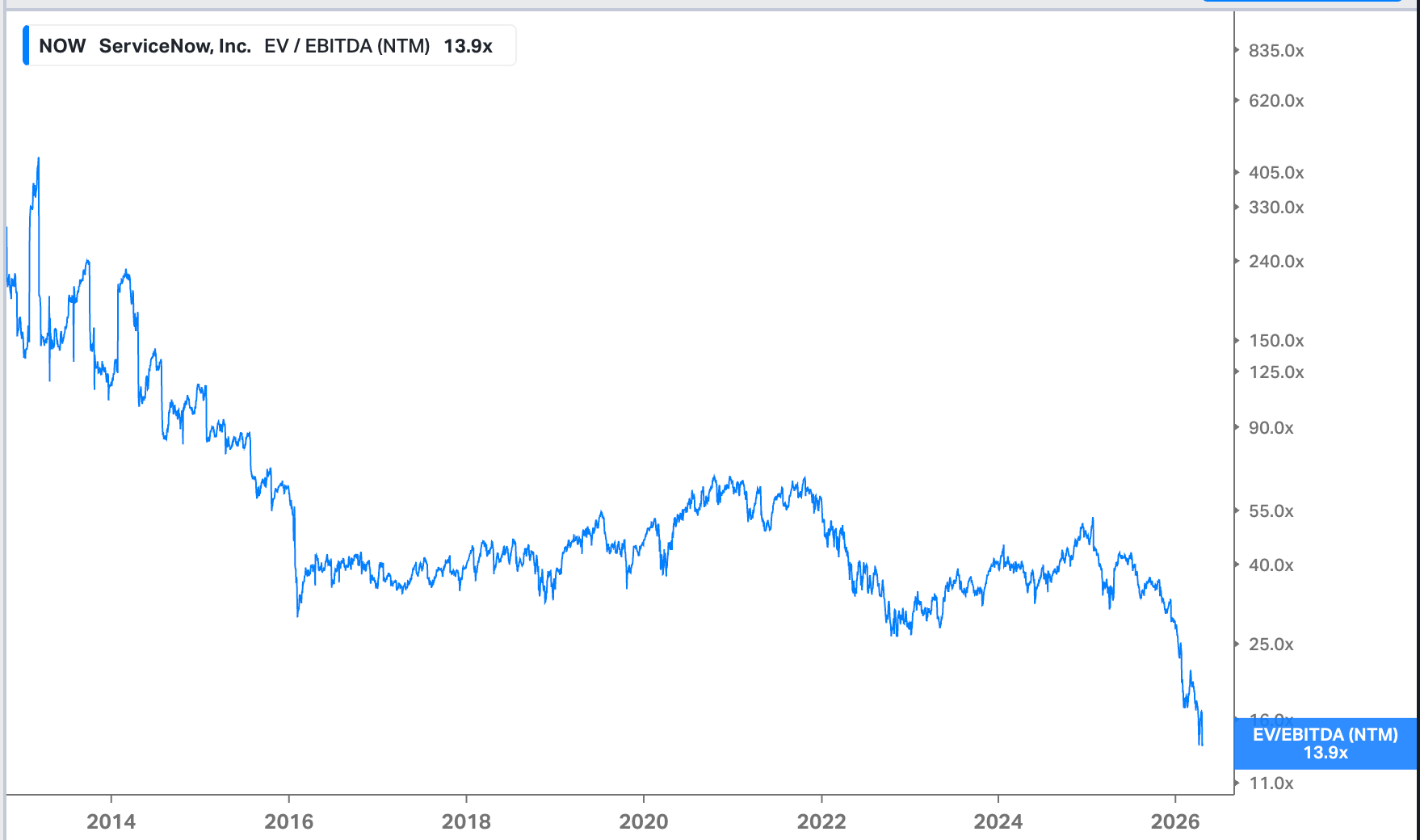

As a multiple of EBITDA, ServiceNow has never been cheaper. By a long shot. Part of that is simply being a more mature business, but they are still one of the fastest growing public software companies AND they are the 3rd largest in revenue scale.

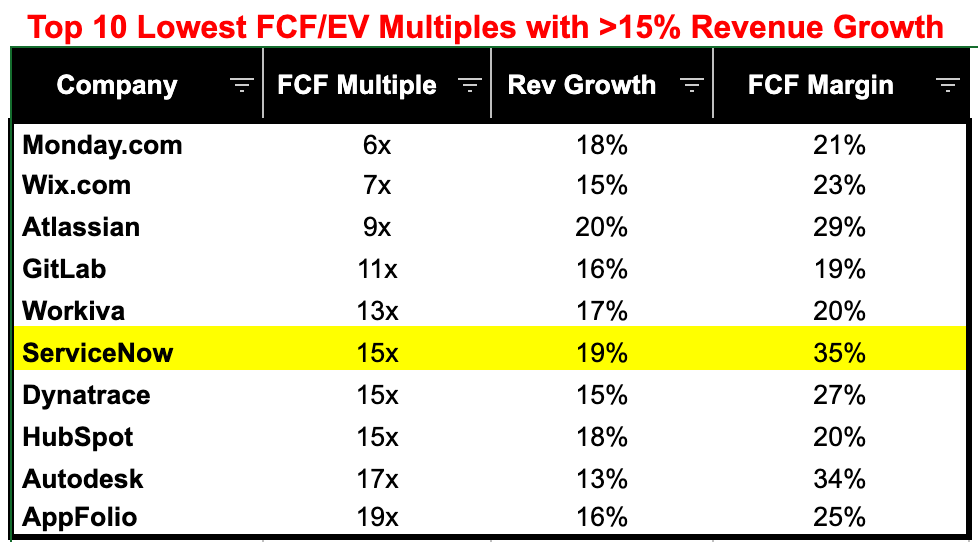

ServiceNow’s FCF multiple is the 6th lowest FCF/EV multiple for companies growing revenue >15%.

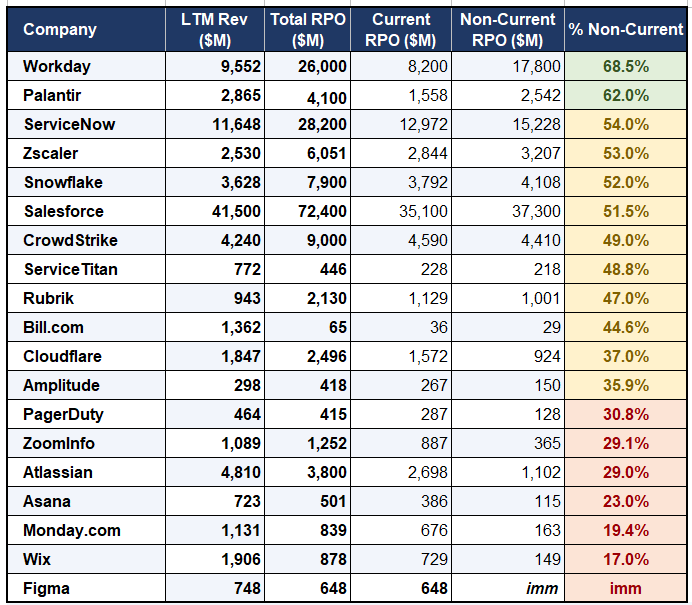

And ServiceNow has one of the highest RPOs of any public software company. They have about two years of current run-rate revenue locked in under contracts.

But the bajillion-dollar question is:

What companies get disrupted by AI versus what companies become more valuable because of AI?

Problem is that 90%+ of legacy software probably sits in the first bucket. And the 10% may temporarily look like losers with cracks in their story as well as they rebuild to become AI winners.

The AI Story: Nothing Else Matters

If a company doesn’t have a clean AI story (with financials to back it), then investors will shoot first.

But in order to create a long-term AI story, companies may need to walk in front of a firing squad. They may take some flesh wounds along the way, but it might be necessary for them. And it could present a potential buying opportunity for investors if the company can become an AI winner.

But many stocks will become “cheap” for a reason. The terminal value goes to zero. And if that is true, it’s hard to be cheap enough for investors to not lose money.

Some folks like to say the following about building companies: “It’s a marathon, not a sprint”. But that is likely bad advice today…if you are not sprinting toward an AI story then the rest of the race may not matter.

Footnotes:

Check out the EOR Guide. It’s a must-read if you have international employees or are thinking about expanding more internationally.

Want to sponsor? Email onlycfo@onlycfo.io

📚 This Week’s Interesting Things:

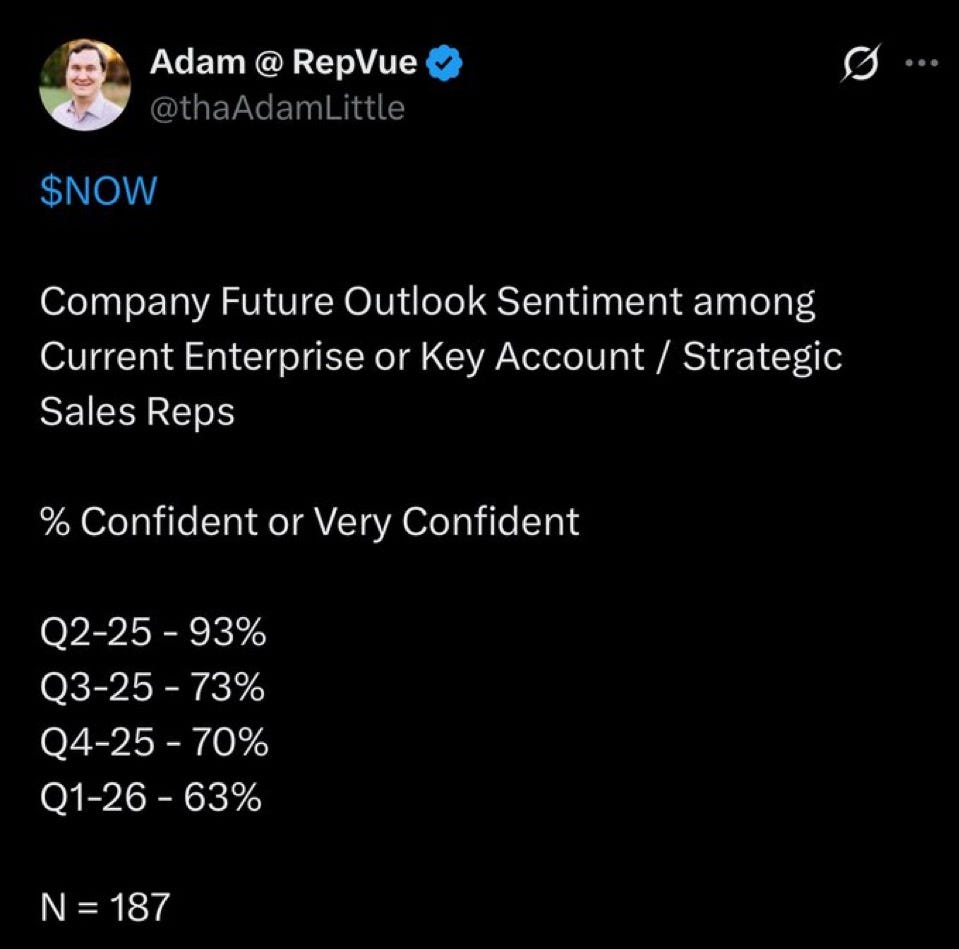

Insane how fast sales rep sentiment has fallen at ServiceNow…sales reps are the closest to the customers and what they are saying/doing so it’s usually good to listen to them.

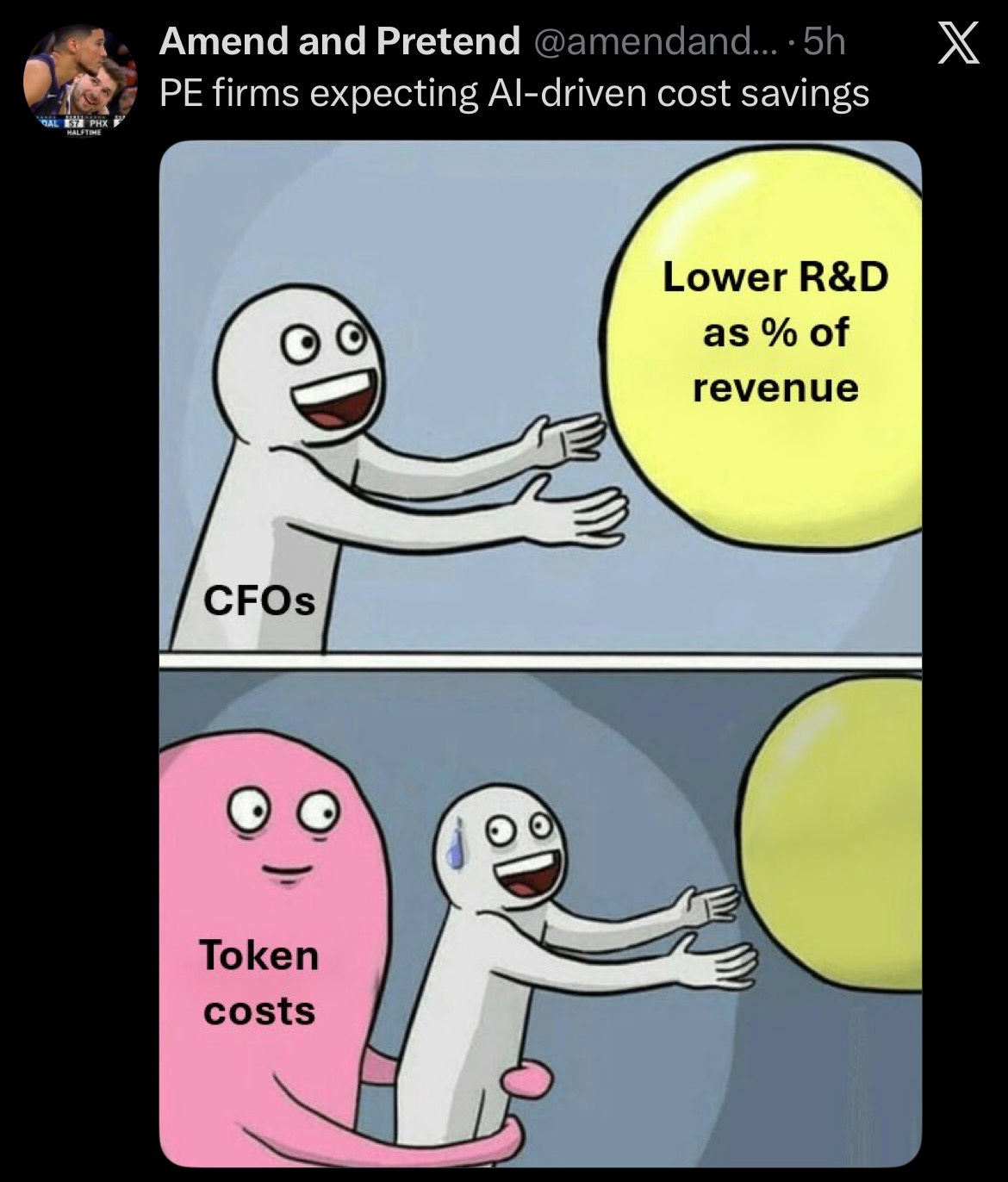

I feel this one deeply…those additional token costs got to come from somewhere. And it’s headcount.

ServiceNow beat AND raised and still dropped 18%. That's the market telling you clearly that in 2026, showing up with strong numbers isn't the same as showing up with a clean AI story. The new bar for software is not "did you grow" but "did your AI narrative tighten." Any software name without a crisp, defensible AI angle is getting re-rated regardless of results.

That sounds right until “pretty good” becomes the warning sign.

In this tape, the business can beat while the story loses permission to trade at the old multiple.

That’s where valuation stops being forgiving.