Software’s Top Winners and Losers

How has public software companies performed since peak 2021? How have IPOs performed?

Brought to you by…Brex

AI agents in finance are really powerful when they have the right context, controls, and operating environment.

I (OnlyCFO) have been working closely with Brex for over 2 years, and what they’ve built for agentic finance (AF) is incredible. With Brex, agents handle all the tedious stuff, like expense reports, policy enforcement, and month-end close, so your team doesn’t have to. Check out Brex AF!

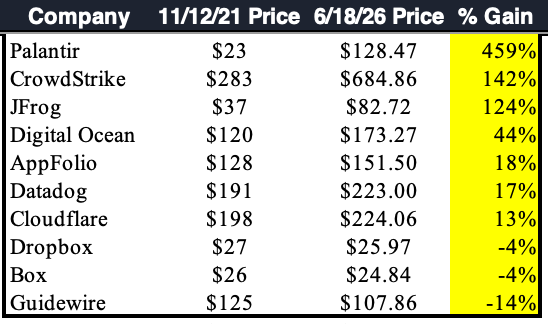

Stock Price Performance

Only 7 out of 75 public software companies have a higher stock price today than 5 years ago (peak of software valuations in 2021). Unless you invested in one of the top 3 performers, you underperformed the broader market…

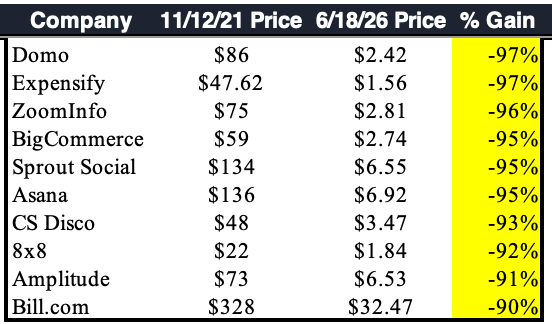

And the biggest losers were really big losers… The bottom 10 all lost >90% of their value. Domo leads the pack at a 97% loss.

IPO Performance

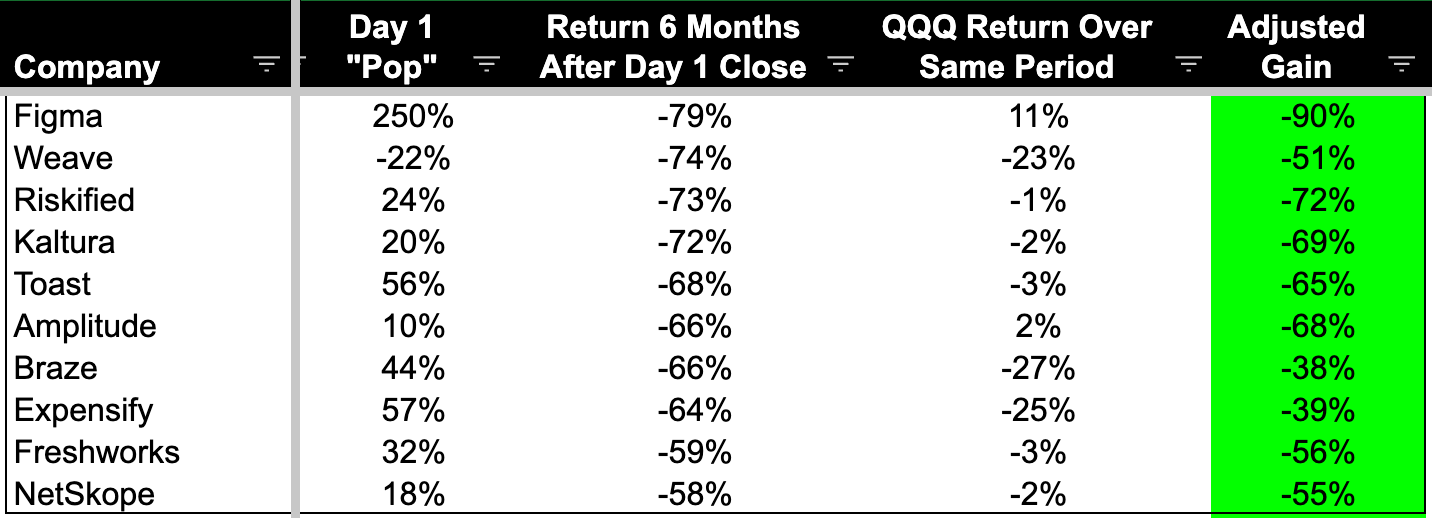

IPOs can be wild rides given the excitement around them and the extremely low float (ie the number of tradable shares).

SpaceX went public last week and saw its stock price increase by ~70% within a few days (a trillion-dollar increase…). But since that peak SpaceX stock has fallen over 20%.

History says that buying on the IPO day (when publicly traded) is a bad investment. The average software IPO was 5% lower six months after the IPO while the broader market was up over 6% over those same time periods…

Biggest IPO Losers

Figma, for example, had a massive 250% day 1 pop (one of the largest in history). Just six months later though Figma was down 79% while QQQ (tech-heavy market ETF) was up 11%…If you invested in Figma on day 1, then you are worse off than the broader market by 90% (green column)

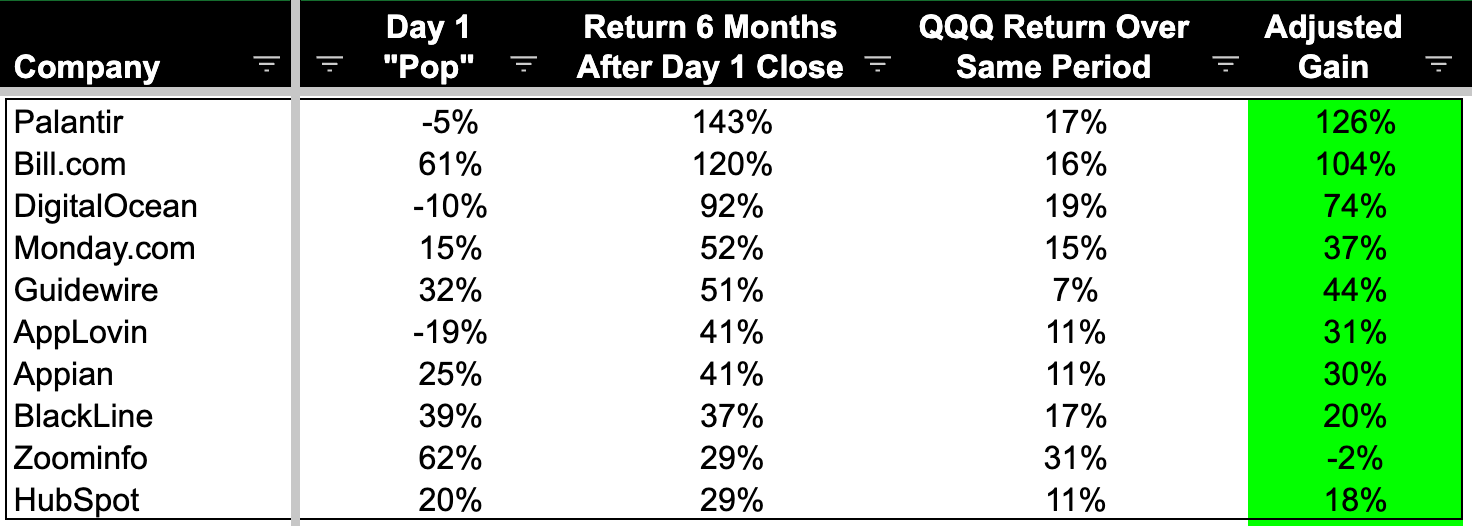

Biggest Winners

Funny enough, the biggest winner (Palantir) didn’t IPO. They went public via a direct listing. Shares slid on the first day, which is very unusual, and then it turned out to be a major AI winner.

Revenue Multiples

Revenue Multiple = Enterprise Value/Revenue.

And “revenue” is either LTM (last 12 months), NTM (next 12 months), or sometimes ARR (which is something in between LTM and NTM).

If revenue multiples increase, then stock price almost always goes up for software companies (because revenue doesn’t typically fall).

But revenue multiples can fall while stock prices increase. This happens when revenue growth outweighs the decline in revenue multiple, which is exactly what every software company has been fighting to do since the sky-high revenue multiples of 2021. AppFolio, for example, had its revenue multiple cut in half, but its stock price is up by 18%. This is really hard to do!

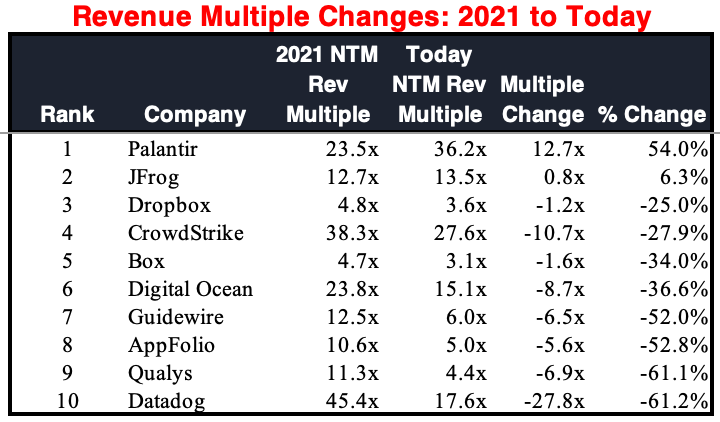

Top 10 Revenue Multiple Changes

Below are the top 10 increases (or smallest decreases) in revenue multiples from 2021 to today. Only two companies actually increased their revenue multiples since 2021… Palantir is obvious, but JFrog surprised me.

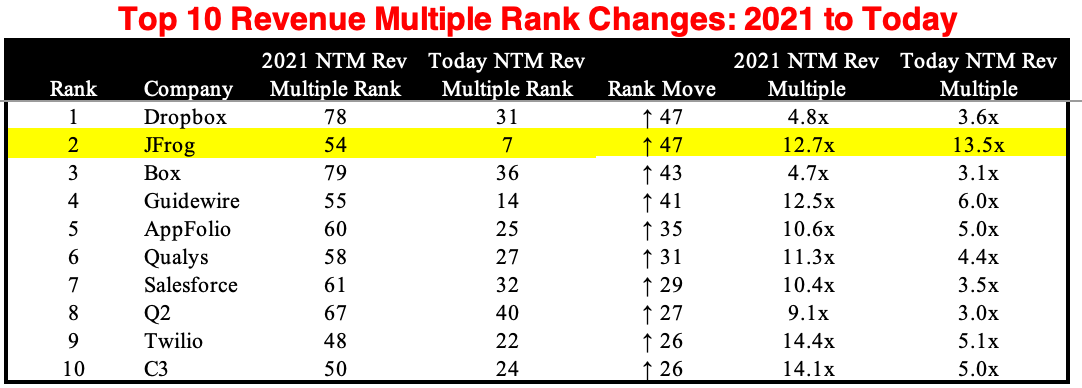

Top 10 Revenue Multiple Rank Change

I like to see the trend in relative revenue multiple ranking. In the table below I ranked all software company revenue multiples in 2021 and compared them to the rankings today.

JFrog had the second highest relative revenue multiple change since 2021 (jumping 47 spots) and it now sits in the top 10.

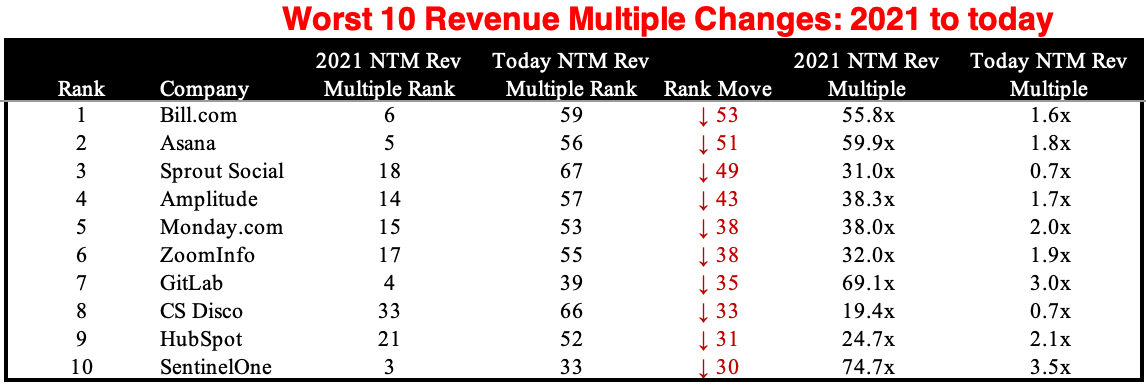

Bottom 10 Revenue Multiple Rank Changes

The biggest revenue multiple losers generally come from the companies that experienced the weakest revenue durability (see next section).

BILL leads the pack here. It’s really hard to recover when your revenue multiple goes from 56x to 1.6x….Most of these companies have been deemed AI losers which helps explain the massive multiple drops.

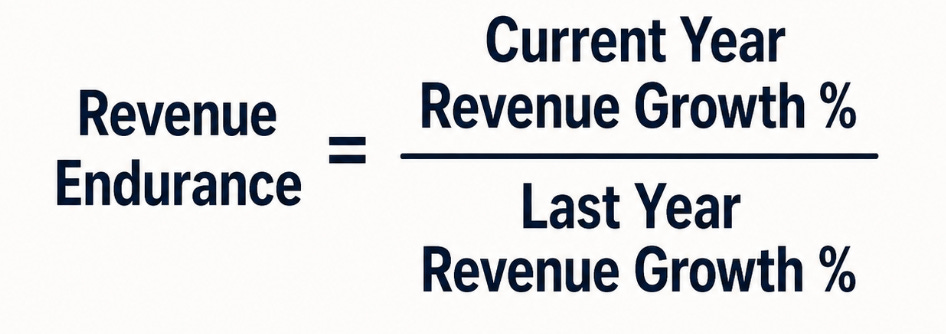

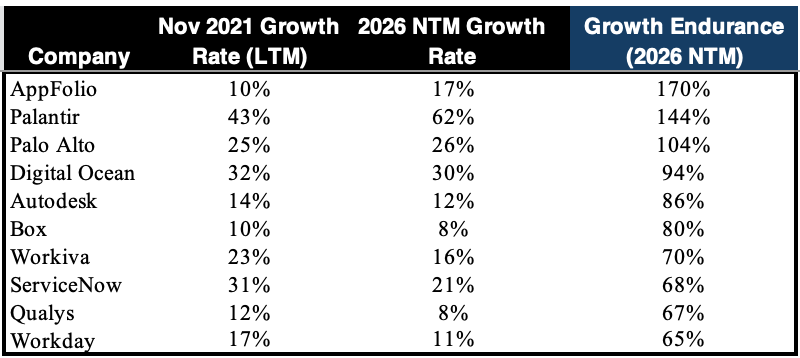

Growth Endurance

Growth endurance measures the stickiness of your revenue growth over some period of time (usually measured annually).

Top 10 Best Growth Endurance

Below are the companies with the best revenue growth endurance over the past 5 years.

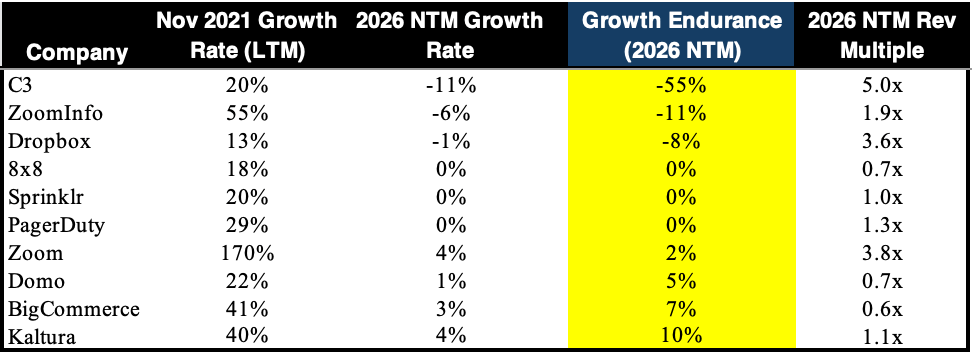

Top 10 Worst Growth Endurance

C3 tops the charts for worst growth endurance at -55%….I don’t really follow the company at all, but it blows my mind that C3 is trading at a 5x revenue multiple with negative revenue growth. I guess people are still grasping onto hope that it has some AI that will magically make them grow again and be profitable.

The higher multiples for Dropbox and Zoom make sense given how profitable they are (and Zoom’s early investment in Anthropic helps too)

Gross Margins

Should gross margins be increasing or decreasing?

All else being equal, higher gross margins is obviously better. Gross margins represent the ceiling of profitability. So we want gross margins high, right?

Well…the counterargument is that if companies are implementing AI in a meaningful way then gross margins will likely come down (at least near-term) since AI is more expensive to run. If the tradeoff truly is slightly lower gross margins for significantly better revenue growth durability, then I will take that trade every single time. But it’s usually not that simple.

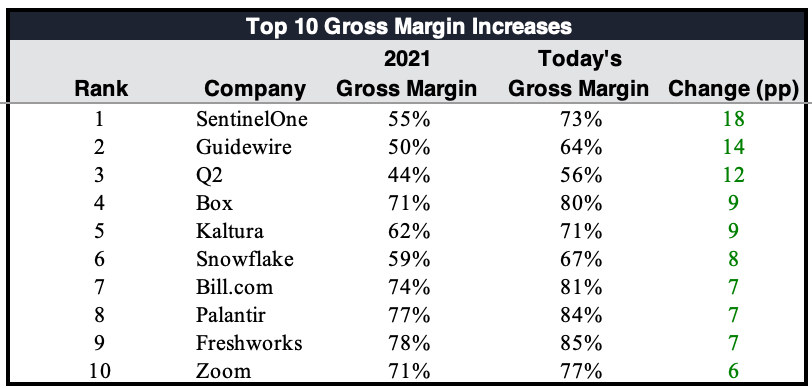

Top 10 Gross Margin Increases

Most of the companies below that saw the largest gross margin increases also saw their growth rates decrease the most. When growth rates decline, companies start to prioritize fixing things like low gross margins. It’s also easier to have better gross margins when revenue growth is slow.

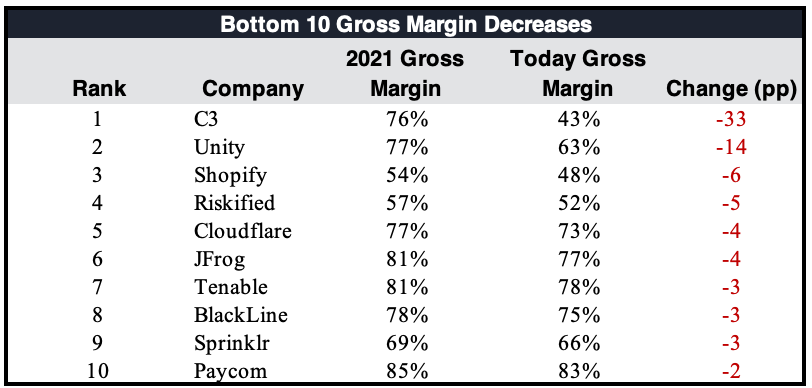

Top 10 Gross Margin Decreases

C3 has seen an absolute disaster of gross margin deterioration (falling 33 percentage points). I know they are an “AI” company, but…that isn’t what explains this…

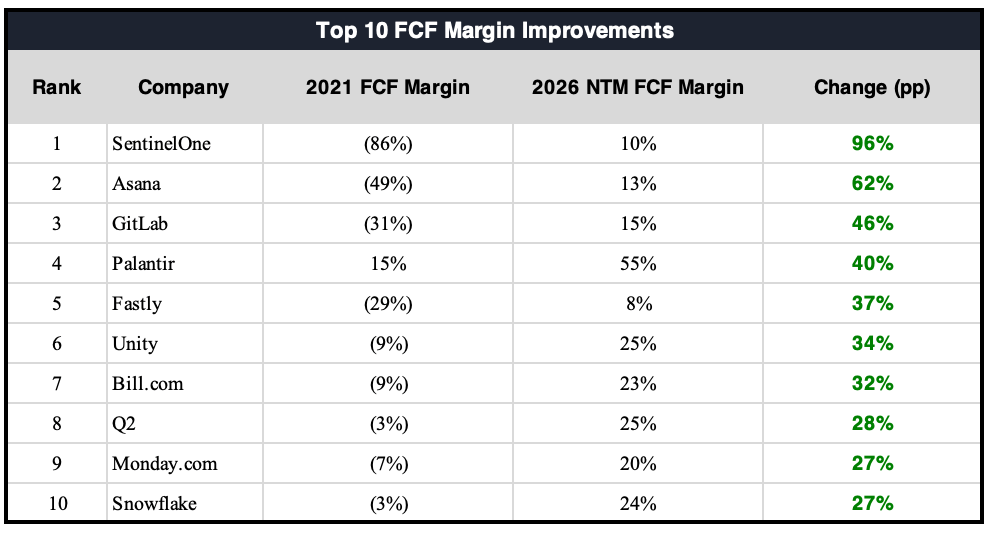

FCF Margins

The biggest improvements came from some of the very worst starting points back in 2021. SentinelOne increased 96 percentage points because it started at a -86% FCF margin 🤮. It’s now at a 10% FCF margin, which is good progress, but it still isn’t very good if it can’t keep improving FCF margins as growth rates fall.

The most impressive FCF margin improvement is Palantir…It’s the only one that started positive.

One reason why the Rule of 40 can be a misleading metric is because it assumes all companies can eventually trade growth for FCF margins. Many have proven that they are pretty terrible at doing that.

Footnotes:

See how Agentic Finance can transform your finance department (today’s sponsor is Brex).

Subscribe and share the OnlyCFO newsletter with your teams

*nothing in this post is investment, tax, or legal advice

Shopify had a stock split. Their stock performance since 2021 has actually been fairly strong, even hitting new highs earlier this year.

Great insights!