The Downside of Secondaries

How secondary transactions are sneakily costing you lots of money

Spend smarter and move faster with Brex, today’s sponsor.

Meet your AI mandate faster. Facing more pressure to accelerate AI’s impact on your finance operations? The CFO’s Guide to AI Strategy is your free roadmap. You’ll get 5 best practices to fast-track AI adoption and turn high expectations into big results. Like “eliminate 60% of manual finance work” big.

The Rise of Secondaries

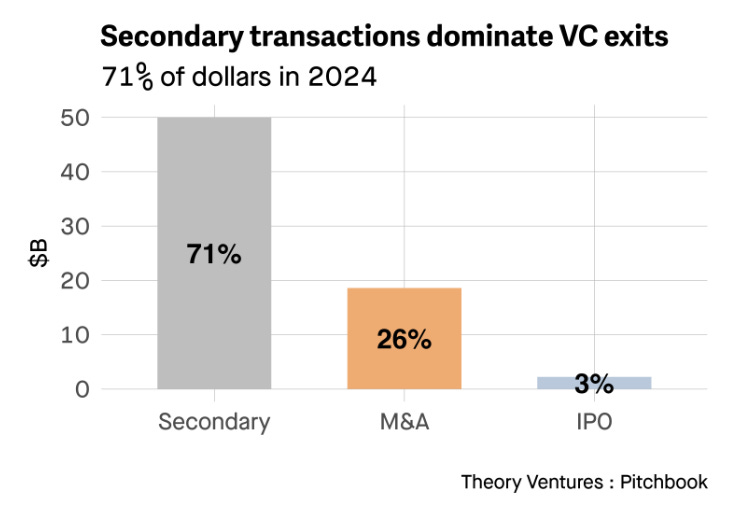

There has been lots of discussion recently about the rise of secondaries and their importance for VCs in 2025 and beyond. The dominance of secondaries for VC exits has exploded in recent years as the IPO markets have essentially been shut and the M&A environment has also been pretty weak.

I am going to publish a few posts on the general topic of the changing landscape for VCs, company fundraising, secondaries, etc, but I want to start with an impact of secondaries that most folks don’t talk about.

The negative impact of secondaries has personally cost me lots of money…And it may also be costing you lots of money — without you even knowing.

What is a “secondary”?

Transactions where an existing shareholder, like an investor or employee, sells their shares in a pre-IPO company to another investor.

There are two primary types of secondaries that this post is about:

Direct Secondary Sale

An individual (employee, founder, or investor) sells shares directly to another investor.Tender Offer

The company arranges for a group of shareholders (usually employees) to sell a portion of their shares to a buyer or group of buyers at a set price.

There are also indirect secondaries that have a different impact (which I will cover in a future post). I care less about these as an employee, but they too also have important implications.

LP-stakes

Ownership shares that investors (LPs) have in a VC fund, which can be sold on the secondary market.

Continuation vehicle

A new fund that buys select assets from an old fund to give GPs more time to manage and exit them.

Secondary Trends

Secondary transactions have significantly increased in volume over the last 5 years. GP-led secondaries used to be almost non-existent.

There used to be a strong stigma against GPs selling shares in companies before an exit (IPO or M&A). But given the longer timelines to exits (and liquidity crunch right now), GP-led secondaries have become much more popular.

What happens when secondary market transactions increase?

When a bigger market exists for secondaries and there are platforms that make it easy then there will be less of a discount from the last fundraising round for secondaries. Also, obviously a lot of AI excitement is fueling a smaller discount as investors just want to be able to get into the hot AI companies.

While secondary transaction volume is fairly concentrated in the hottest private companies, if secondaries become more popular and easier to do then it generally means increasing prices for those secondary transactions.

In other words…employees/investors get to sell their shares for more money!

What’s the downside?

This all seems positive so far, right?

Investors, employees, and founders are all getting liquidity and they are selling at increasingly better prices. That’s awesome!

But…there is a significant downside of secondaries that most people don’t know about.

Secondary sales typically impact the 409A price of common stock.

A 409A valuation is an independent appraisal of the fair market value of a private company’s common stock. This valuation is based on guidance and standards established in section 409A of the IRS’s internal revenue code.

A 409A valuation is NOT done by your investors and does not necessarily represent how they would value the company. The purpose of the 409A is to determine the value of common stock so that stock options and other equity awards can be granted to employees appropriately (and meet IRS rules).

409A must be performed at least annually or when a major material event happens (like a fundraising round). Larger companies closer to an IPO will start doing them more frequently (semi-annual and eventually quarterly)

How do secondaries impact 409As?

409As determine the common stock price by potentially weighting several different indications of company valuation:

Public market comps (using valuation multiples like revenue or EBITDA)

Discounted cash flow model

Recent fundraising rounds price

Other market transactions that may indicate a valuation (such as secondaries)

409A providers will look at all of these valuation indicators and assign a weighting to each one based on their belief on how strong of an indicator it is.

Example: When a 409A is completed immediately after a fundraising round then typically the valuation is primarily weighted toward the fundraise price. But remember that VCs get preferred stock so the 409A will look at that price and “backsolve” to get to a common stock price for the 409A.

When there is no recent fundraising round then it might be an equal weighting across all of indications of value.

Common stock of private companies also receive a significant haircut for "discount for lack of marketability” (DLOM). The haircut related to the DLOM can be significant but if there is an active secondary market then this starts to go away a lot earlier.

Lower 409A Price = Good

A low 409A price is a GOOD thing. Many people don’t get this, but employees want the lowest 409A price possible because it means new grants have a lower exercise price, which means less money they have to pay to exercise stock options (and the more money they potentially make in an exit).

The common stock price per the 409A is always lower than the preferred price (what VCs pay) because of the protections and preferences that preferred stock gets.

The 409A price of common stock can be up to an ~80% discount to preferred stock in the early days. And then as a company scales and gets closer to an IPO the prices start to converge.

But secondary sales can really screw this up for employees by eliminating a lot of that discount of common stock — making the upside potential much smaller.

The $ Impact of Secondaries

Price: As mentioned earlier, when secondaries are sold at a hot company then the common stock price can get bid up a lot closer to the preferred price. And the issue is that the secondary transactions’ price will likely be A LOT higher than what the other 409A valuation methods indicate.

Weighting: How much weighting a 409A puts on secondaries depends on factors such as transaction volume, who participated, and how long ago the secondary occurred. Weighting may be as small as like 5% for small number of transactions that happened several months ago to 100% for a large tender offer sale.

Either way, secondaries are increasing the 409A price. Often significantly.

These secondaries are great for those selling, but bad for all new hires and other people getting stock option grants afterwards.

Example: An executive friend joined a later stage company recently and was granted ~2M stock options at a ~$2/share exercise price. He later found out that there were a significant number of secondaries 3 months before he joined (right before they updated their 409A)….And if those secondaries didn’t occur the exercise price would have been ~$1.50. Secondaries will cost him $1M ($0.50 difference * 2M shares)!

Is my company doing secondaries?

If you are at a super hot company then there is a good chance there is a somewhat active secondary market and those sales are already screwing up your 409A.

Most companies don’t have an active secondary market, but a small number of secondaries might still be happening that almost no one knows about (often kept pretty secret). Two common examples include:

Founders (and very early employees) selling some in connection with a fundraising round.

Large stock option holders (typically VPs and execs) leave a company and are facing a huge cost to exercise and a large tax bill so they work with the company to sell to current or new investors.

Employees don’t know these are happening but they might be massively increasing the 409A price on all future grants.

Final Thoughts

Secondary sales are a double edged sword for employees:

When you want to sell you love them

When you want an equity grant you hate them

If the secondary market continues to expand then the built in upside for employees will continue to shrink.

While I love the liquidity for employees that comes from secondaries, I hate the impact it has on all future employees and equity grants.

Footnotes:

Download the Brex 2025 Survey

Join the next OnlyCFO Webinar on how the definition of ARR is change and how you should adapt. You won’t want to miss it!

Check out OnlyExperts to find offshore accounting resources. They have some amazing talent for 20% the cost of a U.S. hire

This is super informative. Thanks for sharing.

In most cases aren’t hot/larger companies that have a high volume of secondaries, issuing RSUs at that point? Or do some still prefer issuing options?