The ARR to Cash Leaky Bucket | Build This Bridge

You will be surprised at what you find. Read to the end to get my free bridge template

Brought to you by…Paraglide

My teams have always spent way too much time on billings and collections...chasing customers, sending reminders, providing additional detail, etc. It’s high-volume, boring, and repetitive. Which is exactly why it’s a perfect place to use AI agents.

Have my friends at Paraglide tell you what AI agents can do in accounts receivable.

Paraglide helps businesses get paid on time with AI agents that automate billing and collections conversations in the finance inbox. AI agents respond to billing queries, send personalized payment reminders, track commitments, and manage disputes, removing the bottlenecks that delay payment.

The ARR → Cash Bridge

You are missing out on critical information if you are not bridging ARR to cash based on actuals. Every finance team should be doing it. Many are not…

Few things make a CFO (or CEO with their board) lose credibility quicker than not being able to truly explain the movements between:

ARR (or revenue run rate)

GAAP revenue

Cash collected

A couple of months ago I asked a CEO why their GAAP revenue as a % of ARR had decreased so much over the past 2 years. It was pretty gradual so I don’t think they noticed. It was a 3 percentage point drop, which was $1.5M in revenue that disappeared….What caused it? They dug in and created a bridge and realized they were gradually giving away a lot more free months at the beginning of the contracts. These free months weren’t counted against ARR but must count against revenue.

A few reasons to create an ARR → Cash Bridge:

Discover leaky ARR that doesn’t turn into cash

Help fine tune forecasting assumptions

Understand if any policy changes need to be made (too many credits, bad debt, free months, etc)

If you want to get acquired, diligence will be MUCH easier if you have this ready. Conversely, if you are acquiring a company then make sure to get this.

Helps significantly with your financial audit

The goal of this bridge is to see how ARR turns into cash. I break the analysis into two separate models:

ARR → GAAP Revenue

GAAP Revenue → Cash

The first one is usually more art than science. It’s OK if it doesn’t reconcile exactly because you are usually using high-level assumptions.

GAAP revenue to cash is more of a data exercise where you should be able to get pretty exact. My accounting team always puts this together for our auditors and it makes the audit so much easier. And it also significantly helps my FP&A team with their forecasting.

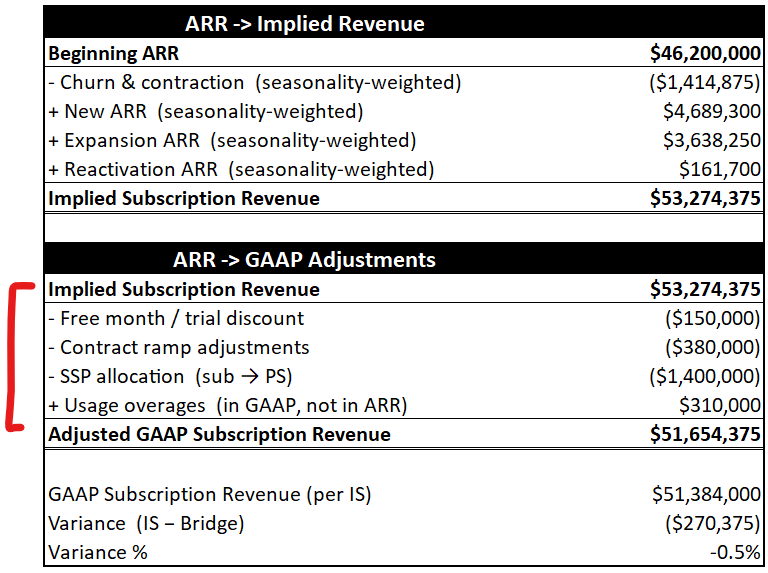

1. ARR → Revenue

Your FP&A team should be factoring all of these things into their forecasts, but not enough companies actually calculate it retrospectively:

The adjustment section (highlighted in red) is the hard/important part

Breaking out the adjustment detail helps find process/policy issues

Updating this analysis regularly highlights changes that might get hidden in FP&A’s forecast vs actual review

Makes the CFO’s job explaining the movement a lot easier (builds confidence)

Because of the seasonality of ARR (when new ARR gets booked) and that ARR is usually defined as the most generous topline number, GAAP revenue is almost always lower than ARR.

2. Revenue to Cash Bridge

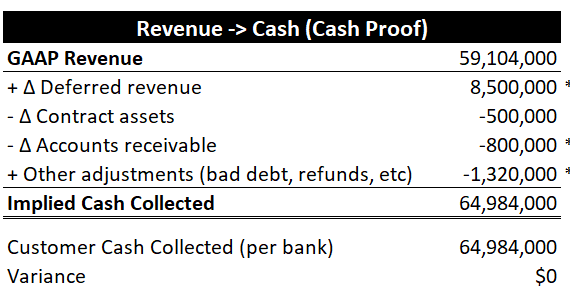

Below is a high-level summary of a Cash Proof (revenue to cash bridge). I will explain each of the components further below.

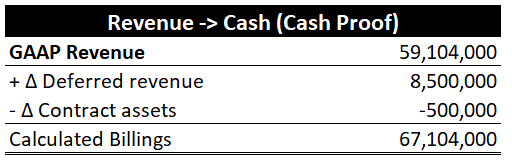

Calculated Billings: The first two adjustments of the Cash Proof are “calculated billings”. It’s a common software metric for public companies so investors can estimate how much was billed to customers in the period based on the information they have. Private companies should also track this metric because it’s a good sanity check on your actual billing data. I prefer to just report calculated billings at private companies if they are close.

Deferred Revenue: When you bill your customer upfront it gets added to deferred revenue. If deferred revenue is increasing, then you are billing faster than you are recognizing revenue. Which means more cash to collect.

Contract Assets: This is where the company has the right to invoice (revenue has been recognized), but they haven’t invoiced yet. This is subtracted because it’s the opposite of deferred revenue….revenue is recognized but we haven’t billed for it so we can’t collect cash yet.

Accounts Receivable (AR): Next you have to subtract the change in AR. Just because you billed it doesn’t mean you collected it. So by subtracting the change in AR you are reducing the amount you added for billing above by how much of that increased billing wasn’t collected.

Other Adjustments: This is where you find the surprises and where you want to pay attention. The biggest one is typically bad debt expense. Bad debt means you recognized the revenue, billed it, and it’s not in AR…but you didn’t collect any cash because it was written off from AR to bad debt expense.

💡 If you want to collect more cash (for less cost) then check out the collection and billing AI agents from Paraglide. Obvious place to leverage AI agents. They are today’s sponsor.

Here are a few other common things to watch out for when building this bridge:

Sales Tax: You need to remove sales tax collected from your total billings number and your customer collections per the bank. It’s not your money…

Gross vs. net presentation mismatches: An example of this is when a payment processor like Stripe nets fees before remitting. Your bank shows net cash but your revenue was gross.

Foreign currency translation adjustments: When multi-currency lines are converted at different rates than what was booked you will have a difference if there are material changes.

Bridges Create Understanding

Your team should be building these two bridges. If they are not, start today.

Revenue → Cash Bridge: Accounting team owns

ARR → Revenue Bridge: FP&A owns, but needs help from accounting

Once you put it together, it is pretty easy to maintain. It’s important to understand all the leaky bucket items that prevent ARR from dropping to cash collected. I promise you will build more trust with all stakeholders if you do…

3 Things From The Week…

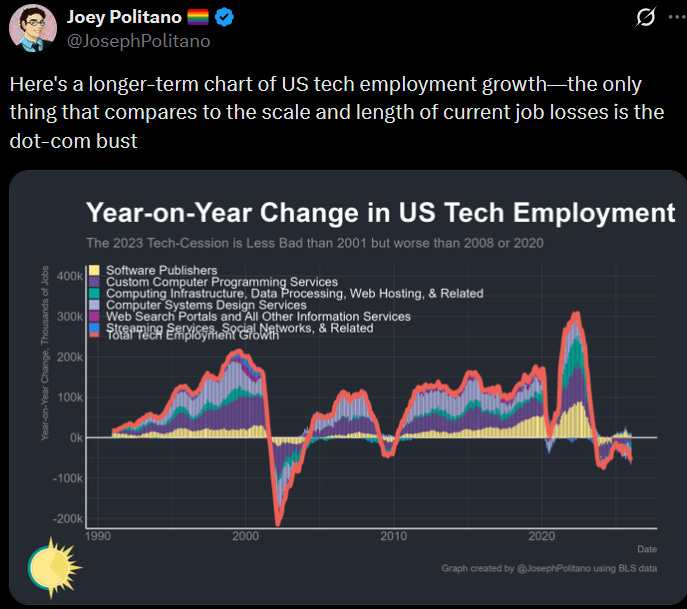

YoY change in tech employment is down A LOT. We had a big hiring pull-forward, but it has now fallen beyond that and is getting worse.

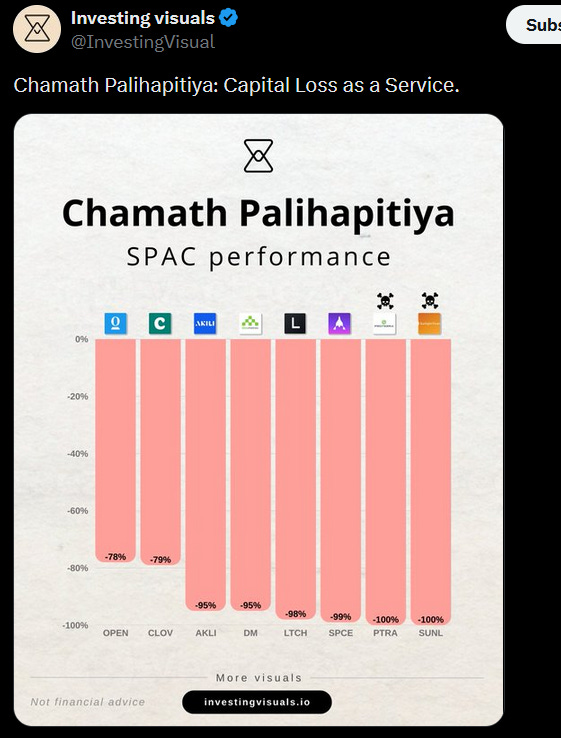

Chamath told one Twitter user (who was complaining about his losses from Chamath’s SPACs) to post their tax return of capital losses and he will reimburse the losses. So is anyone who invested in them getting free money? ha

In the second image below you can see how 8 of Chamath’s SPACs have performed. There are plenty of people who lost money…

Chamath also told another Twitter user to thank him for generating capital losses that he can use to offset future capital gains 🤣

Anthropic put out data around what they believe is the theoretical capability vs observed exposure of AI by occupation. There are more AI use cases finance teams (and everyone else) should be implementing!

Footnotes:

Want to learn how AI agents can transform the finance department? Make folks like Paraglide teach you.

Want my 1) revenue to cash and 2) ARR to revenue bridge templates? Shoot me an email at onlycfo@onlycfo.io.

Want to sponsor this newsletter? Send me an email