The Only Path Left in Software | Accelerate or Die

The penalty for being mediocre has never been greater…

Brought to you by…Paraglide

I (OnlyCFO) recently took a demo with Paraglide and it blew my mind. My team has been wasting incredible amounts of time on billing inquiries and back-and-forth with customers on collections.

Paraglide can automate the majority of this work. It’s high-volume, boring, and repetitive so it’s a great place to leverage AI. Talk to my friends at Paraglide and see what accounts receivable AI agents can do.

What Paths Remain for Software?

David George (GP at a16z) wrote an article titled “There Are Only Two Paths Left for Software” where he argues that there are only two paths left for durable equity value creation (down from 3 paths):

Accelerate revenue by 10+ percentage points YoY (through AI-native products)

Messy middleof slower growth and not very profitableRebuild the company to 40-50% operating margins (including SBC)

I agree that the “messy middle” path leads to certain death (of equity value) in 2026. For the past 10+ years, the messy middle path still often turned into a decent outcome (usually via acquisition by PE). But those days are gone. PE isn’t coming to rescue you.

So that leaves two remaining paths…

However, I take a more aggressive stance. There is really only one path remaining. Any other path will be destructive to long-term equity value.

The Profitability Path Still Ends in Tears

Lots of companies are trying to get on the profitability path. It’s the natural thing to do for companies as their growth has significantly slowed. But there are two potential traps that most folks on this path fail to grasp:

They are actually on the messy middle path (which is an even worse fate)

and/or

The path feels good until they realize they are driving off a cliff

Let’s go through both of these traps:

1. Escaping the Messy Middle

I believe low-growth SaaS companies can get to 40%+ profit margins in 12-18 months. If they really want to…

Many companies have already made massive FCF improvements as their revenue growth has slowed. Public company median FCF has exploded from 0% to 22% in just ~3 years.

But…an important point that David makes is that most companies that have shifted to strong FCF margins are still unknowingly in the messy middle after considering the impact of SBC expenses. True high profitability requires you to also consider SBC/dilution.

Most public SaaS companies aren’t growing fast enough (or profitable enough) to outrun their high SBC expense. While the increase in FCF margins is great, it isn’t enough…And shareholder returns will be the casualty.

In addition to SBC expense, most companies won’t get their FCF margins high enough because they will experiment with AI products just enough to burn more money without seeing real long-term ROI.

I am already seeing a lot of this.

Companies have a FCF margin target so they can't spend much on innovation, but they need to spend some so they dip their toes in innovation. FCF margins are ~5%+ lower than what they could be. Problem is that customers don’t care about their AI products because it isn’t nearly as good as the competition. Burning cash with no added value.

👉 The penalty for being mediocre has never been larger…and it’s only going to get worse.

2. The Mirage of Profitability Will Lead You Off a Cliff

Becoming highly profitable can feel really good. “We are in control of our destiny”. “We don’t have to rely on VC money”.

Companies that go down this path may feel pretty good for 6-12 more months, but then, without warning, you will discover that the path led you right off a cliff…

Here is what will happen over the next 1-2 years on the profitability path:

Lots of change will be required to get to 40-50% profitability (including SBC)

Adopt a ton of AI internally

Massive layoffs

Cut lots of legacy software

Raise prices on products

So what’s the problem with this path? It’s worked for PE firms for decades.

AI has changed things. By the time you get within reach of those juicy 40%+ profit margins, they will start to fade. Below are three major things coming that I don’t believe most people on the profitability path are fully considering. And they will eat away at their profits, pushing them back to the “messy middle”, and ultimately cause equity destruction:

Pricing Power Weakens:

If you are not accelerating product, then customer willingness to pay a premium will drop because you aren’t a top product anymore. Customers also won’t accept your annual price increases.

This has always been true to a degree, but expectations are so much higher now.

Pricing Pressure Grows

The number of competitors in the “good enough” category is skyrocketing. If you are not top ~5% in your space, then AI will birth hundreds of copycats that are also “good enough”.

It’s worth repeating: The penalty for being mediocre is massive today (and growing).

Churn Is Coming

Most company leaders are not concerned enough about churn. They are complacent because the churn hasn’t really shown its full impact yet because of:

Multi-year contracts delaying churn

Deeply embedded software is making it hard to churn (yet)

Companies are slow to adopt AI so they haven’t experienced AI use cases yet

Churn will come slowly and then all at once for companies that choose mediocrity.

The Value of the Profitability Path

If you are admitting defeat that your company can’t compete and innovate with AI, then maybe the profitability path is the optimal outcome.

But is it worth it?

If my earlier scenario holds true, then lifetime future profits are maybe 1.5-2x current annual revenue — 40% FCF margins for the first year but then they get rapidly eaten away until they hit zero and you eventually shut down.

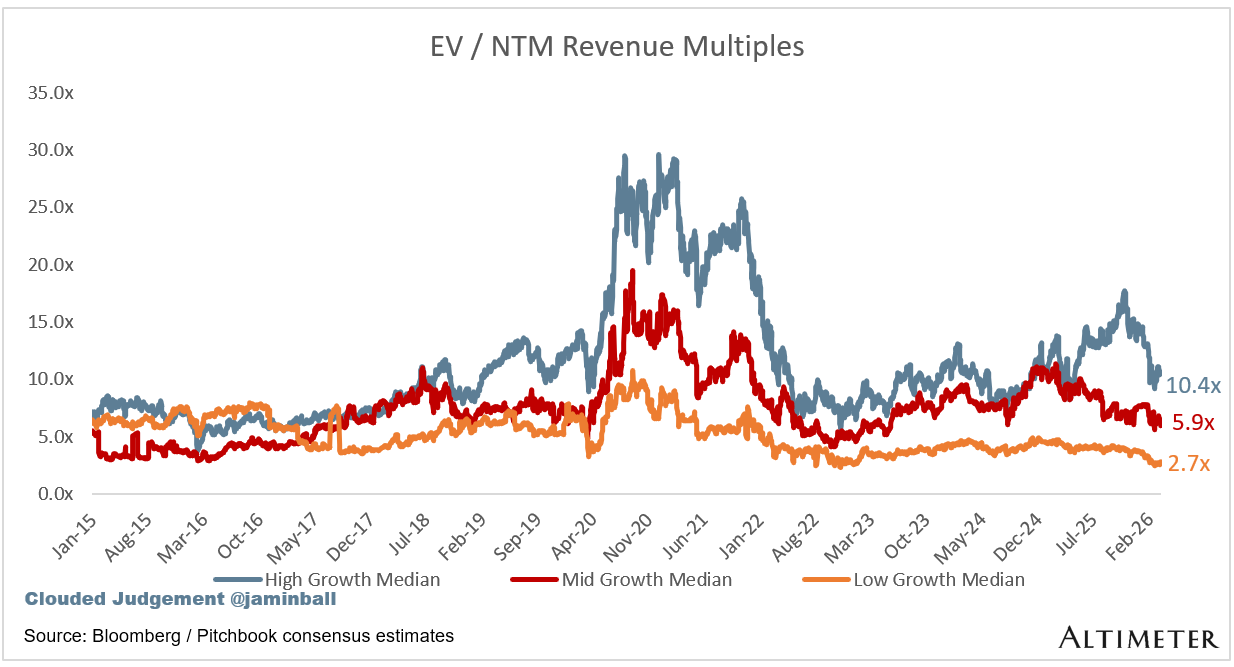

Look where “low growth” public company multiples are at…2.7x. And falling further every day.

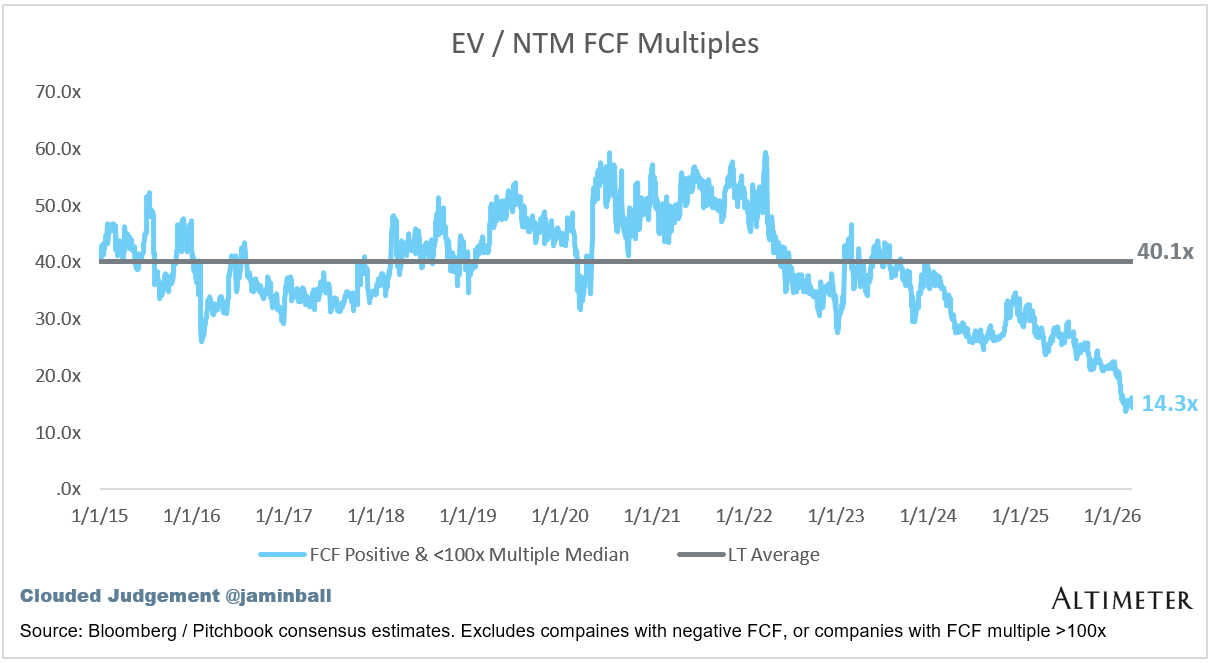

EV/FCF margins have been on a rapid decline since 2021. It’s at its lowest level ever at 14.3x. Why? Because investors don’t have faith in revenue durability. These companies are generating a lot more FCF, but how long will it last?

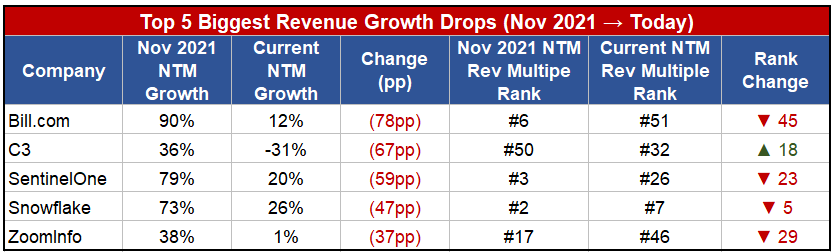

We have already seen what the market does to companies with weak growth endurance (ignore C3 which is benefiting as a perceived AI beneficiary). Their valuation multiples have been crushed.

But the future mediocre companies will get punished even worse because future durability will be even worse and profits will be eaten away even faster.

Mediocrity will create an eventual death spiral…

The Only Path Left: Accelerate

“Accelerate or die” is likely the only path left. Any other path just changes the timing and how you eventually destroy equity value.

I don’t have the answers on how you must accelerate and rebuild to become a true AI company, but you need to figure it out. It’s the only path that creates long-term equity value.

For companies with imagination, you will do more with more. For companies where the leadership is just out of ideas, they have nothing else to do. They have no reason to imagine greater than they are. When they have more capability, they don't do more. — Jensen Huang

Final Thoughts

If you don’t think you can accelerate the top line and build AI-native products that will win in the market, then maybe path #2 is right for you.

The reason I say there is only one path is because path 2 (high profitability) leads to outcomes that are rarely worth the journey. Fire most of the company and drastically cut costs to maybe be worth 1.5-2x ARR (or 4-6x FCF)? Not a terrible outcome if you are bootstrapped, but if you raised any amount of money then your equity is going to be worth close to zero anyway. If you are going down path 2, then get highly profitable asap and sell the company as soon as you can. If you wait, then revenue will struggle and profits will eventually fall. Then there will definitely be no buyers.

Get on path 1. It will be a lot more fun (and hopefully more valuable) than the alternative. You can be both accelerating AND highly profitable (many are), but it still requires you to be focused on path 1.

The #1 question teams should be asking:

What changes do we need to make now to actually get on path 1?

Footnotes:

Check out Paraglide’s AI agents in accounts receivable (today’s sponsor)

Check out David George’s article: There Are Only Two Paths Left for Software

Reply to this email if you want to sponsor OnlyCFO

📚 This Week’s Interesting Things:

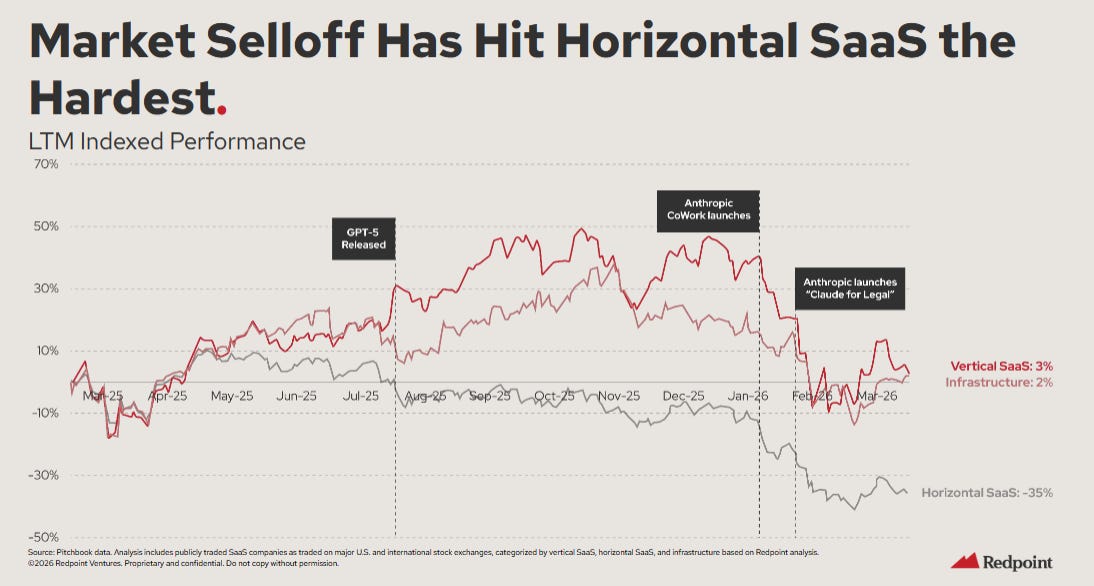

Redpoint’s Market Update

Logan Barlett and Redpoint team always do a great job on their annual market updates. There are lots of good slides, but the two below are interesting:

Riches in the niches….vertical software has been more resilient than horizontal due to the presumably more durable revenue

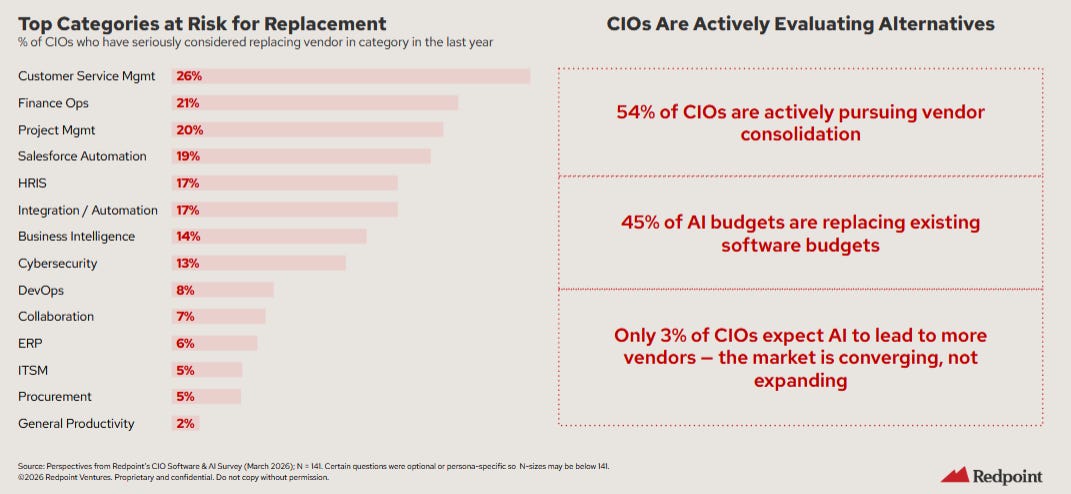

The categories at the most risk for disruption and less durable revenue

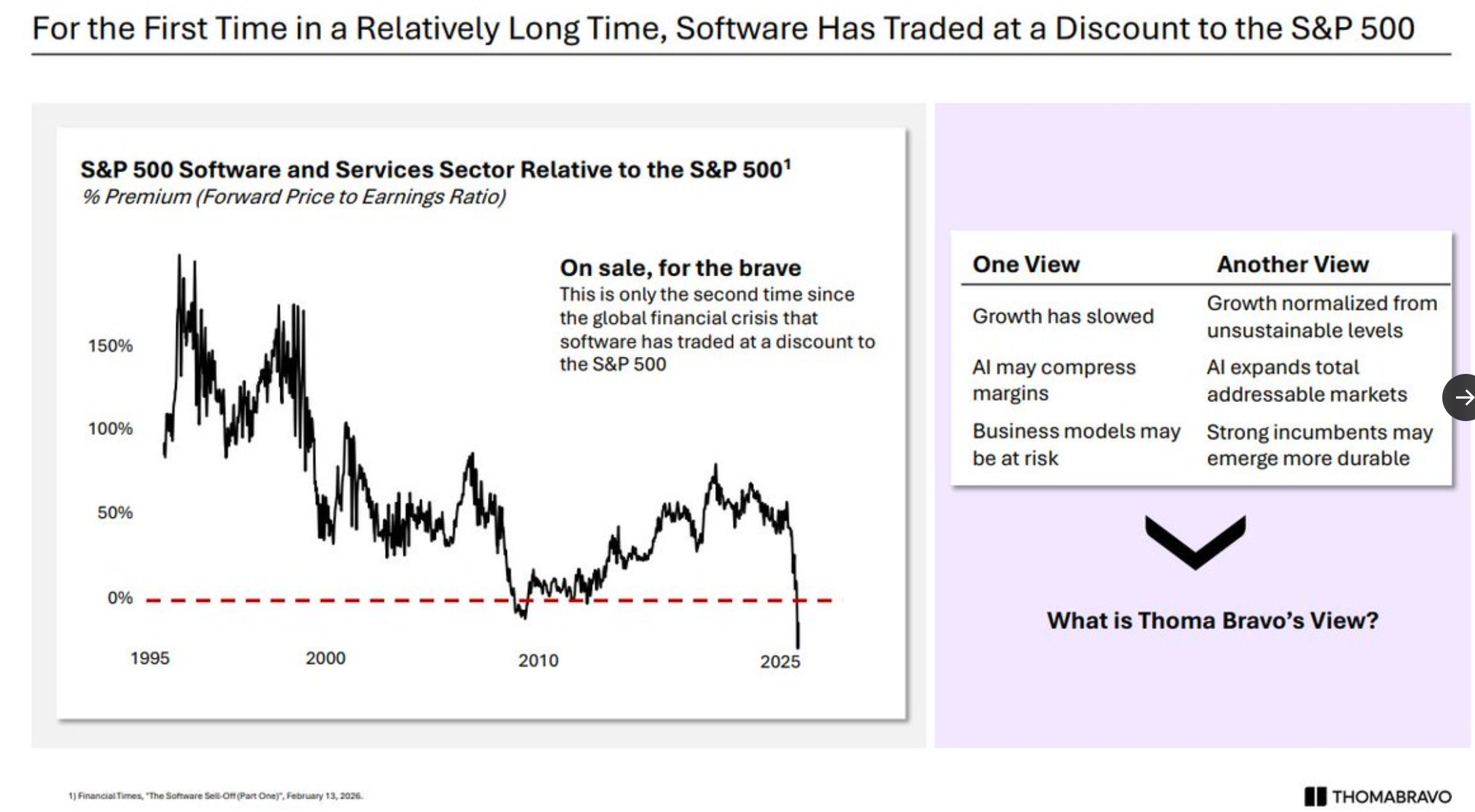

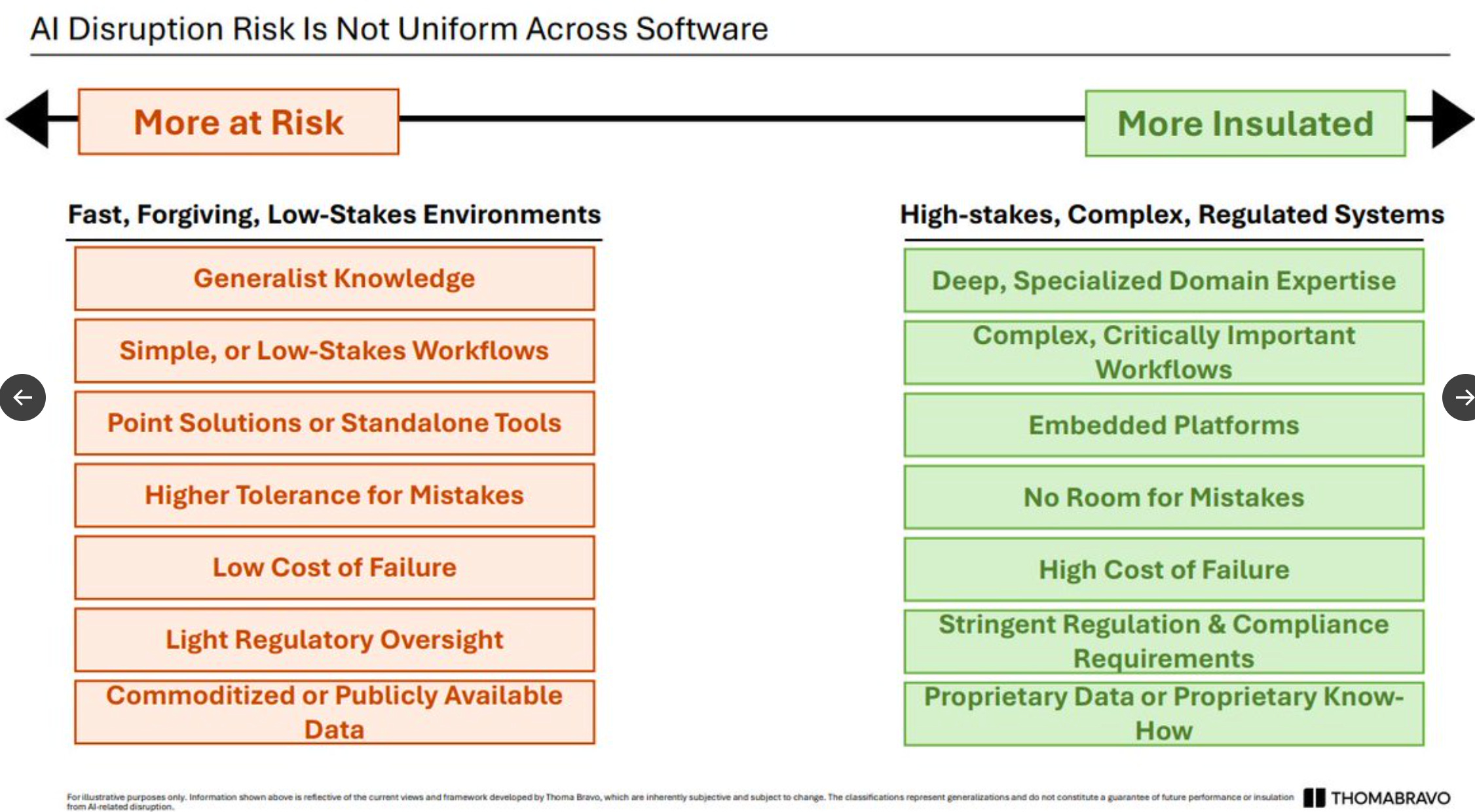

Thoma Bravo’s Software Update

Below are a couple of interesting slides from Thoma Bravo. Not all software is created equal, but the big question is how durable any existing software revenue will be. Some is certainly more durable than others, but….like I said in this newsletter, I don’t think it really matters unless companies are truly accelerating and building an AI company.

Another provocative post here. Agree with you that you just HAVE to focus on breaking through to higher growth with AI if you want to survive. Lock-in ain’t what it used to be.

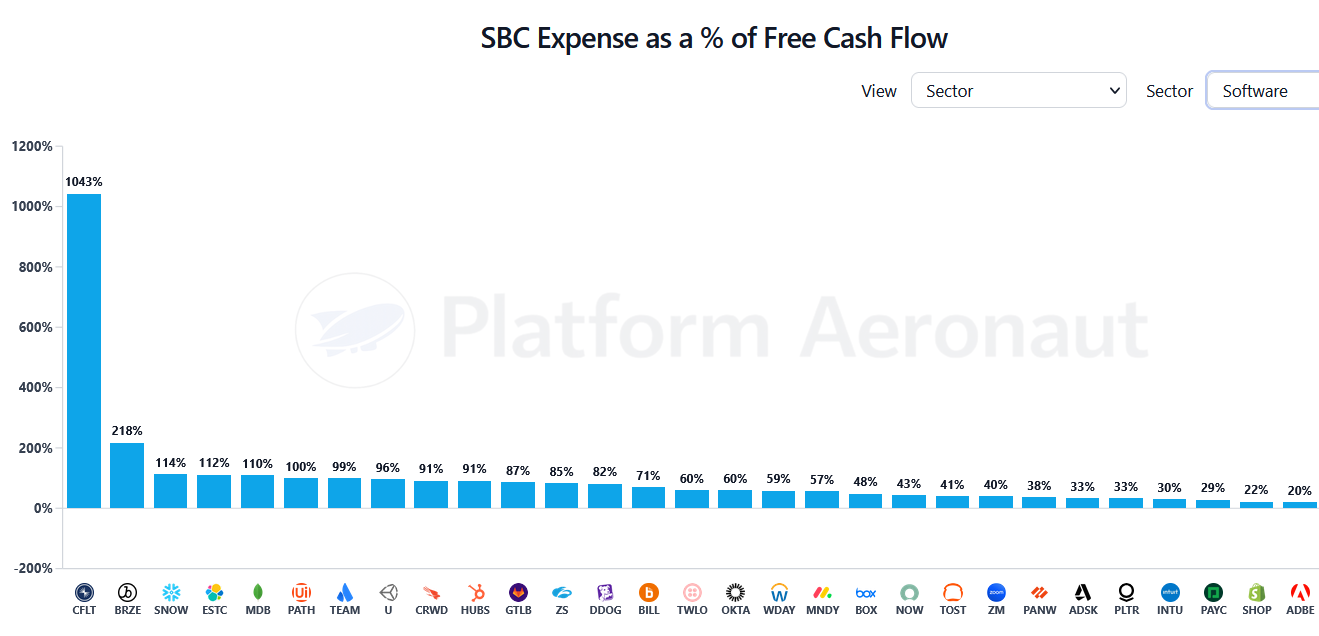

And those 22% FCF “profits” are illusory when you factor in SBC.

Turns out the median SBC cost % of ARR in my public data set is about 20%. At least the accounting value. As you know (and wrote about a few years ago) that “cost” isn’t necessarily tied to reality since for many it was set based on valuations for those shares that are long gone.

I’m thinking the trued up SBC cost is more like 10%, rather than 20% (a guess admittedly but I’m gonna see if I can put some meat in that) — meaning these companies are still generating real profits on average.

But yeah even that won’t be enough! And going away pretty quick. And of course it’s not like the companies won’t need to re-up their options pools to keep their good folks!

Good read. I am about 80% with you. Profitably is always a path, one huge reason. People, it is what is the difference. The question is more, what do you do when you are creating cash flow. Acquire, invest in innovation or go after adjacent markets. Profitably gives you options. My 2 cents…