The Software Debt “Maturity Wall” Looms | Who Will Survive?

The perfect storm is brewing for software value destruction...

Brought to you by…Paraglide

My teams have always spent way too much time on billing and collections...chasing customers, sending reminders, providing additional detail, etc. It’s high-volume, boring, and repetitive. Which makes it a perfect place to use AI agents.

Have my friends at Paraglide show you what AI agents can do in accounts receivable.

Paraglide helps businesses get paid on time with AI agents that automate billing and collections conversations in the finance inbox. AI agents respond to billing queries, send personalized payment reminders, track commitments, and manage disputes, removing the bottlenecks that delay payment.

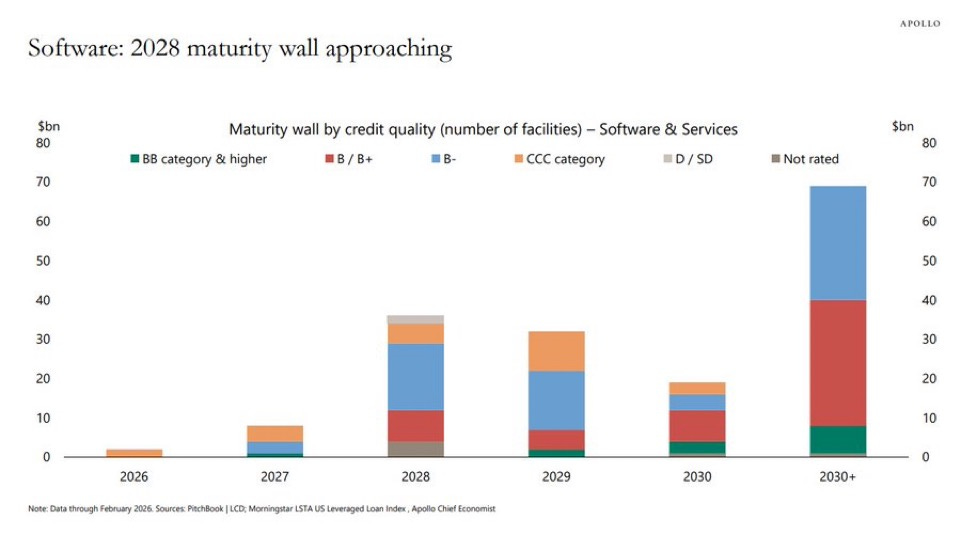

The “Maturity Wall”

There is a massive debt “maturity wall” of $40B (largely B- paper) looming for software companies. And we are going to hit the wall at the worst possible time:

Interest rates are significantly higher than when these loans were originally taken

AI-driven disruption is creating high uncertainty, which is lowering valuations and reducing debt downside protection.

Weakening software growth and fundamentals hurt the ability to pay debt while valuations simultaneously fall

My PE-backed / leveraged company friends are nervous because they know what comes next…

My company doesn’t have debt so this doesn’t apply to us, right?

Wrong.

1st order impact: It will be much harder for you to raise any kind of debt instrument.

2nd order impact: Software exits (at good revenue multiples) will start to fall, which also negatively impacts the VC fundraising environment. M&A (particularly from PE) has been responsible for the vast majority of software company exits. If private credit sentiment drops, which is led by the overall software sector sentiment, then both M&A exits and fundraising will fall as well.

The chart below will look very different in a few years…especially when evaluating PE returns on these M&A deals.

Understanding the “Maturity Wall” and Private Credit

Debt “maturity wall”: Large amount of debt comes due at roughly the same time. Companies with debt have a few options:

Repay loan: lol…yeah, right. SaaS companies aren’t doing that

Refinance: unlikely for most companies given the conditions today

“Amend and extend”: kick the can down the road with existing lenders

Sell the company: This is the PE goal. Sell before maturity to 3-5x their money after a few years. But this is not happening for almost anyone right now.

Distressed options: Equity value likely getting wiped and debt taking a discount (fire sale, lender swap debt for equity, default and bankruptcy, etc)

The software debt coming due is from loans made when Fed rates were near zero, tech valuation multiples were at their peak, and lenders believed the SaaS gravy train would run forever.

Companies trying to refinance today may see their debt interest rates increase by as much as 2x (or more) based on higher Fed rates and increased AI risk

Slightly more than half of software debt is rated at B- or lower (not good)

$25 billion of US software loans slid into distress in January

Typically, borrowers will handle maturing debt 6+ months before maturity.

A UBS strategist said we could see default rates in software heavy portfolios increase to 15% (up from the historic ~1-2% over the past decade). The baseline default rate for private credit has already climbed and the use of paid-in-kind (PIK) interest is at an all-time high. Both factors indicate trouble is brewing…

Software companies previously looked like the perfect LBO (leveraged buyout) candidate for PE firms, which is why private credit had the most exposure in software (software M&A by PE has been hot for many years). Software companies had recurring revenue with high net retention, highly profitable at scale, and software companies could also be sold for at least 2-3x ARR (in a downside scenario to recoup the loan). As a result of all of this, software companies account for ~25% of all private credit.

But this is no longer true in 2026. Almost everything that made software a strong LBO candidate is showing cracks (and big ones).

A lot of these companies will need to refinance when their valuations have tanked, growth has slowed, uncertainty has risen, and interest rates are higher. And many companies will be trying to do it at the exact same time.

There are ~2,000 PE-backed software companies that will need to figure out how to service their debt load in a disruptive AI world where refinancing may not be an option or the terms might be crippling. And ~20% of those companies will need to refinance in just a couple years (at most).

The Leveraged Company Playbook

The reality is a lot of these highly leveraged companies won’t survive. Or at least the equity will be worth zero and the business will be sold for parts to recoup the debt. It’s hard enough just being a legacy (non-AI) software company in 2026. And then throw debt into the mix and you have a ticking time bomb that is growing bigger every day.

If these companies are too slow to act, then they will enter a death spiral that quickly swallows them (if it hasn’t already).

1. Start Cutting Costs Now

This is why my PE-backed company friends are nervous…

PE-backed companies are going to do this faster and cut deeper than anyone else over the next 12 months. PE firms have IRR targets and a ticking time bomb in the form of debt. So they MUST cut costs:

To fund higher debt payments when they amend and extend

Lower leverage ratios so they actually can amend or refinance (and hopefully get lower rates)

Become a more attractive acquisition target

In order to accomplish the size of cuts that are probably needed at most PE-backed companies, they will need to aggressively adopt AI internally.

And it’s already happening. They are going to use Claude to cut headcount and likely rip out a lot of software as well (at least the non port co software :).

2. You Can’t Fall Behind in AI

Customers are moving fast in 2026. Cutting everything to the bone to juice EBITDA used to be a good strategy because of how sticky software was. The PE folks could raise prices by 10% every year and customers had vendor lock-in for several years.

Much less true today.

Make sure R&D still can compete on the AI front. Extending your debt a couple of years won’t help you if all your customers churn next year…

3. Start Refinance Conversations Early

Don’t wait until just 6 months before it matures….because based on the “maturity wall” there will be A LOT of other folks trying at that same time.

The AI risk premium might only increase and/or your situation may deteriorate to a point where you are forced into default or the terms are so bad it will cripple the company.

The “Amend & Extend”

The vast majority of these companies will “amend and extend” their debt with their lenders. It’s beneficial for both sides:

Company: Gets more breathing room and time

Lender: Doesn’t have to mark down their loans

This is often referred to as “extend and pretend” in private credit because you are just delaying the problem and pretending that everything is fine.

There are two pieces to this strategy, but both have the same goal of delaying any cash payments by the company:

Extend the maturity of the loan

If paying interest in cash each year, amend it to paid-in-kind (PIK)

Extending the maturity delays the big loan principal payment while amending to PIK delays the interest payments until the end as well. The problem is that PIK is basically an interest IOU. Instead of making interest payments every quarter, it gets stacked on top of your principal and your debt problem compounds. And it compounds at an even higher interest rate because your lenders don’t “amend and extend” for free…

Lenders get:

An upfront fee to amend

A spread bump (higher interest on the debt)

And often some incremental covenant protections

Company gets:

1-3 more years of runway

No default

No restructuring

In other words, everyone kicks the can down the road while the problem grows…

The Losers?

Here is the order of who loses in all of this craziness.

Employees at leveraged companies. PE-backed (and other companies with debt) are going to feel the pain/pressure first and be quicker to act. Layoffs are coming.

Legacy software companies whose tools are getting ripped out at these companies as they cut costs with true AI efficiencies.

Private Equity: Everyone has been talking about private credit, but remember they sit at the top of the capital stack. Meaning private credit lenders get paid before the PE firms. Whatever is left goes to the equity holders. Many PE firms with high software exposure will see massive losses on those deals.

Private Credit: The negative sentiment here seems a bit overblown to me. Since private credit sits at the top of the capital stack, they are much better positioned than private equity in downside scenarios. The original deals were done several years ago at ~5-7x EBITDA (or maybe 2-3x ARR on the very high side). Assuming they have grown a bit over the past several years, then selling the company to at least cover the debt seems likely in most cases. But some private credit will certainly take a hit from software names that are struggling that no one wants to touch in the age of AI.

The entire software ecosystem: All this means fewer exits for software, which then means less fundraising. Bad for everyone

Final Thoughts

Exits are going to decrease significantly (at least ones where equity holders have much value) as we go through this cycle.

If you have debt, the key takeaways are: 1) cut costs (increase EBITDA) and 2) start the refi/extension conversations early.

And whether you have debt or not, your chances of a decent exit are 100x greater if you show strong EBITDA margins than you have today.

Footnotes:

Check out this billing and collection AI agent. If you want to cut costs (everyone needs to) and collect more cash, then you should have an AI agent in accounts receivable. Paraglide is today’s sponsor.

Reply to this email if you want to sponsor OnlyCFO. I will make your wildest marketing dreams come true.

*Nothing should be considered investment, tax, or legal advice. Educational purposes only.

Interesting Things I Read:

Private Credit Redemption

Redemption requests (investors asking to get their money out) have reached historic highs. There is typically a 5% quarterly redemption cap to ensure new investor money can meet the demand. But redemption requests are now surging above these caps and the replacement investor capital is collapsing…

Blue Owl: Redeemed 15% of NAV

BlackRock: Gated redemptions and held the 5% cap

BlackStone: Execs injected $400M into the fund for 7% redemption requests

The private credit concerns seem a bit overblown, but it is impacting private credit and its availability.

Where Are 2026 Budgets Going??

Yes, IT budgets haven’t shrunk but it’s being reallocated to AI…

Move Faster

If your company isn’t moving fast, then you are toast. Things are moving too quickly for you to not move fast. And importantly fail fast, move on, and adapt.

Yeah I've been thinking that speed is not a number 1 priority, but last few years changed that entirely. Now the speed is almost everything