"Trump Accounts" Are Live | Should Companies Add This Benefit?

Yes, it's one of the highest ROI employee benefits available. Here’s what you need to know.

Jul 14, 2026

“Trump Accounts” (aka Section 530A) are one of the greatest employee tax-advantaged opportunities ever created and they just went live on July 4th.

Every parent of an eligible child should open up an account (it’s free). Even if a child does not qualify for the free $1,000 government contribution, there are still meaningful benefits for all other children under 18.

Every company should likely create a “Trump Account contribution program”

If you are a CFO, then read below and figure out how to start getting it set up. If you are not in charge of benefits, then send this article to your HR team and/or CFO and tell them they need to implement it :)

*Put your politics aside and get over it being called a “Trump Account”. The program has huge tax benefits and can significantly help your kids. Every U.S. citizen and company based in the U.S. needs to understand this.

Who Benefits From Trump Accounts?

These accounts are early childhood savings vehicles to help kids learn about the value of investing and save for retirement.

Who? Anyone <18 years old with a social security number (after 18 typical traditional IRA restrictions apply).

Amount? Total of $5,000 per year (including employer contributions) can be contributed to each child’s account.

Investments? Limited to low-cost mutual funds and ETFs that track broad indexes mostly composed of U.S. companies.

Withdrawals? Prohibiteduntil the year the child turns 18 years old and then IRA rules apply (10% additional tax on early distributions with limited exemptions like first-time home purchase, education expenses, etc)

Free $1,000? Qualifying U.S. citizen born between 2025 and 2028 can receive $1,000 from the government (does not count toward the $5,000 per year limit)

Taxes? All gains, interest, dividends, etc are tax-deferred (only taxed when withdrawn).

Why Employers Need to Offer It

All the above benefits are great, but one of the biggest potential benefits comes from your employer.

There are three things a company can add some of this benefit (all companies should probably at least do #1 and #2):

Enable after-tax payroll deduction which just helps employees automatically invest part of their regular payroll into Trump Accounts. This wouldn’t impact the employer $2,500 limit but would count toward the total $5,000 limit. No tax advantages, but potentially adds a tiny bit of convenience for employees if it helps streamline deposits and limit tracking.

Enable employees to contribute pre-tax dollars up to $2,500 to a dependent’s Trump Account. This would reduce their taxable income and save taxes.

The company can contribute up to $2,500 per employee which is tax-deductible to the employer and tax-free to the employee.

💡 Note: The combined limit of #2 and #3 is $2,500 per employee (not per child). For example, if the company contributes $1,000, the employee can contribute only another $1,500 through pre-tax salary reduction. The employee could then contribute another $2,500 with after-tax dollars (#1) to reach the child’s overall $5,000 annual limit.

Obviously #3 (company contributions) can add a lot of new expenses for a company, but simply adding the plan and allowing employees to contribute pre-tax dollars (#2) saves employees on their marginal federal income-tax rate.

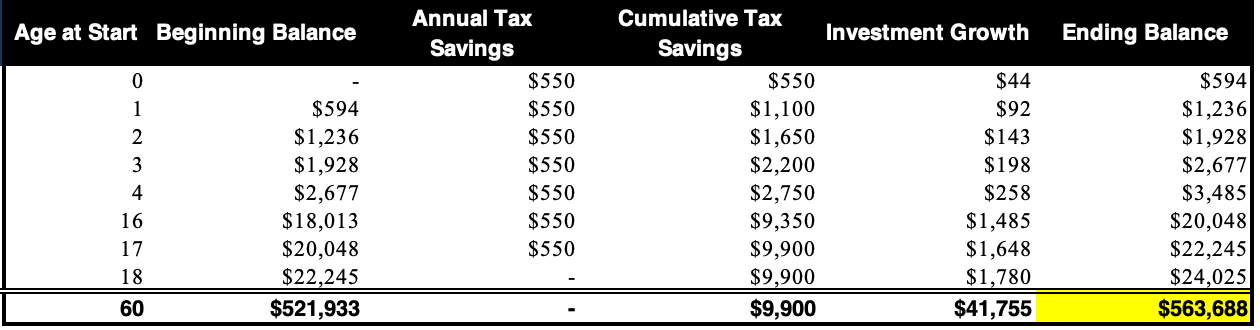

Pre-Tax Contributions Example

Let’s say I have a household income of $150K and I am in the 22% marginal federal income-tax bracket (I am married filing jointly). If my employer offers this benefit then I can reduce my taxable income up to $2,500 per year and give those dollars to my children’s retirement.

Instead of giving the IRS $550/year (22% * $2,500) you can contribute more to your children’s retirement or you can just save that amount in taxes if you plan to contribute $5K either way. Based on compounding returns in the U.S. stock market (assuming a reasonable 8% growth per year), those tax savings will grow to nearly $0.6M (or about $100K in today’s dollars if inflation adjusted) by the time the child is 60.

So instead of giving the IRS $9,900 over the first 18 years of your kid’s life ($550 * 18 years) there will be an additional ~$600K benefit by age 60 because of the pre-tax contribution benefit.

*If you use the 10.5% annual return that the Trump Account website uses then the tax saving alone would grow to $1.9M while each child’s account would grow to $18M by the time they are 60. Very generous assumption, but still…power of compounding is incredible.

Obviously if your employer is willing to just fund employees’ children’s Trump Accounts then that is even better for employees, but many companies won’t want to pay an additional $2,500/employee so this option is a major advantage for employees versus those that do nothing.

Process & Cost to Companies?

CFO: We are trying to cut costs so we can’t add more employee benefits like this

Wrong. Companies can add the program for just a little incremental cost that still has a large tax advantage for the employee.

The Department of Labor confirmed last month that Trump Accounts should not be subject to ERISA. That’s a big deal. Company 401(k)s, for example, are subject to ERISA and have a lot more additional documentation, reporting, audits, internal communications, etc.

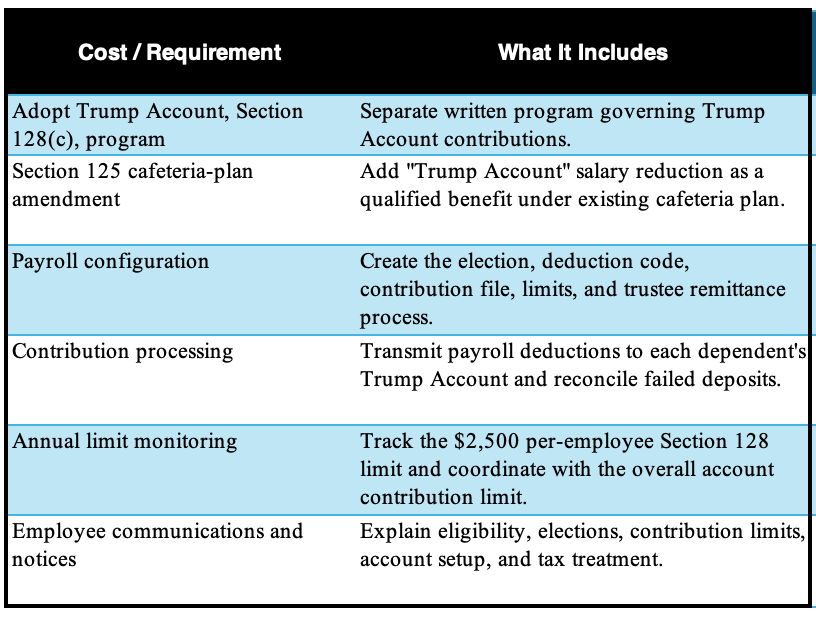

Below are the main requirements to get it set up:

So maybe a couple thousand dollars to create the written plan and amend your existing cafeteria plan. And then your benefits provider will charge an additional small per participant fee.

Fairly immaterial cost for a material potential benefit.

Other Important Notes

Tax-deferred vs Tax-Free: These accounts are retirement savings vehicles (IRAs) so eventually kids will pay taxes on gains on withdrawals at their tax rate at the time of withdrawal

Money belongs to kid: The money is the property of the kid when it goes into the account. Parents can’t redirect money to another child like a 529 plan

Money is locked until the year the child turns 18: There is no hardship exemption or any way to access the money before the kid turns 18. Don’t contribute if you think you will need the money before then

Employees need to set up the accounts themselves: Employees have to set up their kids’ accounts and then provide that info to the company in order to participate in the program. Setup is really easy though…

Need to track contribution limits: Someone who changes jobs or receives contributions from multiple employers must ensure total contributions do not exceed the $2,500 annual per-employee limit.

Employers Have Contribution Options: Examples include, $1,500 funded for a new baby or adoption, employer match up to $1,000, flat dollar contribution per year, etc.

Final Thoughts

A company with a Trump Account Contribution program is a significant benefit for employees. And it will be a big negative in recruiting if you don’t have one.

I have heard many people (and even some companies) say they won’t sign up because Trump’s name is attached to it… Let me be clear, that is stupid. It’s a great benefit that will hopefully teach kids the value of investing while also giving some great tax advantages.

It’s also pretty cool that Grandma, Grandpa, or a friend can easily contribute to a child’s retirement account (scan a QR code and send money).

Set up accounts for your child and tell your company that they should set up the program as well!

Footnotes:

Sponsors: Email me at onlycfo@onlycfo.io for sponsorship opportunities.

Subscribe and tell your friends

*Nothing in this post should be considered tax, legal, or investment advice. Educational purposes only. Consult an investment and/or tax advisor.