"We Just Raised $20M at a $100M Valuation" | What Does "Valuation" Mean?

Understanding valuations and where headlines can be deceiving

Brought to you by…Brex

AI agents in finance are really powerful when they have the right context, controls, and operating environment.

I (OnlyCFO) have been working closely with Brex for over 2 years, and what they’ve built for agentic finance (AF) is incredible. With Brex, agents handle all the tedious stuff, like expense reports, policy enforcement, and month-end close, so your team doesn’t have to. Check out Brex AF!

OnlyCFO’s Valuation

Headline: The OnlyCFO newsletter hits 39,000 subscribers and raises $20 million at a $100 million valuation!

While the above isn’t real (it’s probably worth a lot more 🤣), we see these types of headlines all the time.

What does “valuation” even mean?

How do private valuations differ from public companies?

How can fundraising announcements be deceiving?

What Does “Valuation” Mean?

In public markets, “valuation” usually means one of two things:

Market cap

Enterprise value

1. Market Cap

When people say “valuation” they could be referring to a few things, so first you need to understand some terms and definitions:

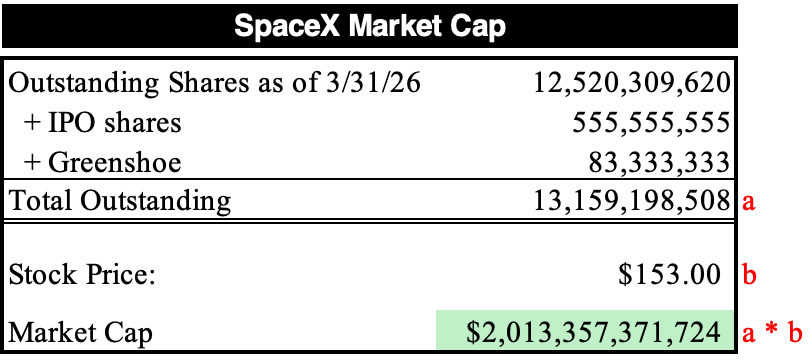

Market Capitalization (aka market cap): is the total value of a publicly traded company’s outstanding shares.

Market Cap = stock price * number of shares outstanding

SpaceX Market Cap

Stock price is straightforward. It’s the price listed on the stock market. SpaceX closed on June 25th at $153.

Outstanding shares is a bit more complicated. Outstanding shares are only disclosed quarterly (on 10Q/10Ks) unless there is a material event that requires additional disclosure. Additional shares from an IPO are disclosed in an S-1 and the exercise of the greenshoe is disclosed in a subsequent 8-K, but things like employee exercises and immaterial changes only get updated quarterly.

2. Enterprise Value

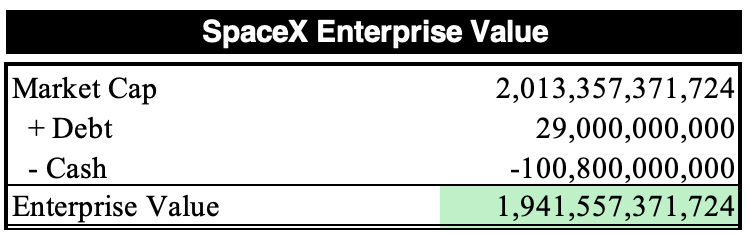

Enterprise value (EV): is more comprehensive than market cap. EV includes the market cap of a company but also adds debt and subtracts cash. EV is used for operating valuation multiples like EV/Revenue and EV/EBITDA because it accounts for capital structure.

EV = Market Cap + Debt - Cash

To continue the SpaceX example, their EV would be lower than their market cap, which is common, because they are in a positive net cash position (cash > debt)

Wait….Why would debt make your company more valuable and cash makes you less valuable? That seems like a mistake, right?

Enterprise value is a financing calculation. It represents the amount someone would theoretically pay to acquire the company. An acquirer would have to pay those who own equity (represented by market cap) plus everyone who has loaned it money (lenders). Once you acquire the company though you get the company’s cash so you can use that to pay off the debt. That’s why you add debt and subtract cash.

Example: Imagine two companies with a market cap of $1B. Company #1 has $1B of cash and Company #2 has $0 of cash. The company with $1B of cash is valued just on their cash level. Someone could theoretically buy it for free. since they get their $1B of cash after they acquire it. While the company with $0 of cash has built something worth $1B so you will have to pay $1B for it.

In reality though, acquiring a public company outright will almost always be higher than the current EV because there will be a large premium paid to be able to acquire all the shares.

Valuations Can Rise While Stock Prices Fall

A company’s “valuation” can increase while shareholders actually lose money. This happens when your slice of the pie shrinks faster than the total pie grows. In other words, dilution eats away stock returns faster than the valuation increases.

Zoom is a good example of this…

Zoom’s stock price is flat since May 2019 (shortly after the IPO). But during that time the market cap went from $18.9B to $24B over that period of time (a 26% increase)

Wait…so why is the stock price flat if the market cap is up?!?

Dilution.

Valuation increased slower than dilution increased which was a huge drag on stock price. If it wasn’t for dilution, Zoom’s stock price would be 26% higher.

What Does a Falling EV Mean When Market Cap Increases?

Zoom’s cash position has changed materially since the IPO. Immediately following the IPO, Zoom had $0.7B and as of April 30, 2026, Zoom had $7.7B in cash and investments….

So while the market cap went from $19B to $24B (26% increase), the enterprise value actually decreased because of its net cash position today versus 7 years ago.

$24B market cap - $7.7B of cash + $0 of debt = $16.3B EV

So it is actually cheaper to acquire Zoom today than 7 years ago. While the market cap increased, the underlying business is deemed to be worth less today by investors. EV shows this by taking out the cash and debt that the business has.

It’s why EV is used in financial metrics like EV/revenue.

Private Company Valuations

When a private company says something like “OnlyCFO newsletter raised at a $100 million valuation” it’s similar to market cap but inflates valuation in almost all cases.

Headline Valuation = recent price per share * fully diluted shares

This definition looks the same as market cap but the nuances can be significant

Price per share: This is the price the recent financing was at, but it’s also the terms the recent round was at.

Fully Diluted Shares: This is outstanding shares + all dilutive securities (unexercised options, available option pool, warrants, etc).

The biggest potential issue is using the recent price per share and applying that to all shares. If a round was done with heavy structure then that creates a lot more value for those shares. Some valuable terms may include:

Liquidation preferences mean they get paid back some amount before common stockholders get paid anything. 2x liquidation means preferred holders get paid back 2x their investment before anyone else gets anything. That is valuable and would be deceiving then to apply that share price to all shares.

Participating: They receive their liquidation preference and then also participate in the remaining proceeds as if they had converted to common (double dipping). This is pretty rare to have.

Seniority: Does the latest round get their liquidation preference first or is it pari passu (equal priority) and gets paid pro-rata?

Anti-dilution: Protects investors in a future down-round (lower valuation) scenario. They will get more shares if it kicks in.

For example, when you have a liquidation preference then your downside risk is significantly limited.

Liquidation Preference Coverage = Total liquidation preference / ARR

Let’s say VCs invest $500 million into a company at a $30 billion valuation because it has the potential to be a $300 billion company. But the company currently only has $500M of ARR. That is an extremely rich ARR multiple (60x). But…the liquidation preference coverage is just 1x. Most investors will assume that in a worst case scenario the company could sell for 1x its current ARR so they could get their money back while common stockholders would get nothing. That liquidation preference makes the preferred shares a lot more valuable than any of the common shares and the headline valuation of $30 billion a bit misleading.

Final Thoughts

Theoretically, I could have my dad invest $1 at a $2 billion “valuation” and say my most recent valuation is $2 billion.

It’s a fact, but it’s obviously not the truth.

It’s important to understand what people mean when they say “valuation.” And if you are an employee at a private company then you should understand what the structure of that recent valuation is so you understand how real it is and what it means for your employee equity.

Footnotes:

See how Agentic Finance can transform your finance department (today’s sponsor is Brex).

Subscribe and share the OnlyCFO newsletter with your teams

Another banger. Price is what you pay, Valuation is what you get!

If you don't think that someone would pay $100M for the business today, but you have a term sheet valuation of $100M, then there is a dislocation in expectations. Better figure that out!

The gap you're describing between headline valuation and what it actually represents is the same gap I keep running into on the AI side. A dashboard can show a number that's technically correct and still be the wrong number to be looking at. The fix in both cases seems to be the same: someone has to ask what the figure is actually measuring before it goes in front of a decision-maker.