Where AI Costs Belong on the P&L

AI token spend will soon be your largest vendor expense (if not already), and many of you are accounting for it wrong...

Brought to you by…Deel

I made plenty of mistakes when expanding internationally. I’ve learned a lot over the years, so I wrote a guide on some of the most important finance considerations:

General guidelines for how to hire (contractor, EOR, set up an entity)

Offshore cost benchmarks by country

Additional employer burden (don’t forget about these!)

I partnered with Deel to pull real cost benchmarks (the kind of data I wish I had when doing this). Download my playbook for expanding internationally.

A CFO’s Worst Nightmare: “Tokenmaxxing”

Anthropic is awesome. I am going to probably use $300 million of Anthropic this year at Salesforce. Coding. Everything’s going to be cheaper to make. — Marc Benioff (CEO of Salesforce)

AI tokens are becoming the biggest vendor expense on the income statement (if it isn’t already). From basically $0 spend to the largest in just 2 years...If token costs aren’t rapidly becoming your largest vendor expense, then that probably means you are behind in AI adoption.

Everyone is “tokenmaxxing” right now. And everyone seems to be encouraging it. Well, everyone except for maybe the CFO 🤣.

Tokenmaxxing: maximizing AI token consumption as a signal for AI adoption.

The primary goal, which everyone can agree with, is to make sure folks (across departments) are really adopting AI. AI adoption is critical to every tech company’s survival in 2026.

But this AI adoption is creating a very large expense that companies need to make sure is treated properly on their income statement. And leaders need to understand how it impacts the financials, their budgets, and the company’s long-term unit economics…

AI Costs on the P&L

Cost of Revenue & Gross Margins

When AI is embedded in your product, then that portion of the costs is included in COGS. It’s an incremental expense line in COGS.

The COGS lines 1-5 are the same, but now we have a large new one (#6).

Professional services

Support team

DevOps

Customer Success Management (diversity in practice)

Infrastructure/hosting costs (AWS, Azure, etc)

AI token/inference costs

API spend with AI models (Claude, ChatGPT, etc)

Model hosting when you self-host (not calling an API but using AWS, Azure, etc GPU power)

Vector database costs

Orchestration and observability

This new (and large) expense line in COGS is creating much lower gross margins and that requires a shift in how leaders think about long-term unit economics.

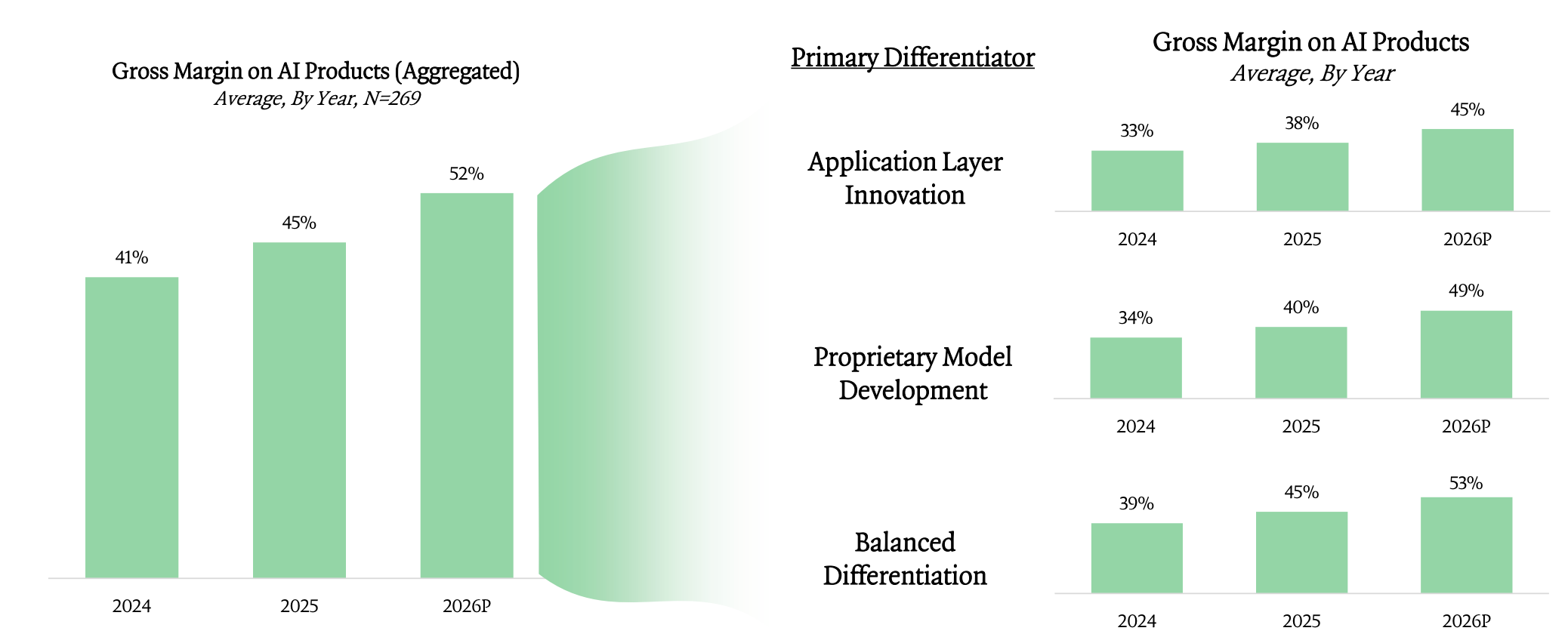

While AI gross margins are up a lot in the last couple of years (from 41% in 2024 to 52% expected in 2026), they are still significantly lower than typical software gross margins.

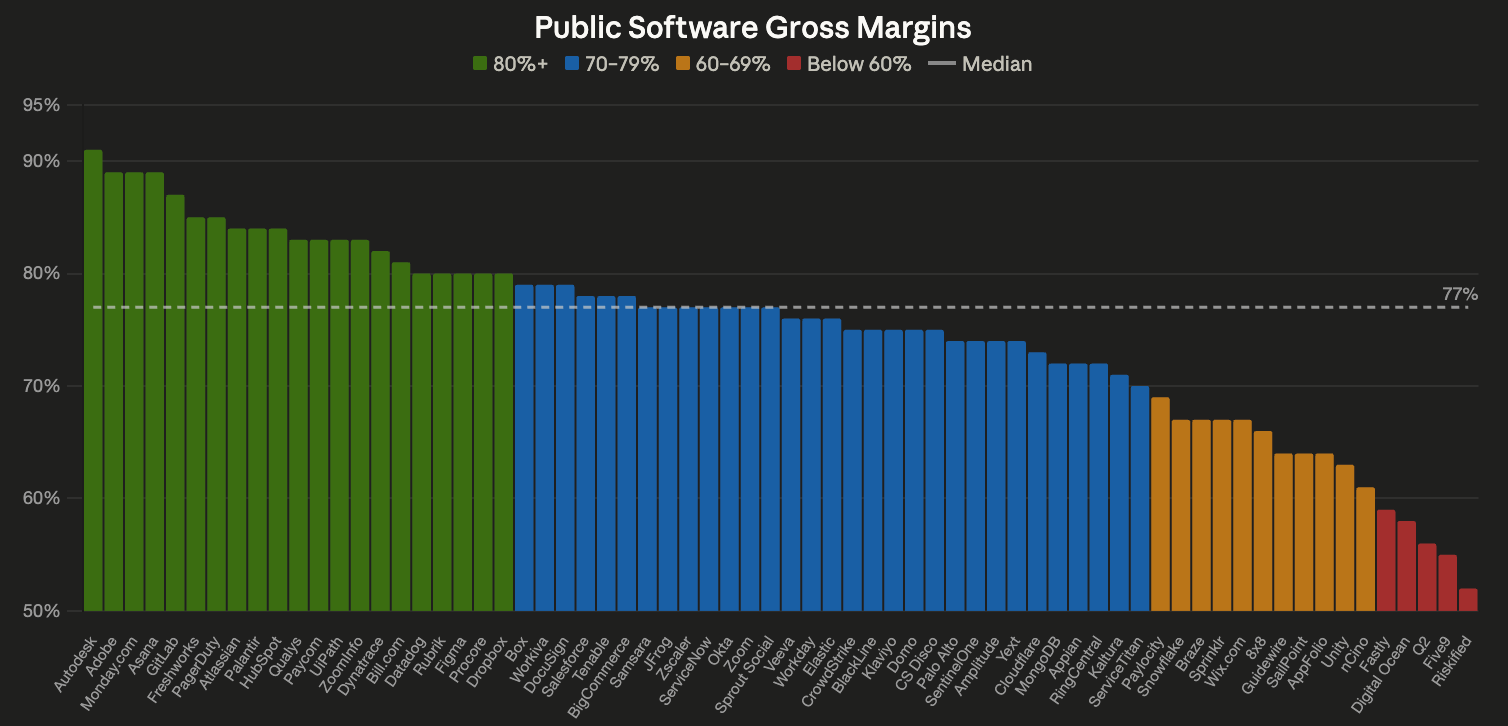

The median public software gross margin is 77%. This is largely because true AI revenue still isn’t a significant portion of their total revenue yet. Gross margins will be materially lower for most of these companies in 12-18 months…

Because of the vastly different economic profile of AI products, it’s important to be able to track the revenue and COGS of all products separately.

I have talked to a lot of companies that have been blending AI token costs in their “hosting” P&L expense line and also can’t segment gross margins by product. Do NOT do this. The extra data is critical for making decisions.

Create a new line just for the AI costs running through COGS. You, the broader exec team, and the board will want to pay close attention to COGS from AI so tell your accounting team to create a separate line for it.

Below are a few new metrics that every company should be tracking:

AI COGS as a % of AI revenue. How much lower are AI gross margins?

Gross margins by individual AI product. Do some AI products have worse gross margins?

AI COGS relative to total revenue. How much is AI degrading overall gross margins? What is the trend?

Correlation of AI COGS with revenue. Do you have a broken pricing model?

R&D AI Costs

Your “builders” (engineering, product, and design) are typically the people at the company who are burning the most tokens/spend on AI. And they should be spending the most given what they should be building.

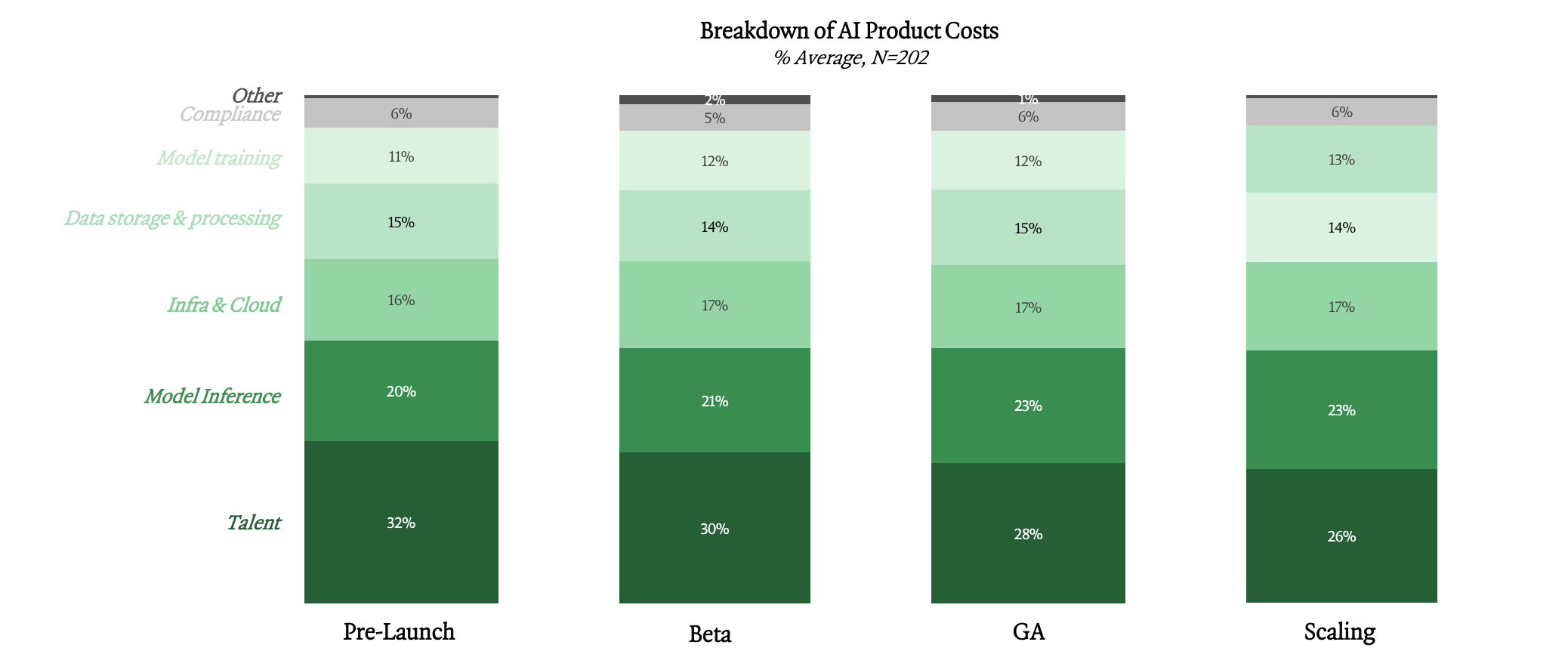

The breakdown below shows the costs required to develop an AI product. Costs are pretty consistent across product development stages.

According to a survey performed by Scale (that Jason Lemkin discussed on SaaStr), the average developer spent $1.3K/month (or $16K per year). And many folks think this is too low…

But you can’t have more token costs and not have something else impacted. Either the higher spend has to directly translate into more revenue. Or…it means you have to cut headcount costs.

You have to figure out the ROI math on when the additional token cost per employee is less effective than the headcount that must be cut as a result of the higher token spend.

S&M AI Costs

There are a lot of AI use-cases in sales and marketing, but most of them are not that expensive in tokens from what I have seen.

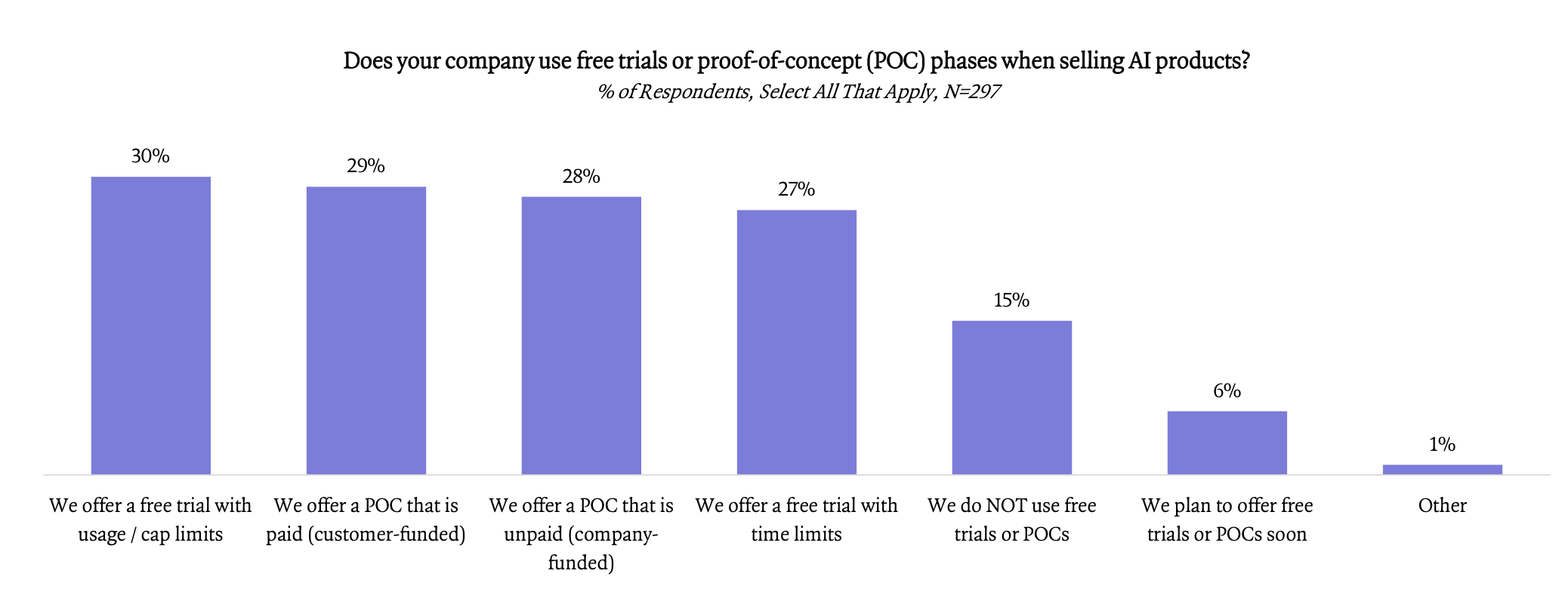

One S&M AI cost that can be large (and often misclassified) is the incremental POC/trial costs for AI products. The costs associated with these should go to the sales/marketing department. I have seen many companies not track these well, and they end up erroneously in COGS.

These POCs/trials are increasingly common with AI products as customers want to see the value before they commit. Companies need to make sure the costs are not spinning out of control as they add more AI stuff.

G&A AI Costs

Beware of the AI cost dumping ground into G&A. G&A frequently becomes a cost dumping ground (even before AI):

Ignorance or bad accountants who don’t know that some of those costs don’t belong in G&A

Intentionally pushed to G&A so it makes all the important financial metrics look better

Some diversity in practice where some costs go

But company-wide enterprise AI licenses (Claude, ChatGPT, etc) do NOT all belong in G&A…In fact, the amount of AI-related costs sitting in G&A should be smaller than the other buckets (COGS, R&D, and S&M).

Yes, my G&A teams are doing some cool stuff with AI (check out CFOpilot to see what my teams and I are building with AI). But we should not be nearly as token-heavy as what R&D (or usually even S&M) should be spending.

Allocating AI Costs

Performing allocations of certain shared costs is nothing new for most companies. Although many do it wrong (especially private companies)

Example: IT Department Allocation

All company-wide software that is used by everyone (Slack, Zoom, Gmail, etc) is put into the IT department and then at the end of each month, it’s allocated across all the departments based on headcount.

Every department absorbs some of the costs since they all use it. So these costs end up in COGS (allocation to the support team), R&D (allocation to engineers), etc.

Your AI bill should NOT be allocated this way.

Headcount was a good proxy for how seat-based costs should be allocated across the P&L, but that breaks down for consumption-based pricing vendors. Especially when the usage can vary so much across departments and when it is a massive expense (like token spend).

More exact allocations are needed for token costs. The only good approach now is to do direct allocations based on specific department usage. Finance teams need to segment the different types of AI costs by department. Anything else will result in materially incorrect financials and unit economics.

Final Thoughts

Token costs are going to be the largest vendor expense in nearly every leader’s budget by the end of 2026, so it’s important to get the accounting and department budgeting right.

Trade-offs and changes will have to be made. You can’t just add a massive line of expense across the P&L and expect nothing else to change.

But companies can’t make the right decisions if the financial metrics are screwed up because AI costs aren’t properly allocated across the P&L.

Footnotes:

Download my playbook for expanding internationally (when to use an EOR, set up an entity, compensation benchmarks, and more).

Subscribe and share the OnlyCFO newsletter with your teams

📚 Other Interesting Things:

Learn the Numbers

So many leaders and founders today don’t understand the numbers. And that will be a problem as they try to scale…

Forward my newsletter to your teams so they can get smarter on the numbers :)

Anthropic’s Revenue

The impact on all of our P&Ls from “tokenmaxxing” can be clearly seen in the unprecedented revenue growth rates of ChatGPT and Claude. We may never see something like this again…

Nice article, very thoughtfully written. Yes, COGS will go up but the salary expense will go down because we will use less number of people because of AI, not proportionally though!

When i was working in a company that did many projects, I coded each project in the general ledger so that we know at the end of the day whether we are making money in the project or loosing our pants & shirts. Perhaps, we need to code AI expense by department so that we can account for it correctly?

Love this... By coincidence, today I created a post on token flow that probably hit LinkedIn within minutes of yours: https://www.linkedin.com/feed/update/urn:li:activity:7465081155164258304/

As usual, we seem to be thinking about the same things, you and I. Though in my case -- at least for this post, I veered away from the gross margin discussion (though I've been thinking and talking a lot about that over the past 6-12 months).

One thing I'm wondering about -- and you'd know more about this than me -- is there a world where if the token consumption is your customer (as opposed to your employees) using tokens which they buy through you because you are delivering the overall solution... are there some scenarios where you as the vendor, can book the NET and not the gross?

Analogous to how some SaaS vendors have historically booked payments revenues (net vs. gross).

If true, this might mitigate the negative impact on gross margins associated with the cost of the customer-facing token usage.

Just wondering...