2024 GTM Benchmarks

Public and private company sales & marketing benchmarks. What's good? What's bad?

The OnlyCFO newsletter has been sponsored by some of the very best finance solutions. I love being sponsored by companies that are very relevant to my audience and can help folks run their companies better.

Today is no different with Meow. They help solve real problems faced by every company.

Today’s Sponsor:

🐱 Meow: Business banking, with interest. (Meow is a financial technology company, not a bank)

When thinking about banking for your business, did you consider whether your checking account pays interest?

It might be easy to forget. Meow finds banks willing to pay interest on business checking accounts, not just on idle cash. Some other benefits:

Zero wire fees on checking accounts from Meow’s partner banks.

Earn up to 5.02% Annual Percentage Yield subject to rate sheets from FirstBank, a Tennessee corporation; Member FDIC;

Earn unlimited up to 2% cash back with the Meow Card. (The Meow Card is issued by Community Federal Savings Bank, Member FDIC, pursuant to a license from VISA U.S.A. Inc.)

Software Benchmarks

ARR Growth Challenges Continue

Revenue growth continues to decelerate across company sizes in 2024. Budgets continue to tighten in a tough environment for software companies. But I know companies are at least making room for AI investments…

Below is benchmark data from ICONIQ’s most recent report:

Another interesting way to look at the above data is the endurance of the ARR growth by ARR buckets from one year to the next (e.g. 2024 growth / 2023 growth). It’s clear that the most impacted by slowing revenue growth are startups and the least impact are the large at-scale companies.

For companies <$25M in ARR, 2024 growth is only 66% of what it was in 2023. Growth for this bucket dropped 85 percentage points over one year!!🤯 That is HUGE…

On the other hand, more mature at-scale companies only saw ARR growth decay slightly — 35% growth in 2023 vs 30% in 2024 (86% endurance).

What does the differences in declining revenue growth tell us?

Two possible explanations that I see continuing to play out:

Fear of buying from startups. “Nobody got fired by buying from [name a big well-regarded company]”. Buying from startups for any critical and/or highly visible tool feels A LOT riskier today because of the startup company risk in this environment and buyers are a lot less willing to bet their career on an unproven tool today.

Vendor consolidation push. We are all trying to be more efficient so many of us are consolidating tools and focusing on larger vendors that can meet several needs versus lots of different point solutions.

Early stage companies need to continue to further de-risk the purchase decision because it’s been getting harder to compete against bigger companies as these two things continue to play out.

Public Company ARR Growth:

The below public company benchmark data tells a similar story for mature cloud companies. On the bright side it looks like ARR growth actually started to pick up in Q2.

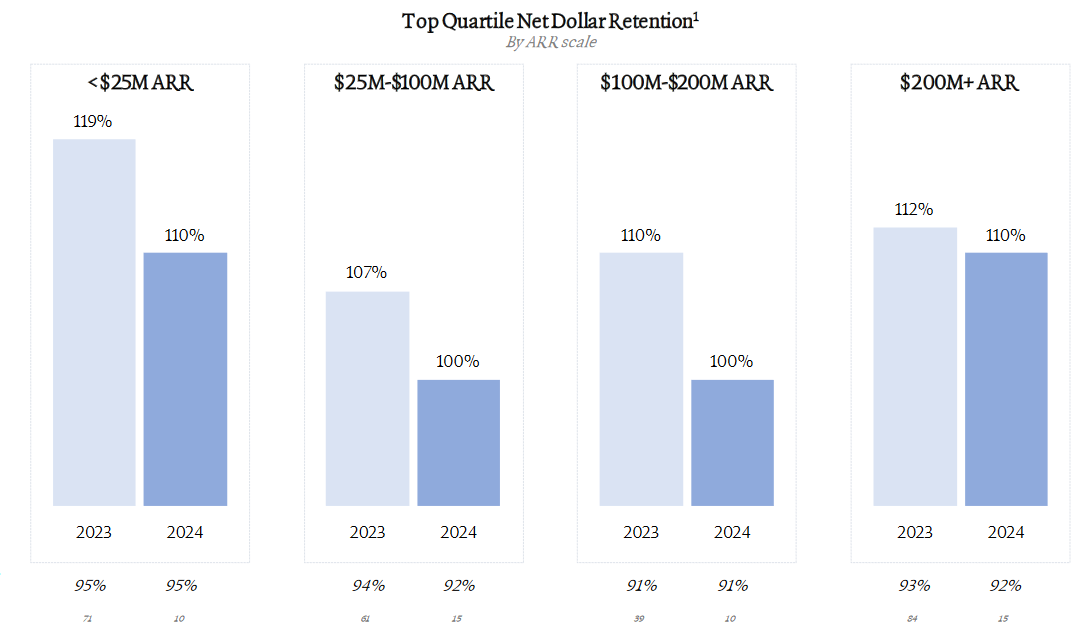

NRR is Falling

NRR (net revenue retention, aka NDR) has been falling since 2021 for most companies. This NRR story lines up with the overall ARR growth decline discussed above. It’s hard to grow fast when the easy expansion opportunities are declining and churn is increasing.

Public company benchmarks: public companies follow a similar pattern. And the bigger they are, the harder they fall — Snowflake’s NRR dropped 47 percentage points since 2021! That is 47% of easier ARR growth that just vanished.

LTV/CAC Thoughts

I am generally not a fan of private company LTV/CAC benchmarks for a few reasons:

For companies with <$25M in ARR the calculation is usually misleading:

Not a fully built out GTM motion so CAC isn’t realistic for when you are actually at scale. Startups bragging about their LTV/CAC of 15+ is just silly…

The LTV calculation is wrong because there isn’t enough churn data (you can get this to be somewhat accurate but that is a post for another day)

Private company benchmark data will have a lot of different methodologies (accounting treatment, customer life, etc) which can significantly change the LTV and CAC numbers

There are way too many variables in LTV/CAC to make it a useful operating metric.

Understanding the LTV/CAC ratio is important because it is ultimately what drives cloud valuations, but don’t over analyze it. In many ways the LTV/CAC ratio is like a discounted cash flow (DCF) model - in theory it is perfect, but in practice it is always very wrong.

Contract Term Length is Increasing

I actually found the below a bit surprising - contract terms are increasing. Most companies I speak with are trying to limit multi-year contracts on the vendor side (most of us like it on the customer side though because it limits churn).

Having said that, with more companies buying more from larger companies as mentioned above, this trend actually makes sense. Companies are much more likely to sign multi-year deals with large companies.

My contract term length policy: any new vendor must be one year max (with very rare exception) and then we can consider multi-year if certain criteria are met:

Discount for multi-year is worth it

Software is critical

Internal champion signs in blood that they need it and won’t switch

Confidence in vendor and roadmap/innovation

CAC Ratio

The CAC (customer acquisition cost) ratio has skyrocketed since 2021. The below chart from BenchSights shows the CAC ratio for public cloud companies.

CAC Ratio = S&M spend / Net New ARR

In Q1 2021 it cost public cloud companies $1.61 to acquire $1.00 in ARR, but today it costs them $2.26 for $1.00 in ARR. That is a 40% increase!

Sales Attainment

A big reason for this massive CAC increase is the drop in sales rep attainment. When sales reps are beating quota everyone is happy because not only are sales reps making piles of money, but each incremental dollar in sales is much more efficient.

Large company quota attainment has continued to decline while smaller company sales quota attainment has started to recover.

Benchmarking Caveats

When comparing benchmarks, it’s important to consider the population and firmographics of the benchmark data before trying to compare. Benchmark data is usually separated by:

Public company

Private company

Public Company:

When comparing public companies data then of course you can just use the publicly available data sets of the most relevant companies. It is important to consider revenue scale and other company specific factors when making comparisons.

Private Company:

Private company benchmark data is not as straight forward though because of the following:

They don’t have individual company data so you don’t really know what you are comparing against. For example, some benchmark reports just show top quartile metrics. Companies are often not top quartile in every metric so if you compare to all the top quartile benchmarks your expectations may be unrealistic

High diversity in accounting and metric definitions amongst private companies. The earlier stage companies may define and do things VERY different so the data is less reliable.

Very different firmographics of companies in data set. Understanding who performed the benchmark report and the firmographics of those companies is critical.

When benchmarking with private company data you need to make sure it’s really relevant to your company before using it as a comp.

For example, I referenced a recent GTM report from ICONIQ above. ICONIQ produces some of my favorite private company software reports. But it’s important to remember that ICONIQ’s investment portfolio is comprised of super high growth VC-backed companies (they get some of the very best companies in the world). It is probably not very relevant to a bootstrapped company or highly profitable company that has a goal to be acquired.

Benchmarks Lag:

Like all benchmarking reports, the data is lagging because it is reporting on historicals. In a quickly changing environment, companies should understand the benchmarks but also consider how things are changing and adapt to where you want to be (not where other companies have been).

In today’s faced pace and quickly changing environment with generative AI, companies need to skate to where the puck is going, not where it was….otherwise they will be left behind. Benchmarks are informative though on trends, but just realize things can change quickly and they may not indicate where you want to be.

Concluding Thoughts

My constant reminder on benchmarks: Make sure you understand what you are comparing. I see way too many people blindly compare to some irrelevant benchmark.

For private companies, ask your investors for benchmarks most relevant to your company. They have lots of data and can share anonymized portfolio company data and/or provide insight on where they think you should be.

Understand the benchmarks, but skate to where the puck is going and not where it has been.

Footnotes:

Create an account with Meow and see what it can do

Need a fractional CFO and/or bookkeeper that specializes in software and tech? Reply to this email (or email onlycfo@onlycfo.io) and I will help you.

Check out OnlyExperts for your offshore accounting needs

From the vantage point of a ~25M ARR bootstrapped SaaS company; we've also seen a dip in NRR like you've outlined here, largely from a significant drop in expansion compared to prior years. Great job collecting all this data and packaging it into a quick, easy to understand post so at least we know we're not alone.

Solid pulse check on KPI trends.