Accounting is My Love Language

A guide to understanding accounting for software companies

Every successful leader I have worked with understands the basics of accounting. You can’t fully understand the health and economics of your business if you can’t read basic financials. The same is true for investors.

While the concepts are similar, every industry has specific accounting/finance nuances and terminology. In the below image are the basic accounting concepts folks need to understand.

PDF version of the image is at the bottom of the post.

What do financials tell us?

The three core financials are:

Income Statement (aka P&L, Statement of Operations, etc)

Balance Sheet (aka BS, Statement of Finance Position)

Cash Flow Statement (aka SCF, Statement of Cash Flow)

Below is a high-level explanation of each. Links to my prior in-depth posts on each financial statement is at the bottom of the post.

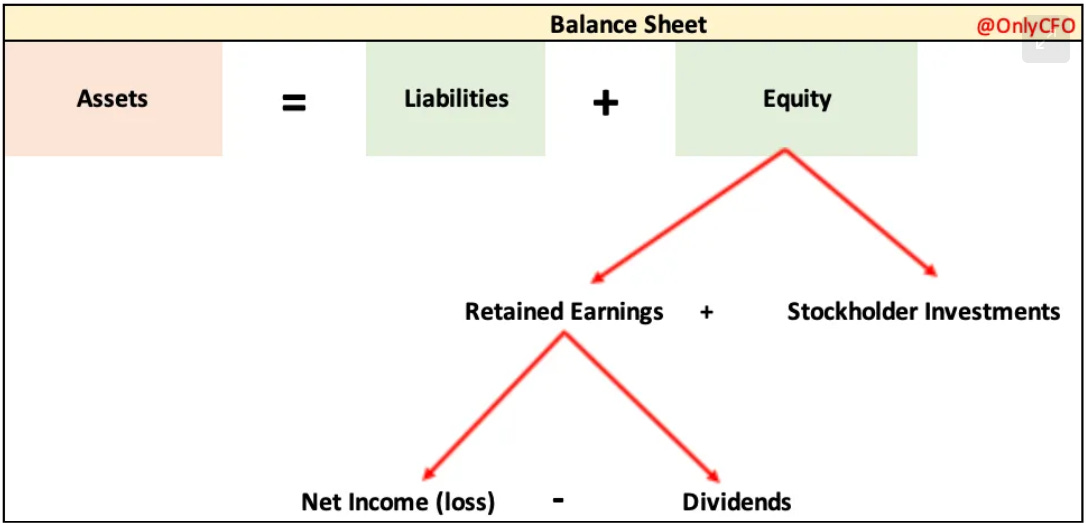

Balance Sheet

A balance sheet is a snapshot at a point in time of a company’s cumulative financial health. This is in contrast to an income statement which is for a specific period of time (monthly, quarterly, annually, etc).

A balance sheet includes three main sections:

Assets: What a company OWNS

Liabilities: What a company OWES

Equity: Value attributable stockholders

Income Statement

The income statement is a window into the performance of a company over a specific period of time by reporting on a company’s revenue and expenses.

A software company’s unit economics and current health is primarily seen from the income statement so it receives most of the attention.

However, the income statement by itself can be deceiving. All statements need to be reviewed together.

Cash Flow Statement

The cash flow statement shows the cash inflows and outflows of a company over a specific period of time. It starts with cash at the beginning of the period, shows the period’s activity, and then the ending cash balance.

Understanding a company’s cash position and how money flows in and out is critical for any business, but software companies have particularly unique considerations.

At the end of the day, a company’s ability to generate strong, increasing cash flows per share is all that matters.

How the Financials Tie Together

Think of the income statement as a sub-ledger of the balance sheet. As you can see in the image below, the income statement (represented by net income/loss) rolls up into the Equity section of the balance sheet.

What does this mean?

A balance sheet must “balance”.

Let’s say a company only has $100K of expenses in a month and no revenue. The accounting entry would be:

Debit expense for $100K

Credit cash for $100K

Cash (or “Assets” below) decreases by $100K so something else must also move for $100K for the balance sheet to balance. The other side of the above entry was to debit expense for $100K so there is a $100K net loss on the income statement.

A net loss causes a $100K decrease to the Equity section. So as the income statement rolls up to the equity section the balance sheet balances!

Unlike the income statement and balance sheet, there isn’t really accounting entries that are directly made for the cash flow statement. Rather the cash flow statement is a method for showing the changes in cash and the main categories for the flow of money.

Advice for Understanding Financials

First, you should read my prior posts for each of the financial statements (linked below).

Company leaders should understand how their accounting team is treating their costs in the financials and make sure it aligns to benchmarking used. And investors need to understand that it’s not always apples to apples comparisons.

Where expenses fall on the income statement can make a big difference on the budget allocated to a team.

Example: Some accounting teams put customer success managers in cost of sales (aka COGS). They are definitely getting less budget than companies who put them in sales & marketing. This is because COGS is a very protected expense line due to its importance with investors and a company’s long-term profitability potential.

Where some expenses get categorized on the income statement can be grey and inconsistent with other companies so make sure you understand how it’s done.

Further Learning

Once you have basic accounting knowledge, do the following:

Read your full financial statements.

Read your public competitors’ financials. You don’t have to read top to bottom every time, but I recommend doing it at least a couple of times so you know what’s in all the sections.

Listen to earnings calls. The Q&A sections are often interesting.

Good basic accounting overview for us readers who are not accountants.

This is an amazing read.