Cloud Valuations | Winners, Losers, and Insights

Lessons from valuation changes from the 2021 peak cloud bubble to today.

There has been A LOT of movement in revenue multiple rankings of public cloud companies in the past two years. The movements and reason for them provide some interesting insights for operators and investors.

There is only one public cloud company with a higher revenue multiple today than at the peak of the cloud bubble in 2021.

Keep reading to find out which company…

Today’s Sponsor: Remote.com

Ensuring HR compliance is crucial for protecting your company's financial health and reputation. Remote Watchtower, a comprehensive compliance safeguard integrated into our products, enables you to effortlessly navigate HR and employment law complexities, no matter where your team is located.

Our internal expertise and cutting-edge research tools guarantee extensive coverage, keeping you ahead of the curve and focused on strategic business growth. Gain peace of mind with our newest solution—explore Remote Watchtower today.

The software companies that experienced the highest relative increase in valuation multiples since peak 2021 bubble probably would have shocked most investors back in 2021.

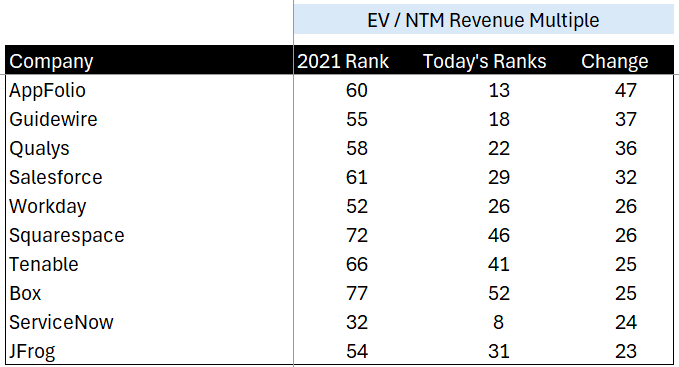

I compared the Enterprise Value (EV)/Revenue multiple rank of ~80 public cloud companies between November 2021 (what I consider the peak) and today. Below are the companies with the top 10 increases in ranking.

AppFolio has risen to the top by jumping a massive 47 spots since 2021.

Fun fact: AppFolio is the only cloud company with a higher revenue multiple today versus peak 2021. AppFolio had a 10.6x revenue multiple in November 2021 and has a 10.9x today. AppFolio is property management software and experienced just mediocre revenue growth in 2021 so it wasn’t a sexy company back then…..But AppFolio has continued to have good growth (unlike many other companies that had revenue growth fall off a cliff) and AppFolio continues to improve profitability so now it is sexy in 2024. Check out my previous deep dive on AppFolio.

Here are the biggest losers over the same period of time.

Amplitude led the pack in having their valuation decimated, plummeting from a 38x revenue multiple to 2.7x (from an $8 billion market cap to $1 billion) 🤯

Lessons from Valuation Multiples Changes

So the question is, what separates the winners from the losers?

Without looking at the data, the obvious answer should be the two primary drivers of valuation:

Better revenue growth

Improved profitability

But the more interesting insights from the data reveal how these movements impacted valuations.

Competitive Advantage Period

Bill Gurley discussed the concept of the Competitive Advantage Period (CAP) in a recent podcast.

CAP = the time which a company is expected to generate outsized returns. In other words, CAP is the life expectancy of the company's moat.

CAP is similar concept to growth endurance which I have talked a lot about.

Growth Endurance: this year’s revenue growth divided by last year’s revenue growth. In other words, how sustainable is revenue growth?

However, CAP puts the focus on the time period that a company should have high revenue growth endurance. For companies being valued in the high revenue growth bucket, knowing the CAP is crucial in valuing the company.

Many companies/investors assume the CAP will be a lot longer than it actually turns out to be. These are the companies that can crash the hardest when revenue growth falls quickly.

There are A LOT of AI companies that fit into this category. While their growth and perhaps profitability are strong, they lack a lasting moat that will endure in the AI platform shift; they are merely early adopters experiencing some success. Many assume that the CAP of these companies should mirror historical trends, but for 90%+ of these companies, I don't believe that will be the case.

The median growth endurance for the companies below is 21% while the median for all the other companies is ~50%.

Profitability

While many companies have dramatically improved efficiency and free cash flow (FCF) margins since 2021, people haven woken up to the fact that not all software companies can reach the same level of high profits.

The ZIRP era of 2021 was the peak of “grow at all costs” without much of a thought about profitability. Companies certainly have made a lot of improvements but the valuations that got crushed the most are the ones where 25% FCF margins no longer appear realistic (even if they have made dramatic efficiency gains).

Below shows a list of companies with the highest percentage point improvement of FCF (far right) and how the relative revenue multiples have changed over this period of time (far left).

You might initially be surprised to see that most of these companies with the highest FCF improvement actually became less valuable relative to the rest of public cloud companies. But most of these companies that improved the most were REALLY unprofitable in 2021 and despite dramatically slower revenue growth they are still not generating meaningful FCF margins. In other words, there is more doubt now that these companies will ever become meaningfully profitable so valuations got hammered.

For example, Fastly has improved its FCF margins by 30 percentage points (which looks amazing by itself), but at only 10% revenue growth now Fastly will only generate 1% FCF margins….That creates little faith that Fastly will ever become meaningfully profitable which is part of the reason is has fallen 26 spots in its revenue multiple ranking.

Takeaways

Competitive advantage period (CAP) is the most important thing to evaluate for high-growth companies. Historical trends may not be helpful in predicting the future, particularly with the AI platform shift.

Not all revenue is created equal. The software companies that have proven they can get to significant FCF margins have performed the best.

Hype and high revenue growth can be dangerous. They lead to high valuations but if the high expectations don’t hold up then they can come quickly crashing down.

Footnotes:

Check out Remote’s comprehensive compliance safeguard, Remote Watchtower

My sponsorship slots are almost full for this year! Grab one of the last spots

Looking for fractional CFO and/or bookkeepers that are experts in the software industry? Email me at onlycfo@onlycfo.io and I will introduce you to some folks.

Something interesting I have recently read - How safe are stock in the long run

Do you have any resources on evaluating or calculating a CAP?

Love the concept of growth endurance. Would you have a benchmark for early stage SaaS?