Domo: Cautionary Tale of Hype & Inefficiency

There are a lot of Domos out there today and most will go just as terrible...

Josh James (founder/CEO of Domo) originally gained fame from a tech company he founded called Omniture which went public in 2006 and later sold to Adobe for a whopping $1.8b in 2009. During this time, Josh was the youngest public company CEO on the Nasdaq and NYSE. He seemed to be “some kind of wunderkind”.

Then in 2010 Josh founded Domo, which was believed to be positioned to be even bigger than Omniture…

Second time software founders with one amazing exit already under their belt are hard to find today, but in 2010 it was nearly impossible. So when Josh founded his second company there were plenty of VCs willing to open their wallets to shower him with money. Domo raised about $700m before it went public at a peak valuation of $2.2b.

Fast forward to today and Domo’s valuation is a mere $445 (even less than its $511m valuation at IPO 5 years ago).

The point of this post is not to kick Domo while they have been down for the past 5 years — they have been doing that pretty well themselves. But rather illustrate the issues and provide their story as a cautionary tale to both operators and investors.

Domo was an early example of a software company being over funded and overvalued, but there are a TON of companies today on a very similar path to Domo.

Extreme inefficiency and weak revenue growth endurance are related and will be incredibly common with these companies. Many will hit a growth wall and struggle to ever have meaningful profits.

Excel-Induced Valuation Hallucinations

Some analyst at a VC firm put together a Microsoft Excel model to determine the potential valuation of Domo to get to the $2.2b valuation. The reason the valuation ended up being WAY off is because revenue growth didn’t continue the way they modeled it. And they definitely looked past the horrendous inefficiencies assuming they would get better…

Power of Growth Endurance

One of the less appreciated metrics for software companies is a company’s revenue growth endurance. Growth endurance is the rate of revenue growth that is maintained from one year to the next. While companies might be able to accelerate growth in one year, over the long-term growth rates decay as a company matures.

The speed of decay can have a HUGE impact on the valuation potential of a software company because the vast majority of value from software companies comes from the outer years as a company starts to mature and generate significant free cash flow margins.

Take a look at the 4 hypothetical companies below with varying levels of growth endurance. They all start at $10M ARR and 100% year-over-year growth rates.

Company 1 has a growth endurance of 90%, which means its revenue growth in each year will be 90% of the previous year. This would be an amazing growth endurance.

Company 4 on the other hand only has 65% growth endurance.

Company 1 with a 90% growth endurance ends up being 3x to 18x bigger than the other companies! Domo’s VC investors incorrectly assumed its growth endurance would look like Company 1 when it actually ended up a lot more like Company 4.

Historical growth endurance is an important metric, but growth endurance often isn’t linear. Many companies can hit a wall after several periods of high growth (particularly when it’s forced by high inefficiencies).

Team and an innovative culture are critical for sustainable growth endurance. Technology is rapidly changing (especially right now) so if the team and culture doesn’t produce innovation that can continue to grab the market then growth endurance will eventually plummet. Companies need 2nd, 3rd, etc products to keep growth endurance high but without a best-in-class team and culture then that won’t happen.

Inefficiency is a symptom of bigger issues

When Domo filed to go public there were A LOT of red flags (almost as bad as WeWork). But one of the biggest flags was its extreme inefficiency. Domo was able to achieve $100M in ARR in a relatively short-period of time, which made a lot of VCs excited to throw money at Domo at ludicrous valuations, but they burned eye-watering amounts of money to get there…

Domo burned ~$740M in order to get to $100M in ARR 🤯. So it cost Domo $7.40 for every $1 of ARR by the time of their IPO….They burned through all of the VC money and were dipping into their $100M in debt by the time they IPO’d.

This type of extreme inefficiency means there are major issues at Domo such as:

Lack of product/market fit (PMF)

Bad management

Broken culture

Competitive problems

These types of issues guarantee a lower growth endurance rate in addition to terrible unit economics that will never work. Companies with efficient unit economics aren’t only more profitable but their growth endurance is likely much more sustainable. Inefficient companies hit a growth endurance wall very quickly once spending starts to get reined in.

Domo Red Flags

Lack of focus

Below is a phrase that was repeated several times in Domo’s S-1 and other places as a flex.

In many ways, building Domo was like building seven start-ups in one.

The only way Domo was similar to “building seven start-ups in one” is that they burned an incredible amount of money and the chance of failure is still REALLY high.

Bad Management

In 2015 when Domo likely had <$50m in revenue Josh said the below as if it was a good thing. In reality it’s probably a red flag of bad hiring that likely led to Domo’s extreme inefficient growth and ineffective strategies…

If an early stage company with <$50M in revenue actually has a management team for a $5b revenue company, then they 100% have the wrong people because what is required at a $50M company is MUCH different than a $5b company.

Quick growth deceleration

Domo’s subscription revenue growth for the full fiscal year preceding the 2018 IPO was only 49% and the subsequent quarter was only 40%. Good revenue growth rates are a function of revenue stage and efficiency to obtain that growth. Domo was barely doing $100M in ARR and had efficiency metrics that will make your eyes water.

James was quoted saying before the IPO that his company was so advanced that “we don’t really have a competitor yet.”

And then just a short time later in their S-1 for the IPO the lawyers made him tell the truth: “The market for our platform is intensely and increasingly competitive”. The lawyers then made Domo list about a dozen competitors (all of which have been around a while…)

Customer stickiness and expansion was weak

Net revenue retention (NRR) is a key metric for cloud companies as it tells you how fast a company can grow if it wasn’t to add any net new customers.

Domo’s NRR was 105%…remarkably low given its product category and target customer being in the enterprise segment. Below are Bessemer’s benchmarks of average retention rates.

Burning huge amounts of cash

Domo has $72m of cash as of the end of the quarter before the IPO and was burning ~$37m/quarter. Their cash balance included $100m in debt which was maxed out.

In other words they would be out of money in <6 months if the money from the IPO didn’t come in — they were backed up against a wall with no good options. A lot of software unicorns will be in a similar position soon…

Domo listed that if equity/debt financing wasn’t available by August (2 months away from their filing) then they would have to implement plans to significantly reduce costs.

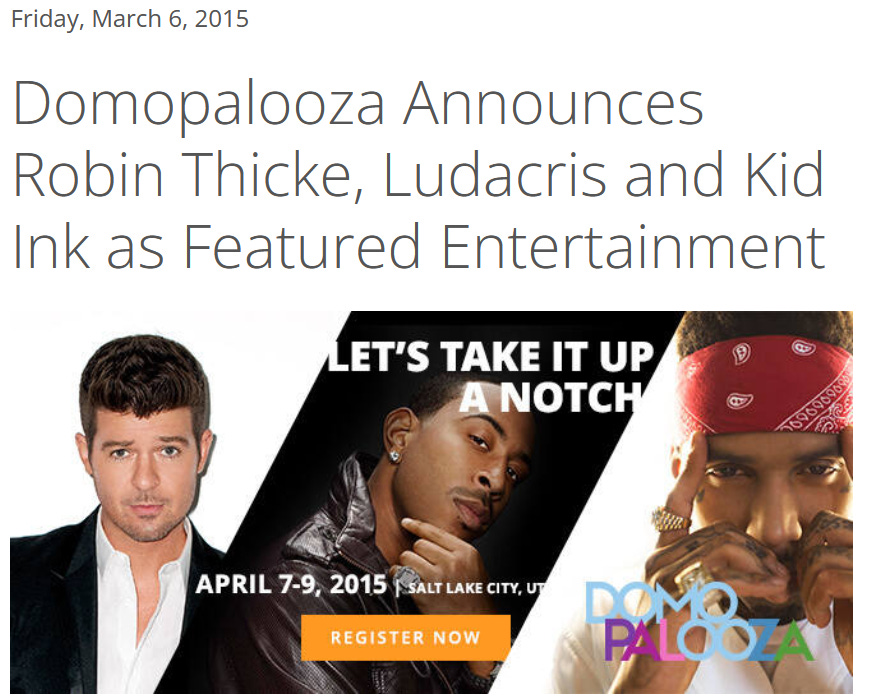

Take a look at their entertainment lineup for their company conference when their revenue was <$50M…likely extremely costly…

Funny business

The inefficiency, questionable culture, and management practices were on full display when Domo revealed some of the related party transactions and other things it did in the IPO filing:

Spent $2m on a private jet lease owned by Josh James (CEO). Bad optics to enrich yourself from your other businesses but really crazy to spend that kind of money at the scale and inefficiency levels of Domo.

Spent $1m between two different businesses Josh had ownership in with his brothers…a restaurant called “Cubby’s” and a design company called “Alice Lane”.

Why Domo IPO’d

There are two main reasons Domo had to IPO and they are related: 1) needed cash asap and 2) clean up the cap table.

Domo knew that they weren’t anywhere close to being valued at $2.2B anymore. If they were to raise more money in the private markets, it would have come at a big down round with a lot of deal “structure” that protects and provides outsized return potential to investors.

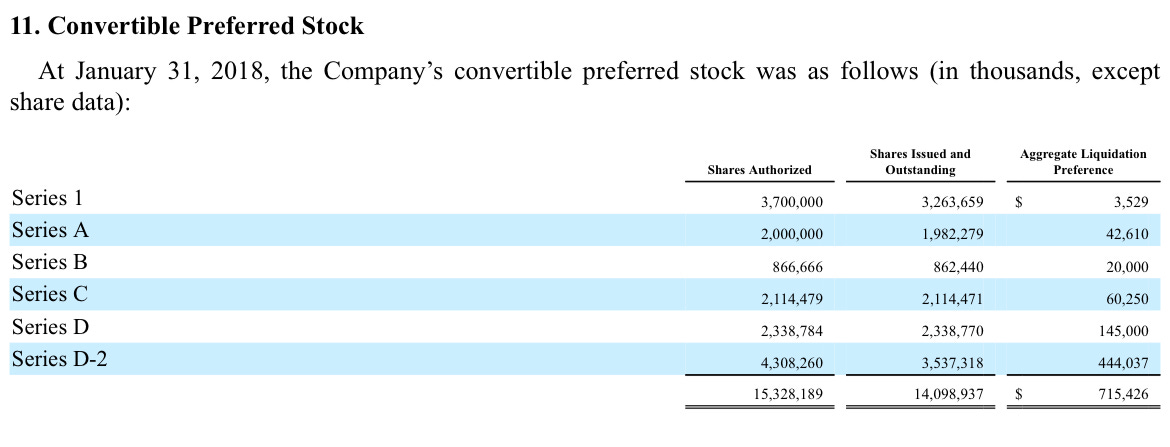

When a VC gives a company money they get “preferred stock” which includes rights that the normal founders/employees don’t get. One of the significant preferences they get is a “liquidation preference”, which basically means they get a multiple of their money back before anyone else gets any money in the event of a sale of the company. When things aren’t bad, the liquidation preference is typically 1x the money invested.

In Domo’s case, all of their funding was raised at a 1x liquidation preference which meant that the first $715m of any sale would go to payback the VCs first. Anything over $715m would go to founders and employees.

So if Domo decided to sell the company instead of going public at $511m, then the investors would recoup some of their $715m and employees get nothing. If Domo goes public though…then all the preferred shares automatically convert to common stock and there is magically no more liquidation preference (everyone is treated the same). The cap table gets cleaned up and all preferred stock structure goes away.

So if Josh owns 15% of the stock at the $511m IPO price then he has $79m worth of stock he can sell, but if they were to be acquired for $511m then Josh is sad because he gets nothing.

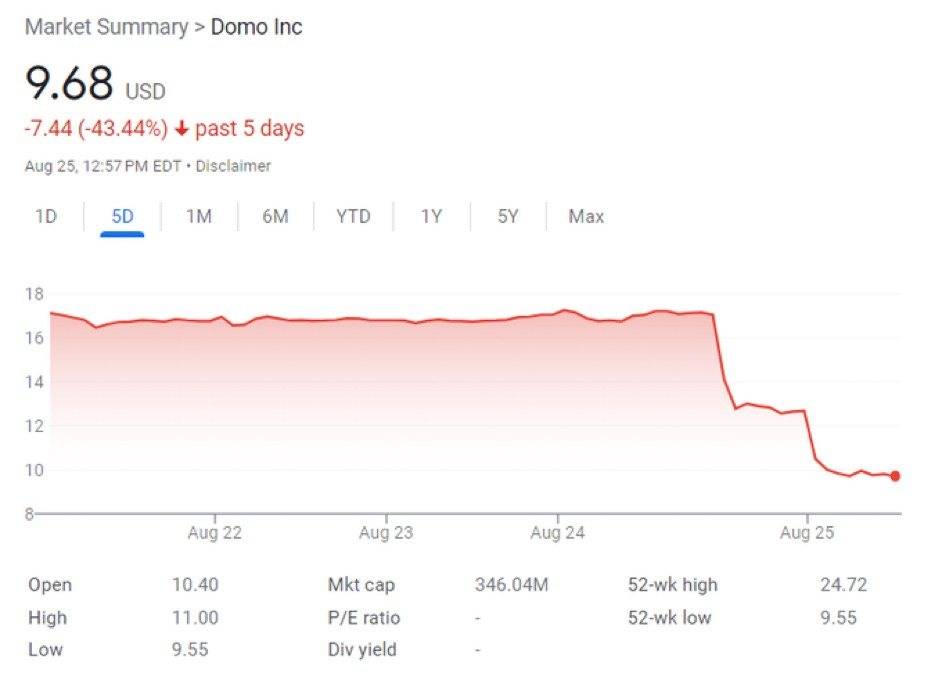

Domo’s Horrible Q2 Earnings Release

Let’s now fast forward to today and see where Domo is now. Domo’s revenue growth followed the trajectory of Company 4 in the example companies above while it continued to be incredibly inefficient.

Domo released its Q2 earnings last week and it continues to not go well…

There are two primary components of a good quarter to have a stock price jump up:

Beating consensus actual results

Raising forward guidance above consensus

This is what is referred to as a “beat and raise”. Consensus refers to the average of all the estimates from equity research analysts that cover a stock. There are two primary consensus metrics looked at:

Revenue - for software companies this includes things like ARR, billings, RPO as revenue is a lagging indicator

Earnings - includes things like earnings per share, FCF margin, shareholder dilution, etc

Management’s revenue and earnings guide is typically conservative so beating its own guide is table stakes while beating consensus is critical for a successful quarter in terms of the stock price.

Domo beat consensus on both revenue and earnings results for Q2. So the stock price did OK, right? Wrong…

Domo’s guidance (2nd and even more important piece) was really bad— cutting revenue growth guide in half (from an already low number) and provided guidance of a much higher loss per share ….As is evident from the post sales price crash, the market wasn’t happy.

Domo currently has one of the lowest EV/revenue multiples amongst all public software companies with a 1.4x multiple.

Revenue growth endurance has been bad (growth continued to hit a wall and customer churn is high). Efficiencies haven’t really come since Domo has matured and revenue growth flattened which is likely a result from one the bigger issues I mentioned above.

Domo’s Path Forward

I get why Domo thought it needed to IPO (for reasons above), but it was probably not the best choice. What they should have done (and still should do) is get really efficient so they can control their own destiny.

Let’s pretend instead of an IPO that Domo became radically efficient. Its revenue growth would be smaller, so let’s pretend its ARR today is $200m instead of almost $300m. But it has 30% free cash flow margins. That business would almost certainly be worth more than its $440m valuation it has today…

Having said that, based on how Domo has been operated I don’t think they have the team, culture, etc necessary to drive that kind of efficiency change so their best path forward is likely to look for a strategic acquirer that values the customer relationships and the tech. But since voting control sits with Josh (given the dual-class structure that gives him 40 votes per share) a sale is entirely up to him.

There are a lot of companies in similar positions to Domo right now. Received high valuations and too much money which has made them be inefficient as they try to grow into that valuation. Don’t make the same mistakes as Domo. Sometimes companies need to slow down in order to speed up. Becoming more efficient and having good unit economics opens up a lot more doors of possibilities.

Reading

Check out the latest accounting memo (internal use software) I added to the free template page. Special thanks to Brian Weisberg for helping me with it!

Great article. I cross-posted this to my channel; hope you don't mind. Feel free to cross-post anything I have.

Exceptional article. Thank you! (I don't feel so bad about buying brownies and cookies from my sons (11) business for our company off-site now. I just hope he doesn't see this article! $1m!!!)