How Low Can Figma Go?

Breaking down Figma’s post-IPO performance. And some lessons learned

Brought to you by…Deel

Payroll is entering a new era with AI-driven compliance, real-time visibility, and higher expectations from the board.

Deel’s Payroll Strategy Toolkit gives finance leaders a step-by-step roadmap to modernize payroll, reduce manual risk, and build a scalable strategy with confidence.

Figma’s Wild Ride

Figma has been on a wild rollercoaster ride since going public just 8 months ago:

IPO on July 31, 2025

250% IPO pop

AI disruption fears and stock volatility

Heavily invests in AI

80%+ stock decline since

Shareholder lockup expired on Jan 27th

Figma went from a 50x NTM revenue multiple right after the IPO to just 12x today…Falling from the second highest revenue multiple (2nd only to Palantir) to the 13th highest (out of 75 public software companies).

Did Figma’s Key Metrics Deteriorate Since IPO?

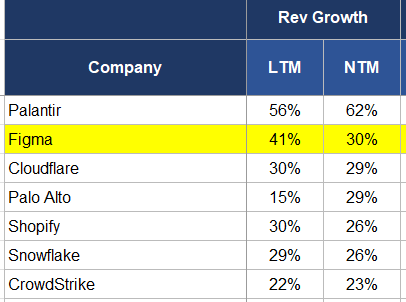

2nd Highest Revenue Growth

Figma’s revenue growth is still the second highest on an LTM and NTM basis. So this isn’t the culprit of the falling stock price. Although growth fell more than some were hoping (more on this below).

Weakening Faith In Revenue Durability

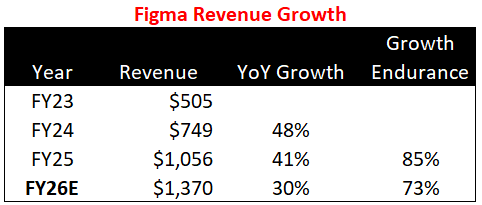

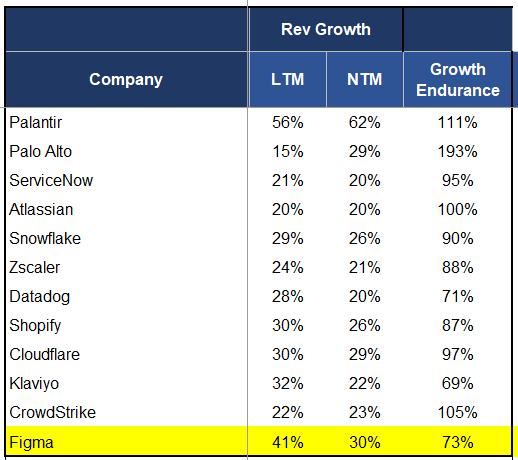

Figma has decent revenue growth endurance (prior year growth rate / current year growth rate), but it is declining faster than others.

Relative to all other public companies with higher revenue growth, Figma has nearly the weakest growth endurance. In Figma’s defense though, they had a higher starting revenue growth rate so higher growth endurance rates are harder.

Revenue durability is the #1 concern I have when investing today. And it’s not just NTM revenue. It’s 2+ years out. Understanding this far out feels like a bit of guesswork in the age of AI (and it is), but there are some early warning signs…like current weak growth endurance.

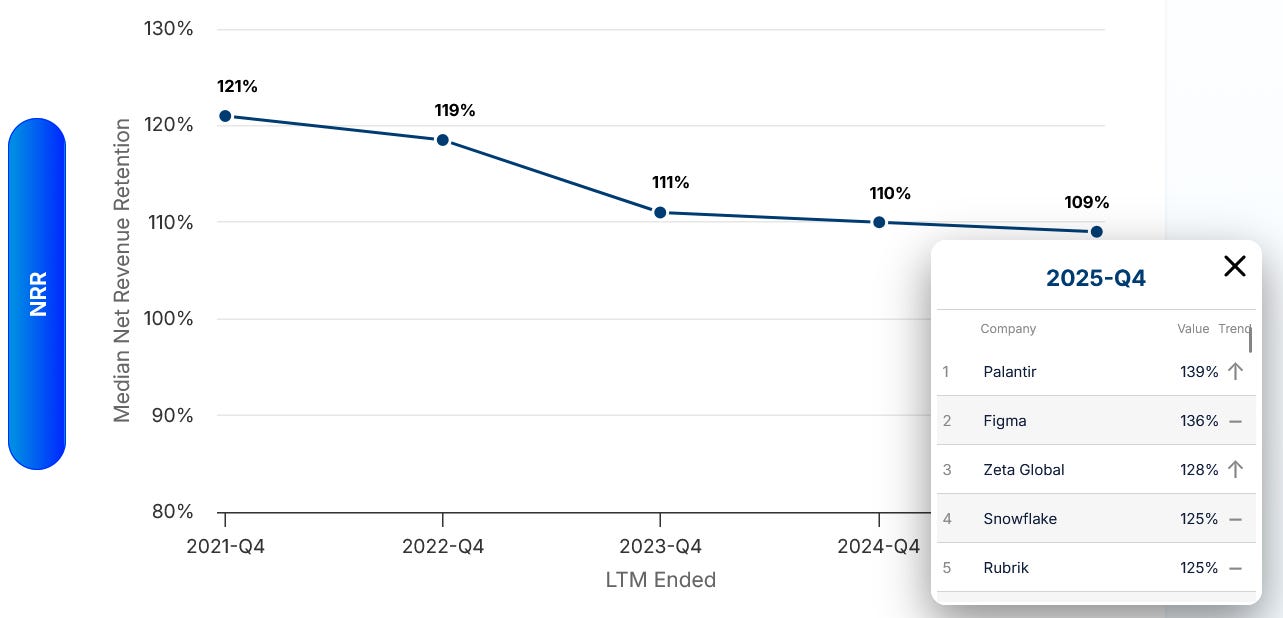

When Amazing Retention Might Also Signal a Revenue Durability Issue

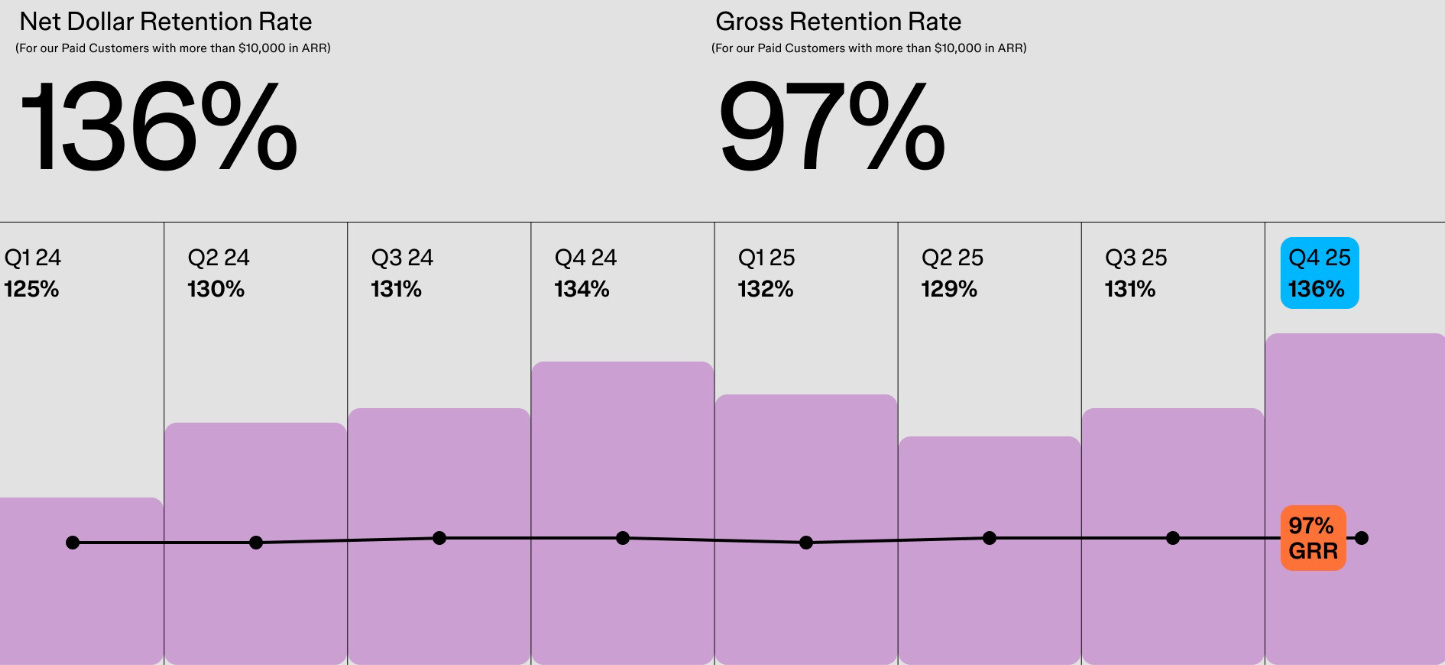

Figma has crazy good retention numbers. And they have gotten even better! Almost no one else is doing that right now. The increase was driven by the release of new products (particularly the AI features).

The median public company NRR is much lower (just 109%) and Figma has the second highest NRR (again, second only to Palantir).

So why would increasing/strong NRR be a bad thing? It’s always good, right?!?!

Strong NRR isn’t bad in isolation. But it may signal potential issues when evaluated with other metrics….

Figma’s revenue growth rate has weakening growth endurance but their already strong NRR is rising. This means that revenue growth from new customers is slowing even faster and they are relying on expansion revenue to hold up overall growth.

Figma raised prices last year, introduced new products, and pushed AI products hard. All of this is good for NRR in 2025. But most of it will be hard to regularly repeat.

The ratio of new customer growth vs expansion is an important indicator for long-term growth. It’s why I always review the break out of growth rates at my company.

We don’t have this level of detail for Figma, but we know the new business growth is dropping faster than the overall growth rate. And that is a potential problem for long-term growth rates if it continues.

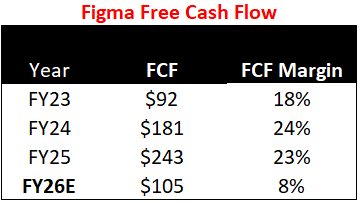

Rapidly Declining Free Cash Flow:

Figma’s decline in FCF margins is obviously a concern…

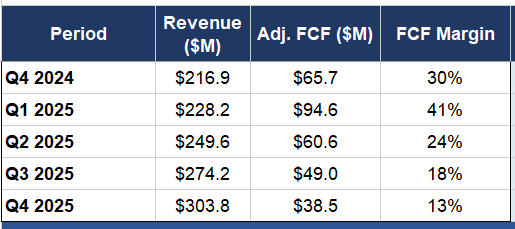

Looking at FCF on a quarterly basis gives an even clearer view. FCF margins were amazing in the quarter immediately before the IPO (surprise surprise), but it has been on a rapid decline since then and projected to be even lower in FY26 (just 8%)

So what happened? What is the justification for the shrinking FCF margins?

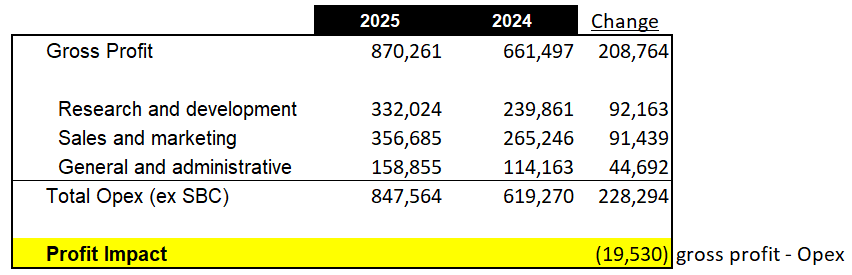

Expenses ran hot in 2025: With slowing revenue growth you generally expect that expenses will not outpace gross profit additions, but that is what happened. Figma increased gross profit by $208M but added $228M of operating expenses (excluding SBC).

Investing in AI: Their main excuse for declining FCF margins is investing in AI. And it’s theoretically a great reason. If Figma doesn’t invest in AI disruption, then their long-term valuation is toast.

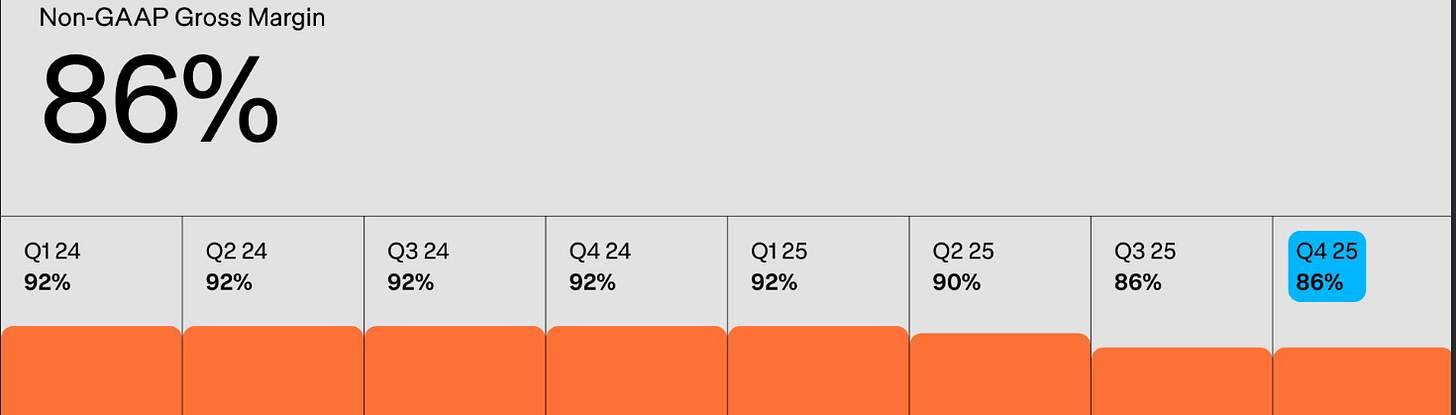

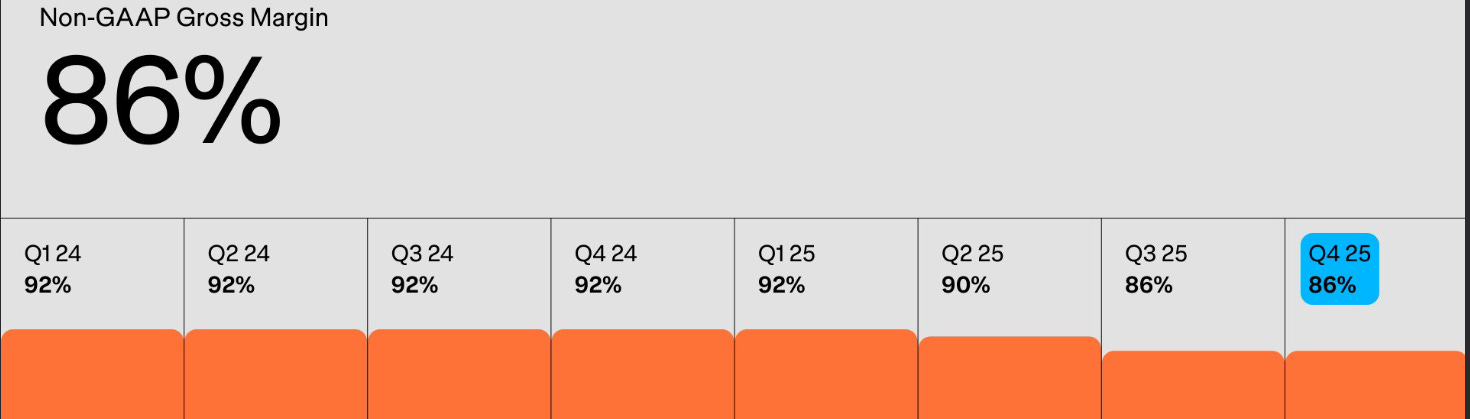

Decreased gross margins because of higher infra and inference spend for AI products. Figma (like many AI companies) is currently subsidizing their AI features to gain adoption.

Increased R&D costs: Need more people and higher infrastructure costs to build out AI stuff.

Increased S&M costs: More free users playing with AI stuff (drives S&M costs up). And they need more sales and marketing to sell new products and meet growth targets.

Making these hard financial choices is really hard (especially when you are public), but if you mentally accept that your terminal value will be zero if you don’t then it is a bit easier. This is easier for some companies than others. Figma has to move faster than most…

Also, if Figma can’t see a path to beating their 8% FCF expectations (and revenue growth), then they will likely feel pressure to do a layoff. There isn’t much investor appetite for weak FCF margins without extraordinary revenue growth in 2026.

What’s Next For Figma?

Figma needs to adapt faster to AI than most other companies because 1) their products have a higher AI disruption risk and 2) their customers can more easily leave (i.e. churn).

There are a lot of concerns investors can have with Figma, but based on their financial investments they seem to be making the right (albeit hard) decisions to rebuild as a real AI company.

The big question for Figma (and so many others) is if what they are building will add enough incremental value beyond the base models to be worth the extra cost and can their unit economics survive the pricing pressure that is coming.

Figma has customers that love them and a fantastic team (I know many of them) so I definitely wouldn’t bet against them.

Footnotes:

Download this guide and up-level your payroll for faster, more compliant processing and building a scalable strategy in the age of AI

Reply to this email if you want to sponsor OnlyCFO

*nothing in this post should be considered investment, tax, or legal advice. Do your own diligence.

The FCF line is probably the clearest tell in the whole piece. Going from 41% margin in Q1 to 13% in Q4 does not look like a company just investing a bit more for growth. It looks like a company that started the year optimizing for an IPO window and ended it spending much more aggressively.

What makes that more interesting is where the pressure shows up. Figma had been running at 92% gross margin for more than a year, which is exactly what you would expect from a browser-based design tool with very low inference costs. That is about as clean as SaaS gets.

So when gross margin drops to 86% in two quarters, it is hard to call that noise. It points pretty clearly to the cost of pushing AI into the product and subsidizing adoption.

The real question now is whether this level holds or keeps slipping. If every new AI feature drives engagement but also pushes up COGS, then the underlying economics of the product are starting to change.

One factor to pay attention to might be the catastrophic job losses among UX designers of the past 2-3 years. Staffs are being slashed and design is being pushed further and further down the value chain, probably permanently. There are a number of factors at work here, most of which are well-documented. Designers seem to have been caught flat-footed, but that isn't new.