More Lies of Stock-Based Compensation

Equity compensation is the most misunderstood expense

Brought to you by…Deel

Global payroll costs extend far beyond salaries. This guide breaks down international payroll expenses, compliance costs, and hidden fees so you can forecast accurately, reduce risk, and improve cost efficiency as you scale. Built for finance leaders managing multi-country operations.

The Hidden Costs of Stock-Based Comp

With the collapse of software valuations, stock-based compensation (SBC) expense is being debated again. But these discussions usually lack real substance so they aren’t helpful.

The question is not “Does SBC expense matter?” Of course SBC matters. All else being equal, lower SBC expense is obviously better. But the “How much should we have?” and “How to measure it?" are much harder questions to answer.

Bill Gurley (VC at Benchmark) kicked off the discussions last week with an article where he argued that software folks are finally waking up to the real cost of stock-based compensation. Here is his final paragraph:

The current environment is revealing a cost that was always there, hidden in plain sight behind an add-back. The companies that navigate this well will be the ones that start doing the honest accounting — treating SBC as what it always was: compensation, denominated in cash, paid for by shareholders.

We knew that high revenue growth in the software industry was hiding a lot of sins of inefficiency (both cash expenses and non-cash SBC sins). But the promise of extremely high future profitability and the large revenue multiples that came with it were justifications for those inefficiencies.

Since software efficiency metrics and shorthand valuation metrics ignore SBC, the problem only becomes painfully obvious when revenue growth slows.

As they say, “when the tide goes out”…

While I agree with most of Bill’s article, our conclusions on what companies should do likely differ slightly.

I want to address 4 questions in this post:

Is the company’s SBC expense too high?

Is focusing on profitability a trap in 2026?

How should you measure SBC’s impact?

Will SBC drive more layoffs?

1. Is Your SBC Expense Too High?

Where I agree with Bill is that SBC expense is basically just like a cash expense. It’s a real cost that has negative impacts on shareholder returns. Essentially all of our metrics and shorthand valuation models completely ignore SBC. That created an environment of ignoring this real cost.

The ultimate long-term valuation of a company is determined by its FCF/share potential. Cash expenses decrease “FCF” while equity compensation (SBC) increases the “share” part. Both are bad for the metric.

High-growth companies:

If growth is strong enough and terminal values are high, then relatively high SBC expenses don’t really matter.

Yes. All else being equal, lower SBC is better. But if you are growing 100% YoY and SBC is kinda high at 5%….does anyone really care?…No.

You are growing the pie a lot faster than you are diluting it, so the tradeoff is acceptable.

Low-growth companies:

Most public software companies (and LOTS of privates) sit in this bucket today. And that’s why SBC is getting a lot more attention.

Revenue growth has slowed and terminal values have been decimated (thanks Claude :), which has crushed valuation multiples.

When this happens, investors value profitability a lot more (particularly near-term profitability). And folks start caring about SBC a lot more because near-term FCF/share drives the valuation.

The expectation has been that when a company’s growth rate slows and the future is uncertain (terminal value falls), then you cut expenses and focus on near-term profitability. This is how you maximize shareholder value given the new investor focus on near-term profitability (including the impact of SBC).

This is the private equity playbook - acquire a struggling business with decent retention (slowing growth, weak profitability, and/or out of control dilution) and prioritize extreme profitability.

However, I think this playbook is going to get a lot of companies killed in 2026 (see next section).

2. The Profitability Trap

The software companies that overly focus on FCF (and cutting SBC) over innovation in 2026 are going to get killed.

Byron is one of the smartest software VCs and he agrees with me…accelerate or die.

In the short-term I can see this playbook appearing to work. Investors may reward them with higher valuations because FCF/share increased while growth is little impacted.

But it’s not the next 6-12 months that matter…

It’s 12+ months out after long enterprise contracts end and customers have time to move off of tools embedded in their processes. It will quickly become a death spiral of churn, slow/negative growth, and weakening FCF margins.

Cutting cash expenses (and/or SBC expense) is not going to save your company in the Age of AI. We are in a “accelerate or die” technology shift.

Am I saying “growth at all costs” is back? That’s a dangerous thing to say, but…kinda. Doesn’t mean you should blow all your money, but if you don’t innovate then I don’t think you will be around in 18ish months…

We will see many companies that took the profits over innovation path that generate 35%+ FCF margins within 12 months. And then we will see them get absolutely crushed and that FCF/share will quickly sink to zero.

Be efficient if you can, but you must innovate and grow.

3. How To Measure SBC’s Impact

There are two ways to look at the impact of SBC:

SBC Expense (GAAP):

This is what most people look at. It’s the accounting expense that gets recorded on the income statement. But accounting rules can be misleading…

There are lots of complex rules, but essentially the accountants come up with a fair value on the grant date and then that same amount is expensed over the vesting period (regardless of what happens to the stock price).

The most common types:

Stock options: The default for private companies. To determine the fair value companies perform a Black-Scholes model and then that is the price that gets expensed over the vesting period.

RSUs: Public companies usually give RSUs and the fair value that gets expensed is typically just the stock price on the grant date.

Example: $1,000 RSU granted at $50/share with 4-year vesting = $12,500 expense per year over 4 years. It doesn’t matter if the stock price drops to $10 after 6 months. The expense is the same.

So is that $12,500 GAAP expense too high?

Without further information, I have no idea. If the stock trades at a 100x revenue multiple (when it probably should be 10x) then that is probably an awesome deal. Dilution is likely very low. If they had to pay cash instead then it would be a lot more destructive to shareholder value.

Similarly, if the stock trades at 1x ARR but management believes it should trade at 10x then that SBC is a lot more expensive because a lot more shares had to be given for that $12,500 GAAP expense.

The GAAP expense doesn’t tell us how it impacts FCF/share so comparing it across companies with different revenue multiples is pretty useless.

Shareholder Dilution:

Ultimately, shareholder dilution is what matters. There is no cash impact from SBC but existing shareholders’ slice of the pie shrinks and the FCF/share formula is negatively impacted.

There are a few ways you can look at dilution, but all of them are much more truthful than the GAAP expense.

4. Employee Equity’s Impact on Layoffs

Public companies treat employee equity like cash. It’s part of employee’s total comp. Essentially no different than cash. Employees typically get granted a variable number of RSUs to hit a target cash value on the grant date (e.g. $250k of RSUs).

So if a company’s stock price craters…the company has to incur a lot more dilution to provide the same cash value.

Let’s pretend that Amplitude (public SaaS co) hired 100 engineers when the stock price was $83 (glory days of 2021) and they gave $250K of RSUs that vested over 4 years. That’s $25M of SBC expense over 4 years and 301K shares being issued.

Fast forward to today and the stock price is only $5.90. If they wanted to give refresh grants to all those engineers of $250K, then they would have to issue 4.2M shares…The expense on the P&L would be the exact same for those new grants ($25M over 4 years) but dilution is 14x higher 🤯

Even if the company cuts back a lot on SBC, dilution would still be higher given how much software stock prices have fallen. You will also risk losing your best talent if you don’t pay good equity packages. You don’t want that either.

So what is the solution?

You likely have to do layoffs to help pay for the additional dilution required for competitive equity packages.

This is another reason companies are pushing AI adoption so hard internally. They need to lay off people to make the new math work.

Revenue multiples have compressed

A lot more dilution is required to pay same comp packages

Increased investor focus on near term profitability (FCF/share)

Terminal values have collapsed

If smaller revenue multiples are permanent (which seems likely…), then dilution from employee equity can quickly become a death spiral because the dilution would be significantly higher to maintain comp packages. Also, a lot of public company employees still have grants from when stock prices were much higher…when they get grant refreshes, promo grants, or company makes new hires then dilution will skyrocket.

Everything points to more layoffs coming….

Final Thoughts

The $250K of RSUs you pay to your engineer isn’t less real than their $250K cash salary. It just impacts a different part of the FCF/share equation.

But the analysis is the same…

Are you creating more long-term shareholder value by spending/diluting more today?

If the answer is yes, then keep spending. If no…then you need to cut back (on all expenses). SBC matters so be efficient where you can, but also…accelerate or die.

Footnotes:

Check out these offshoring costs by country (both salary and employer burden) so you can decide where to focus global expansion. *from my friends at Deel

Reply to this email if you want to sponsor OnlyCFO

📚Things I Found Interesting This Week:

Private Credit

Still looks messy. Not sure what will happen but there are plenty of people panicking

And guess where private credit has the most exposure? The industry that seemed like the ultimate gift to private equity firms, software.

I can’t imagine most places will be increasing their exposure in software….

How Low Can SaaS Go?

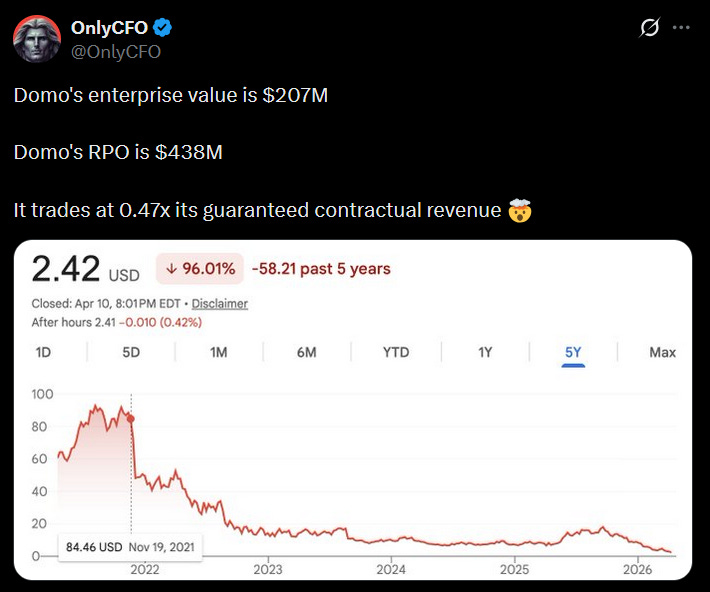

I am going to put my own tweet here because I think this is insane. Software can apparently go much lower…Domo trades at half of its contractual future revenue!

There are a number of companies that are barely trading above their contractual remaining revenue. This was unthinkable a few years ago, but investors are now saying the terminal value of some of these businesses is near zero. And future FCF is at risk.

Interesting data! Yes, I thought about also discussing buybacks but that could easily be a blog post by itself.

Where the analysis gets fuzzy is in theory if your stock is on tear (and you are potentially overvalued) then you shouldn’t do buybacks and you are better off using equity for comp.

Equity comp is a moving target cost which is what makes it so hard to compare to cash comp

One very easy way to think about the cost of the dilution involved -- imagine the company using buybacks each year to neutralize the dilution (from the vesting of RSUs and options)... subtract that cash from Free Cash Flow, and voila you have the "correct" profitability measure. (In fact, some companies actually do these buybacks!).

The ironic thing here is that for the companies whose share prices are on a tear, institutional investors (who generally are the ones setting the price) just don't care about SBC and dilution -- you pointed this out, of course... as did Logan. So we have this odd adverse selection bias going on in evaluating this. Gurley doesn't like this reality. He's a purist on valuation impact. But the investors will gleefully take their profits and not worry about the dilution.

As for figuring out a "better" SBC assessment... I went down a serious rat hole recently, extracting the current state of dilution from RSUs and options for ~70 public SaaS companies, so I could try and do a mark-to-market of "economic" SBC. It's summarized in this LinkedIn post: https://www.linkedin.com/posts/dspitz_saas-benchmarks-activity-7448431646141353985-bRAL . But beware, this is based on stock prices (from a week ago)... and those change!