Revenue Durability is Failing in the Age of AI

The #1 metric that every good CEO and CFO I talk to is thinking about

Brought to you by…Paraglide

Paraglide (AI platform handling billing inquiries, collections, and disputes) just raised a round led by Bessemer to enable companies to get paid on time with less manual involvement.

My AR teams have always spent way too much time in their finance inbox: answering billing queries, chasing customers, chasing down PO numbers, and handling disputes…It’s high-volume, boring, and repetitive. Which makes it a perfect place to use AI agents.

Revenue Durability

Every VC, PE firm, and public market investor has one question they are struggling to answer in 2026. This question has been crushing valuations, putting M&A on freeze, and making fundraising really hard.

Is the company’s revenue actually durable?

No one really has faith that software (or even AI) revenue is actually durable today. If you want to raise money, get acquired, or one day IPO, then this is the most important question to try to answer.

It’s really hard (near impossible) to honestly answer this question today. Long-term durability is too hard to predict in the age of AI. But below are some of the things I am thinking about as I talk to folks about this topic.

What is Revenue Growth Endurance?

Revenue Growth Endurance = (this year's growth rate) / (last year's growth rate)

It measures how fast a company’s growth rate is falling (or rising). The reason software/AI companies have been able to command such high valuations is because we believed that the revenue and FCF margins were very durable (as if they would be strong for 10+ years). Look at a DCF performed on any software company…90%+ of the valuation comes from 5+ years out.

Revenue durability expectations can cause some wild swings in valuations…

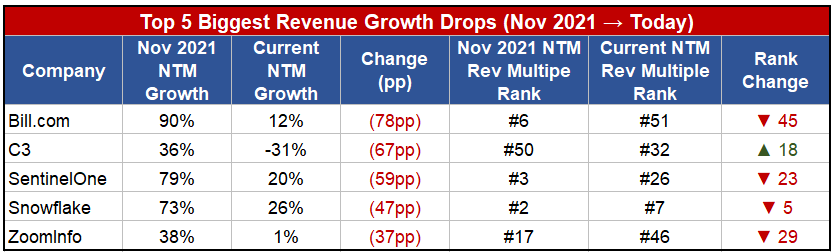

Top 5 Worst Growth Endurance

Let’s look at the companies that had the largest revenue growth rate drops since 2021 (the glory days of SaaS). To measure the impact, I look at the relative “NTM Rev Multiple Rank” change from each period.

For example, Bill.com went from 90% revenue growth in 2021 to just 12% (massive deceleration). So it saw its revenue multiple collapse from the 6th highest to 51st. Investors were clearly expecting Bill.com’s growth to be more durable.

C3, on the other hand, appears to be an outlier. Its revenue growth has gone negative, but it’s relatively more valuable than its peers? C3 actually reinforces the durability point. Whether right or not…some investors are treating C3 as a potential AI winner that will therefore have longer-term durable revenue. So despite short-term growth challenges, some folks believe its long-term durability will be strong.

Many hyper-growth AI companies that are receiving astronomical valuations will see a similar fate. Durability will prove weak, and their valuations will look crazy in retrospect.

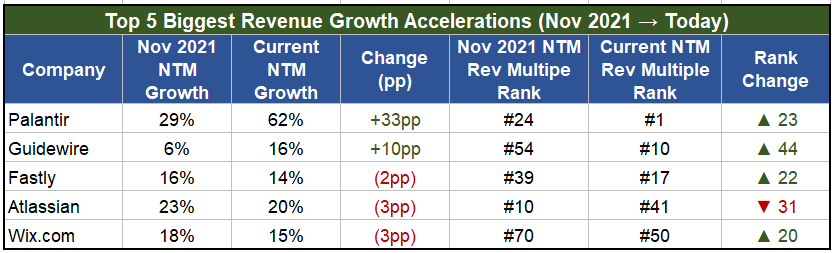

Top 5 Best Growth Endurance

The reverse is obviously true as well.

Palantir is the one seemingly real AI story among public software companies. They are massively accelerating revenue growth at scale. They are signing large, multi-year contracts (more on that below) and investors believe in their durability.

And similar to the C3 story, Atlassian is also an outlier here. Short-term revenue growth hasn’t fallen that much, but investors believe longer-term that AI will destroy revenue durability.

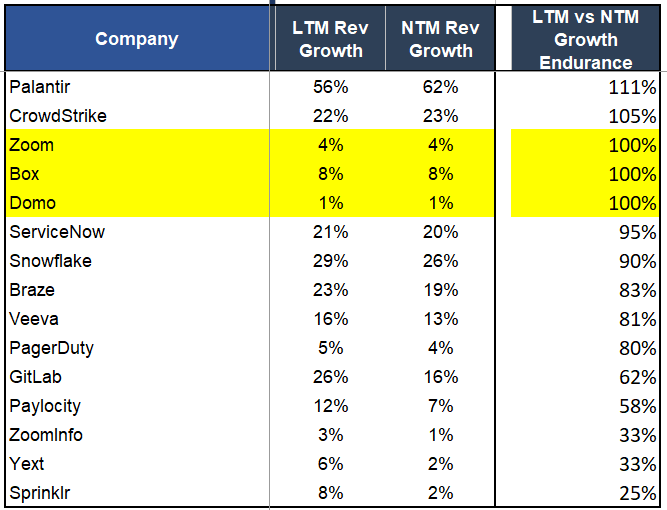

Growth Endurance Needs Context

Below is a sample of public companies and their expected growth endurance over the next twelve months. You might see 100% revenue growth and think, “that’s great!” Well, context obviously matters.

Domo at 100% growth endurance is still lame because it’s based on only 1% revenue growth.

How I Provide Growth Context

Aggregated data can hide growth endurance problems.

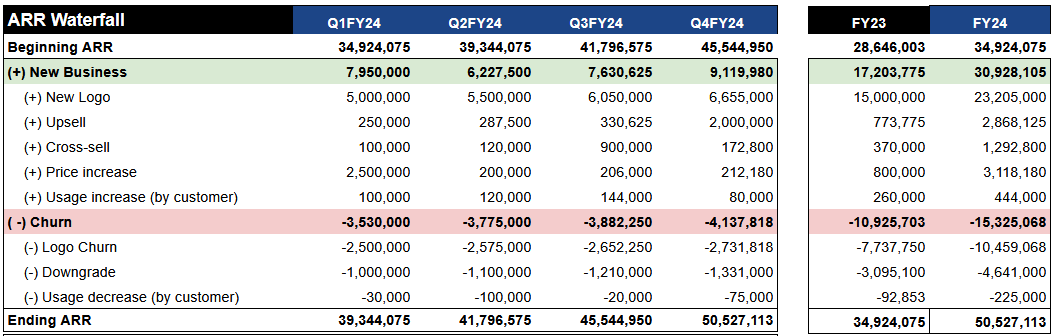

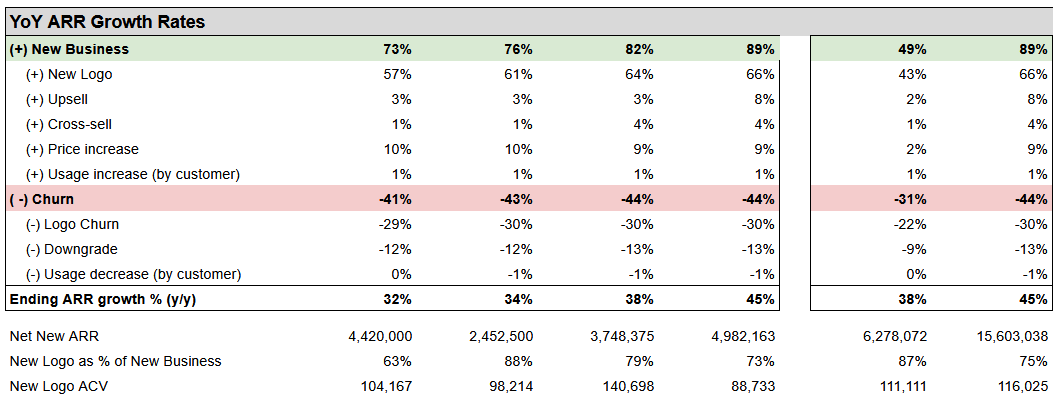

Below is how I break out my ARR waterfall. If you collapse any of these categories, then you lose a lot of relevant information.

I then take it one step further and show the same waterfall in terms of growth rates. This view is critical to spot growth endurance issues that haven’t really shown up in the aggregated data.

Below are a few common things I dive deeper into when I have the right data:

Rapidly increasing expansion vs new logo growth: Are you just milking existing customers? If so, growth rates aren’t sustainable.

New Product Release: Going multi-product is so important in 2026, but it’s REALLY tough to get the same jump in revenue growth after each additional product release. Are you just selling more to existing customers or are you closing new logos as well?

Product M&A: Similar to the above point on new product releases.

Price Increases: Big price increases are almost never durable. Software is becoming hyper-competitive and you think you can raise prices annually by 10%?

Revenue Retention

You can’t have durable revenue without strong customer retention.

What Gokul says below is so true, but also really hard to figure out in practice…so most VCs default to just investing in the highest growth.

Customer retention and net revenue retention are the two fundamental indicators of business quality. I would take a company doing strong growth with excellent net revenue retention over one growing 10x with poor retention. — Gokul Rajaram

My one caveat is that companies should be willing to sacrifice short-term customer retention if it means longer-term revenue growth and customer retention. When does this make sense? An example is when you need to disrupt yourself because of something like…AI. See my prior post (Go Disrupt Yourself)

Final Thoughts

Too many folks are still too complacent about their revenue durability. AI is blowing up durability but it is being temporarily hidden.

It’s almost impossible to truly understand long-term revenue durability based on current finance data. AI is moving too fast and it can change things too quickly.

But my 2 cents:

Having the right data and actually understanding revenue durability are critical to making the right decisions.

Hard financial decisions might need to be made today to ensure long-term revenue durability.

Footnotes:

Check out this billing and collection AI agent. If you want to cut costs (everyone needs to) and collect more cash, then you should have an AI agent in accounts receivable. Paraglide is today’s sponsor.

Reply to this email if you want to sponsor OnlyCFO.

📚 Interesting Things:

Jensen’s Take on Layoffs from AI

For companies with imagination, you will do more with more. For companies where the leadership is just out of ideas, they have nothing else to do. They have no reason to imagine greater than they are. When they have more capability, they don't do more. — Jensen Huang

The bar is raised for every company to build more product surface area. We expect more out of tools today. But also remember that more engineering headcount is good for Nvidia….more shovels are needed.

Fire CFOs Not Using AI?

Your VCs think that if your exec team isn’t using AI then you need new execs. I agree.

But…I’d be even more concerned if the rest of the finance/accounting team wasn’t using AI in Excel…Make sure you have an exec that is pounding the table on AI usage across their teams.

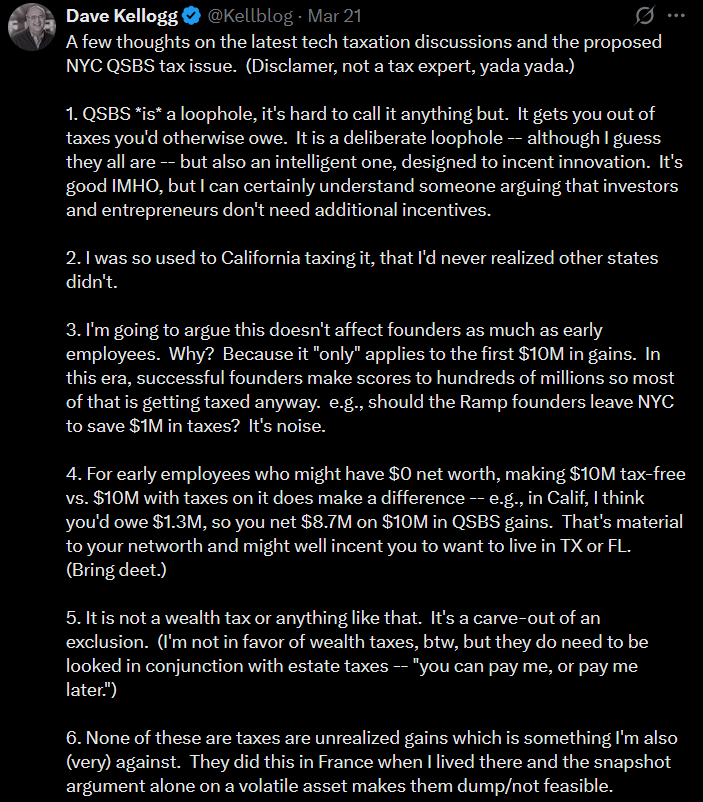

New York Proposes To Eliminate State QSBS Tax Benefit

New York is advancing a proposal to decouple from federal QSBS, which is the tax provision that lets startup founders exclude gains on qualifying exits. It’s can be a fantastic tax benefit.

Dave Kellogg makes some great points. I agree with all of them…

The growth endurance framework is a real improvement over looking at ARR in isolation, and the waterfall breakdown makes the diagnosis much sharper. The natural next step is to go one level deeper and look at what's happening inside the cohorts.

Consider two companies with identical endurance scores. The first is losing its best customers and replacing them with lower-value, shorter-tenure ones. ARR holds, churn looks manageable, everything looks fine from the outside. But each new cohort is worth less than the last. The business is quietly deteriorating while the metrics say otherwise.

The second has weak new logo growth but a core of highly retained, expanding customers that will compound for years. Endurance looks mediocre. The business is actually getting stronger.

Same score. Completely different futures. The aggregate will only tell you so much.