State of GTM

Data/insights from the latest ICONIQ report

Today’s Sponsor: NetSuite

From supply chain shocks to cash shortfalls, today’s business risks can surface fast—and escalate faster. Blind spots, bad data, and aging systems only make things worse.

Download the C-Suite’s Risk Management Checklist —a quick, high-impact guide to help leaders get ahead of 8 critical risks in 2025.

In my last post I discussed revenue growth rate lies of 2025. In summary, there is A LOT of non-durable revenue today that is inflating already low total ARR growth rates.

This matters because many companies have total revenue growth just barely above the minimum bar for unit economics to work. But if those growth rates are inflated with non-durable revenue then growth rates will soon come down even further and the unit economics are going to get even more wrecked.

Companies need:

True (durable) growth to increase

and/or

Efficiency must increase significantly

And ensuring strong unit economics in the GTM function is key.

State of GTM (ICONIQ Report)

Before I dive in…remember that when ICONIQ shows “top quartile” that means top quartile for ICONIQ portfolio companies which are already probably amongst the top quartile of broader VC-backed companies. It’s important to understand the firmographics of the benchmarks you’re using…

Revenue Growth

While most companies are experiencing flat revenue growth, the $25-$100M segment experienced a nice jump in growth. Presumably this is driven by smaller high-growth AI companies that are experiencing a boom in AI sales/adoption in 2025.

It’s the $100M+ ARR companies that have flat/down growth that are likely even worse than they seem due to non-durable revenue growth holding up growth rates.

Total ARR growth matters, but overtime total ARR growth will trend toward new logo growth. So if new business ARR is weak then eventually there will be problems…

Net Dollar Retention

It’s great to see NRR flattening/increasing for most companies, but as I mentioned earlier, higher NRR and lower total growth means….new logo growth is bad.

A strong NRR combined with weak new logo ARR likely means you’re just squeezing more revenue from existing customers — a strategy that can work temporarily to boost growth but will eventually catch up to you.

The other thing that’s a red flag to me is the drop in NRR in the $100M-$200M segment to 101%. This is REALLY bad considering most ICONIQ portfolio companies are enterprise sales. A 9 percentage point drop to just 101% seems to me like a broken (or getting dangerously close to broken) GTM efficiency model.

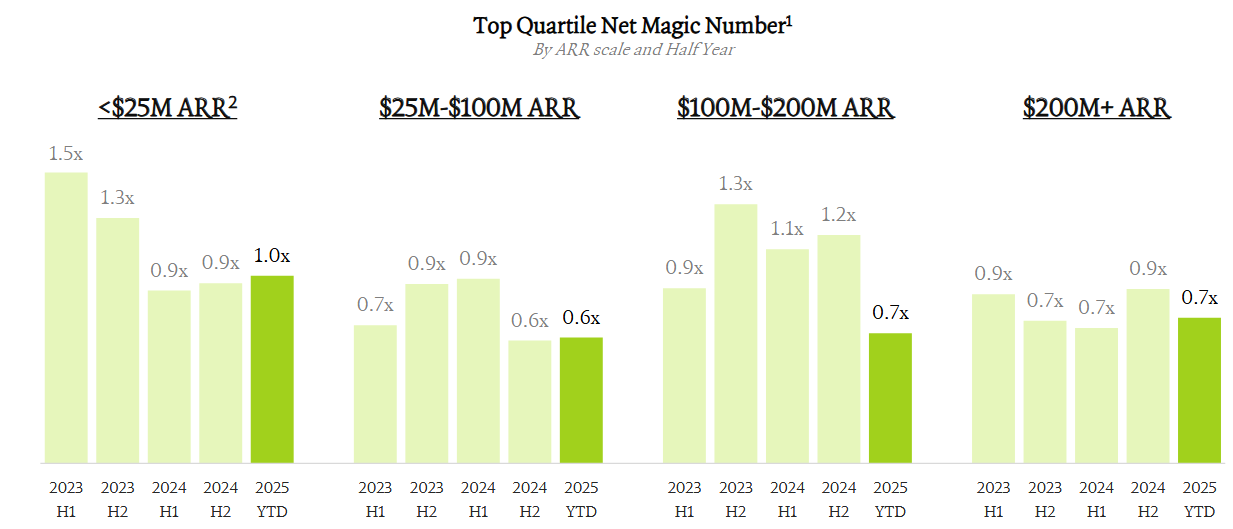

Magic Number

I prefer to look at the CAC ratio, but ICONIQ presents the inverse of that (the “magic number”), which means the higher the better.

Magic Number: current quarter net new ARR / prior quarter S&M

The $100M-$200M segment had a HUGE drop in magic number. This is likely driven by the plummeting NRR in that segment combined with spending too much in S&M while not hitting sales targets.

Quota Attainment

Attainment seems to be trending relatively flat with last year.

Remember that as attainment goes lower, then your sales efficiency plummets because you are paying reps a base salary to close a lot less deals. All else equal, attainment in the ~80% attainment range is ideal — enough are hitting but it isn’t too easy.

Headcount

Interesting HC benchmarks that breaks out high-growth and AI-native companies. The data kind of makes sense intuitively based on product, pricing and GTM motion differences in these breakouts.

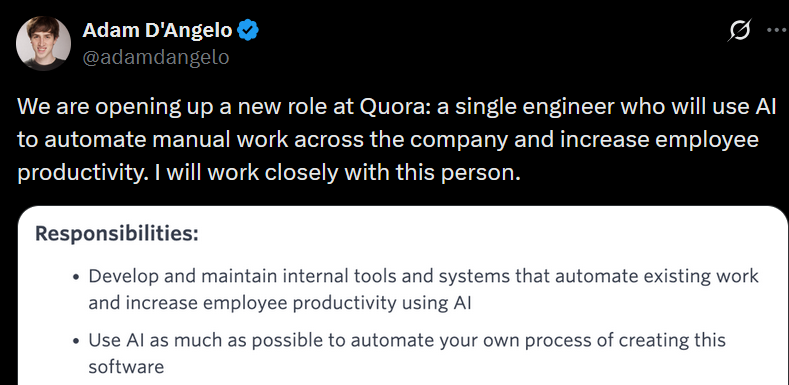

Side note, I strongly believe what Quora recently announced is the right way to push AI adoption — hire someone dedicated to finding AI use-cases across the business and helping departments adopt it. You need a department/person driving the adoption.

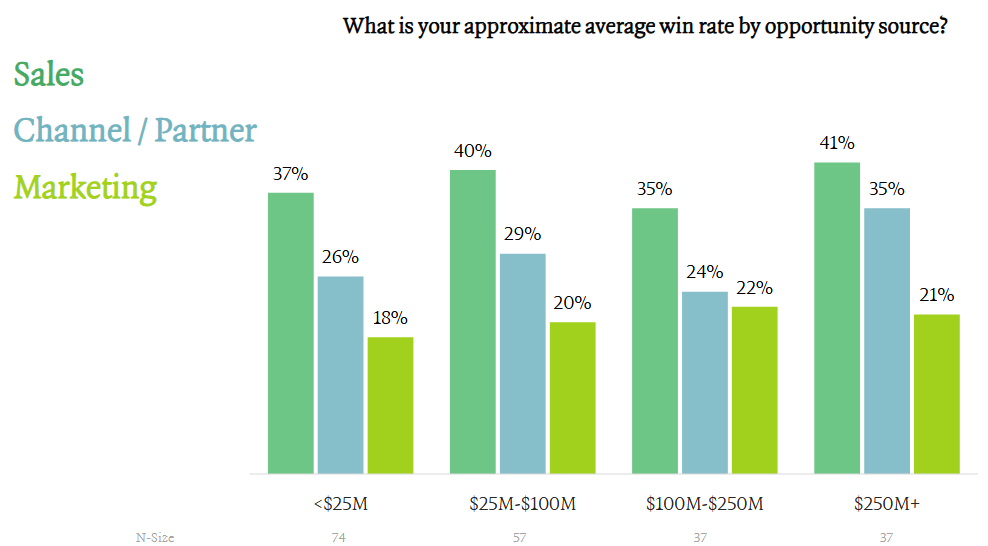

Conversion

The data below on conversion between AI-native and non-AI-native companies is really interesting. Seems like all AI-native companies should be offering a free trial…

My only commentary here is to make sure you are segmenting your pipe gen sources. The conversion, cost, etc can be significantly different between them.

Pricing

A hybrid pricing model takes the lead in popularity. And based on another pricing report I recently read, companies with a hybrid pricing model are more efficient in GTM than their peers.

Bonus Slide from Goldman Sachs

The below shows key metrics (growth and profitability) by sector and YoY so you can see which sectors had the most durable growth.

Not all software is the same in its ability to grow in the age of AI. And there can be significant profitability differences as well.

Final Thoughts

Don’t neglect GTM efficiency.

I think some are ignoring (or blissfully unaware) that their unit economics are starting to break but haven’t seen that reflect in their blended efficiency metrics and overall cash burn.

Free cash flow can temporarily improve as unit economics deteriorate….but it eventually catches up. Pay attention to the GTM efficiency leading indicators.

Footnotes:

Download the C-Suite’s Risk Management Checklist (from NetSuite)

Subscribe to CFOPilot to get the latest benchmarks and easily find them all.

Get 20% off with OnlyExperts to find offshore accounting resources

N is only 6 on that 101% NDR but yea wow that is shocking

Good post. At the end when you say don’t forget GTM efficiency, how do you plan to do that without an in depth knowledge of GTM effectiveness and materiality. How do you know what to cut / remove from GTM spend? This is where understanding the network of causes and effects really matters.