Thoma Bravo's $5B Medallia Loss | The PE Reckoning is Coming...

Inside how Medallia broke and what it means for the rest of software

Brought to you by…Deel

I’ve seen companies roll out new global comp strategies that drove employees to quit. It felt unfair, was poorly rolled out, or was just a bad comp strategy. It’s hard to get right.

What pay model to use? Anchor city-based, single global payscale, localized, etc

How do we balance retaining top talent while also becoming more efficient?

How do we do equity comp across jurisdictions?

Compliance considerations? Local HR laws, mandatory bonuses, statutory benefits, overtime, etc

Check out Deel’s guide for a breakdown of key decisions when creating your global comp strategy.

Private Equity is in Trouble…

We are going to witness a spectacular collapse of many large PE-backed companies over the next couple of years. And the entire tech industry is going to suffer (not just PE-backed companies).

There are two primary stakeholders in a PE leveraged buyout (LBO):

Private credit lenders (Blackstone, KKR, Golub, Apollo, etc)

Private equity firms (Thoma Bravo, Vista, etc)

Lenders are always first in line to get paid and then anything remaining (if any) goes to the PE investors (and any employees with equity).

Many PE-backed software companies have debt coming due over the next couple of years. When that happens, they (and other companies that took debt) have the following options:

Repay loan: lol…these companies don’t have the cash for that

Refinance: unlikely for most given the conditions today

“Amend & extend” (A&E): kick the can down the road with existing lenders

Sell the company: not happening right now at valuations that make sense for most of the deals that were done during ZIRP.

Lender takes the keys: PE equity gets wiped and lenders’ debt is at least partially swapped for equity

“Amend & extend” is the classic playbook, but at a certain point it becomes borderline irresponsible for lenders to keep doing it. Blackstone (largest holder of Medallia debt) refused to “amend & extend” in late 2025 so the PIK toggle expired. And this pushed Thoma Bravo to hand over the keys…

Lenders Take The Keys to Medallia

Medallia is the largest software PE-backed deal to fail to the point where lenders take the keys. But, unfortunately, more of this is coming…

Medallia was taken private at a $6.4B valuation in 2021 (peak of software valuations) by Thoma Bravo at a 9x NTM revenue multiple.

Lenders: provided $1.8B of debt at acquisition

Equity: Thoma Bravo and co-investors put in $5B

Thoma Bravo’s $5B stake is now worth zero. Gone. They just handed the keys to the lenders and are walking away. The lenders took control of the company and swapped debt for Medallia equity.

No lender wants to “take the keys” to a company. It’s a last resort. They don’t want to manage companies, but at a certain point it may be the best option left.

The Private Credit Warning Signs

There has been a lot of discussion about private credit over the last couple of months, driven by their large exposure to the deteriorating software industry, which has created an investor redemption problem (large number of investors requesting to withdraw their money) while software loans continue to get marked down.

Once deemed the perfect LBO candidate, software debt is clearly struggling a lot more than every other industry (it’s a casualty of AI).

But folks are realizing that not all software is created equal. Certain software segments are more durable in the age of AI than others. The least impacted? Vertical software...there are riches in the niches!

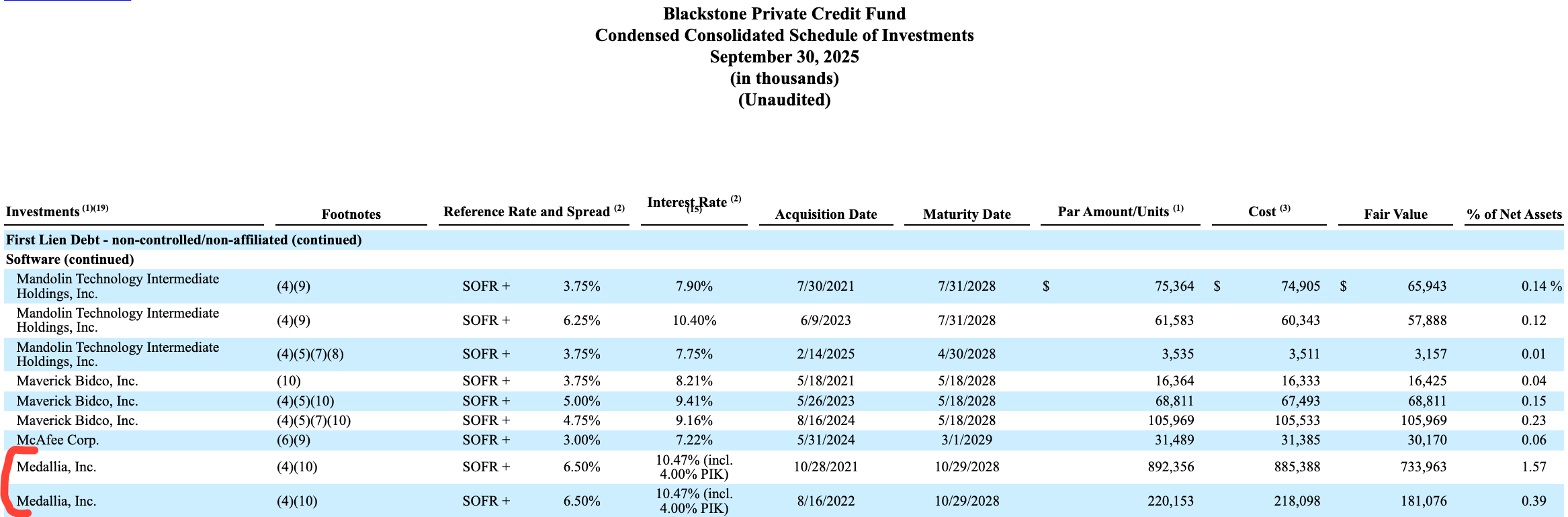

How are these loans valued?

There is no real market price discovery in private credit because the loans are privately held and not frequently traded. 3rd-party valuation firms are used to determine loan prices and then that is approved by the investment committee each quarter. Obviously lenders don’t want to adjust prices downward until absolutely necessary. Often these loans will look totally fine until they just explode (see Medallia’s loan marks below).

Because each lender has a different 3rd party doing the valuations, the marks on the same loan can be quite a bit different across lenders.

Are loans’ fair values publicly disclosed?

A lot of PE-backed private company debt is held by lenders that are required by the SEC to report details of all their investments, which includes details about the interest rates and current fair value of the assets.

Often at least some of a company’s debt is held by lenders that are not required to publicly disclose their holdings so the public filings won’t tell you the exact amount of total company debt.

If your company has debt you can check to see if it is held by any lenders that are required to publicly disclose it. Just go to EDGAR’s full text search and search your company’s name.

What do the marks mean?

How many cents on the dollar are going to get repaid?

Below is a rough guideline of how I think about these GAAP marks. Remember, if the loans are materially impaired then the PE firm’s holding is likely zero since they only get paid after the debt gets paid.

>$0.98 (excellent status): This is just the original issue discount that gets accreted back to income for GAAP purposes.

$0.95 - $0.98 (early stress): Valuation model applies larger discount rate because the asset is riskier. Still expect full principal but pricing in higher risk now.

$0.85 - $0.95 (restructure likely): Now there is a material chance of principal loss.

$0.75 - $0.85 (restructuring soon): Priced now as a distressed asset that won’t cover principal.

<$0.75 (deep distress): “Taking the keys” becomes likely and “non-accrual” status gets triggered. Non-accrual means the lender must stop recognizing interest income because it is unlikely to be collected.

Note - just because a loan hasn’t been impaired does not mean the company isn’t in trouble. Medallia has clearly been a loser for Thoma Bravo for several years (while the loan fair value was still at par). Lenders just thought they could at least get their money back.

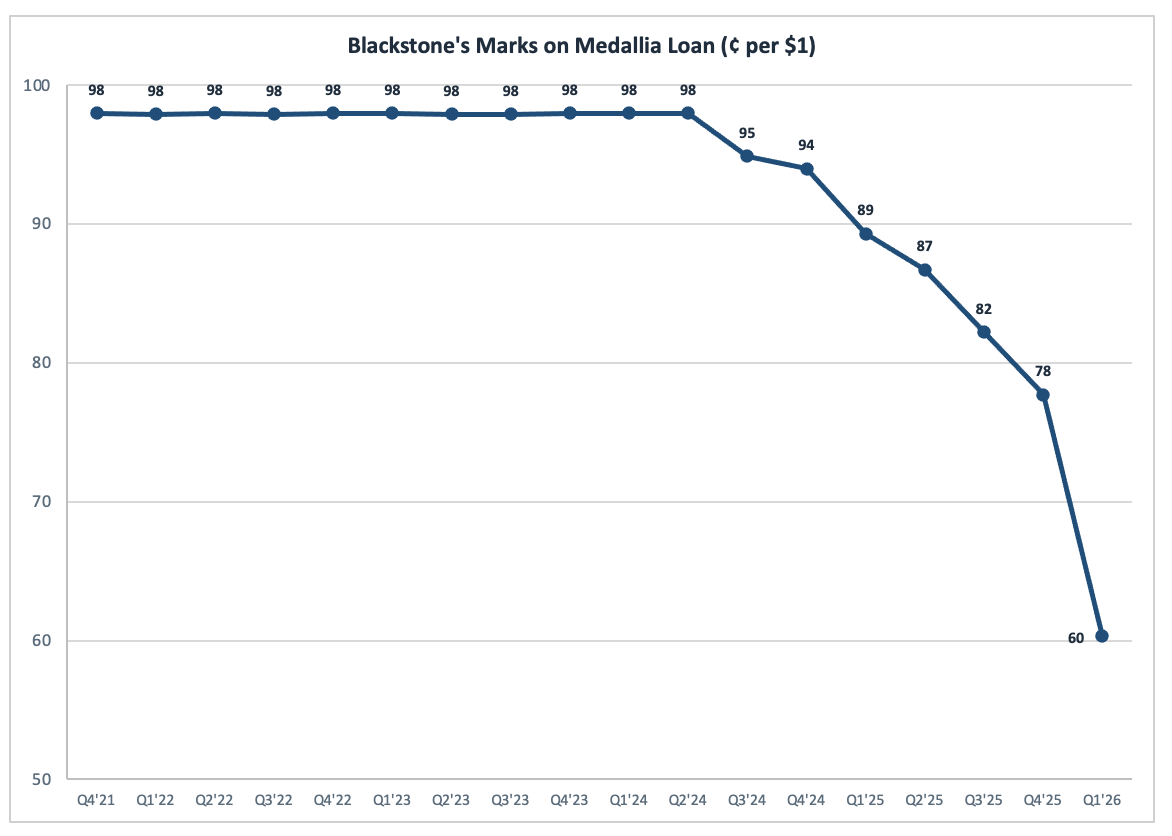

Medallia’s Loan Prices

Medallia debt was in “excellent” condition (basically par) for 3 years and then sharply fell to distressed in just a few quarters…

What Happened to Medallia?

There are two ways lenders get their money back:

Company profits: uses FCF to pay interest and principal

Exit or fundraising event: proceeds pay debt down first

Drowning in Debt

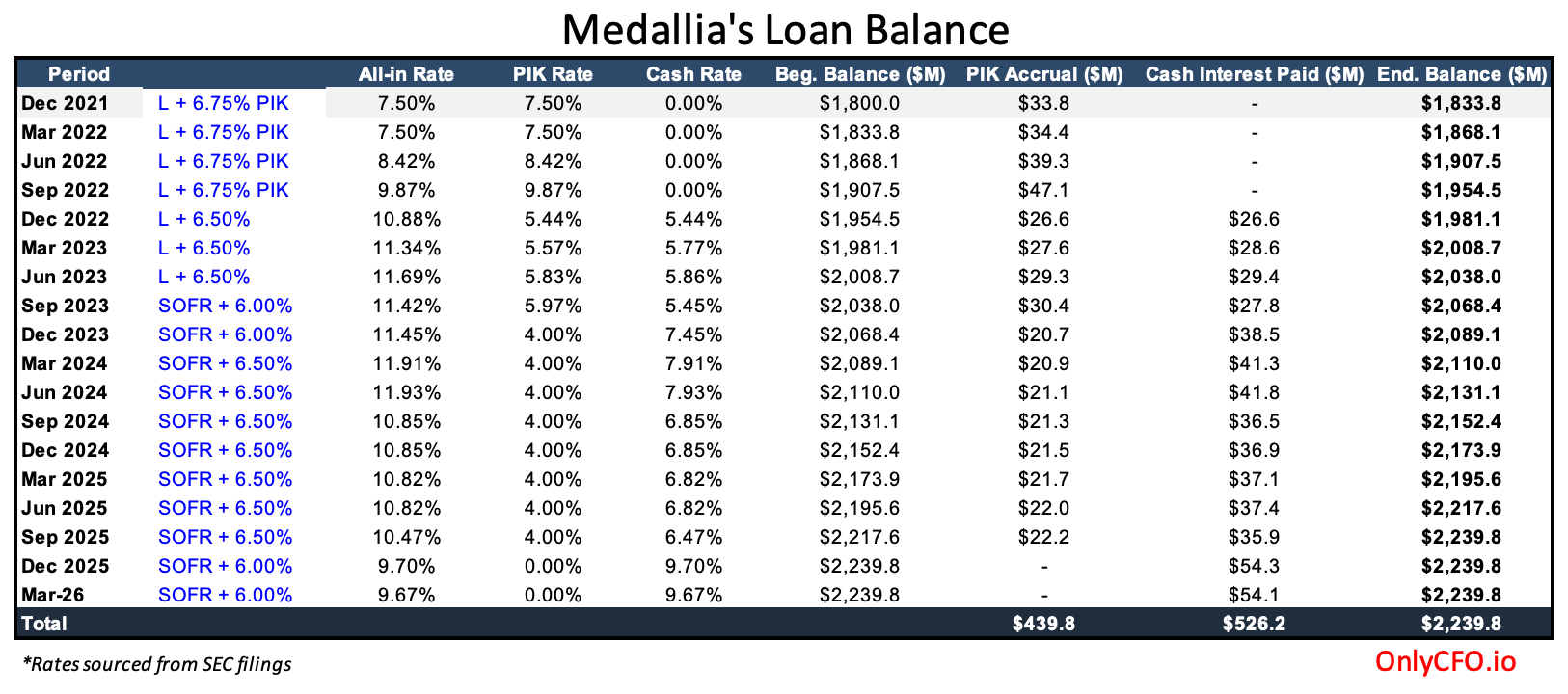

Medallia had one of the lowest FCF margins relative to their growth when they were acquired (bottom decile Rule of 40 score). Thoma Bravo assumed strong growth rates would continue while they turned the company to 25%+ FCF margins.

The LBO loan was underwritten based on Medallia’s ARR (not traditional cash flow metrics). Medallia was burning cash when acquired so the first year of the loan was 100% PIK. Instead of paying interest in cash, PIK allows the company to just add the interest to the loan balance.

Two things with Medallia’s debt made their problem much worse.

LIBOR/SOFR: The cost of variable debt increased significantly. The variable portion rose from ~0.75% in 2021 (good old ZIRP days) to a peak of 5.4% in late 2023 and is now 3.7%. That’s a material increase.

PIK: Medallia went from not having to pay any cash interest to eventually having to pay 100%. 100% PIK for 1 year → 50% PIK for 1 year → ~35% PIK for 2 years → 0% PIK

Below is what Medallia’s debt waterfall likely looks like based on the original $1.8B. The PIK over the last several years took the balance from $1.8B to $2.2B.

Medallia reportedly has ~$2.8B of debt today. The increase likely came from additional loan draws to fund acquisitions that Medallia performed since Thoma Bravo took it private.

Medallia Debt and Interest: Annual interest on the loan went from ~$135M to ~$300M as the loan balance grew from $1.8B to ~$3B and interest rates increased. On top of that, interest payments slowly went to all cash.

Medallia Profitability: They are reportedly only generating $200M/year in EBITDA.

$200M EBITDA with $300M of interest is broken…

Overpaid, Sinking Valuations, and No Exits

Back in the glory days of 2021, a 9x revenue multiple seemed relatively cheap. The overall median when Medallia was acquired was 36x (!!) and the median for mid-growth (where Medallia sat) was 15x.

PE usually gets liquidity the same way as everyone else: M&A (PE or strategic) or IPO. The typical playbook is PE buys at a good price, they cut costs to drive profitability, and hopefully maintain decent growth rates. Then they can sell in 3-5 years for a higher multiple. And that playbook worked for a long time.

IPO: not happening for anyone other than high-growth companies.

M&A: Mostly frozen for larger software deals.

Most folks don’t realize how important PE has been for software company exits…If PE deals slow down then it’s going to impact the entire sector. Multiples continue to fall.

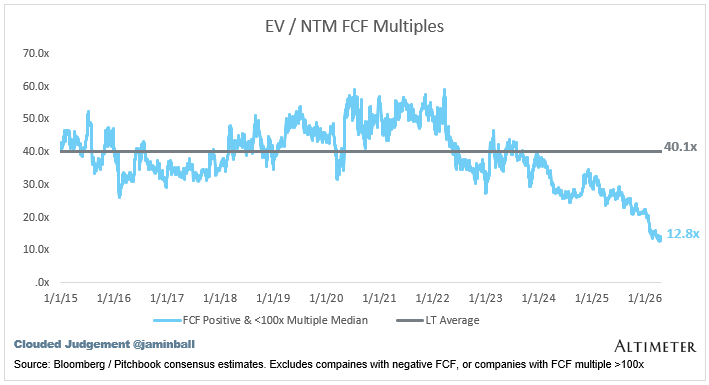

FCF multiples for software have never been lower…

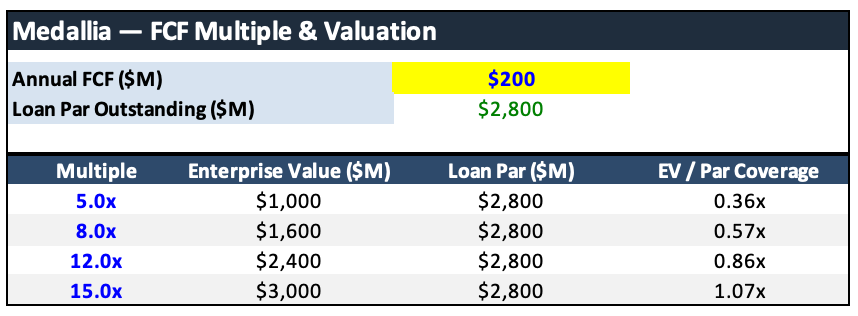

So if we look at Medallia and assume $200M FCF and apply a reasonable FCF multiple based on the market today, you get an enterprise value that in a best-case scenario will barely cover the current loan balance.

Orlando Bravo recently said the following in a CNBC interview about the Medallia acquisition price:

When we bought it, we way overestimated or extrapolated the very high rate of growth of that company into the future. We made a mistake. And that cost us to pay too much.

Are Leveraged Companies Cooked?

Many software companies that took on debt (particularly PE-backed) will follow the fate of Medallia over the next couple of years.

Their debt will create a death spiral that is nearly impossible to escape. Revenue growth has fallen off a cliff, pricing pressure is rising, and AI is disrupting their business. If you are running the business for cash (which they have to in order to pay increasing interest rates) then it will be really hard to innovate in the age of AI.

If you don’t innovate with AI, then your terminal value is definitely going to zero and eventually your profit margins will too. And you are worth less than your debt.

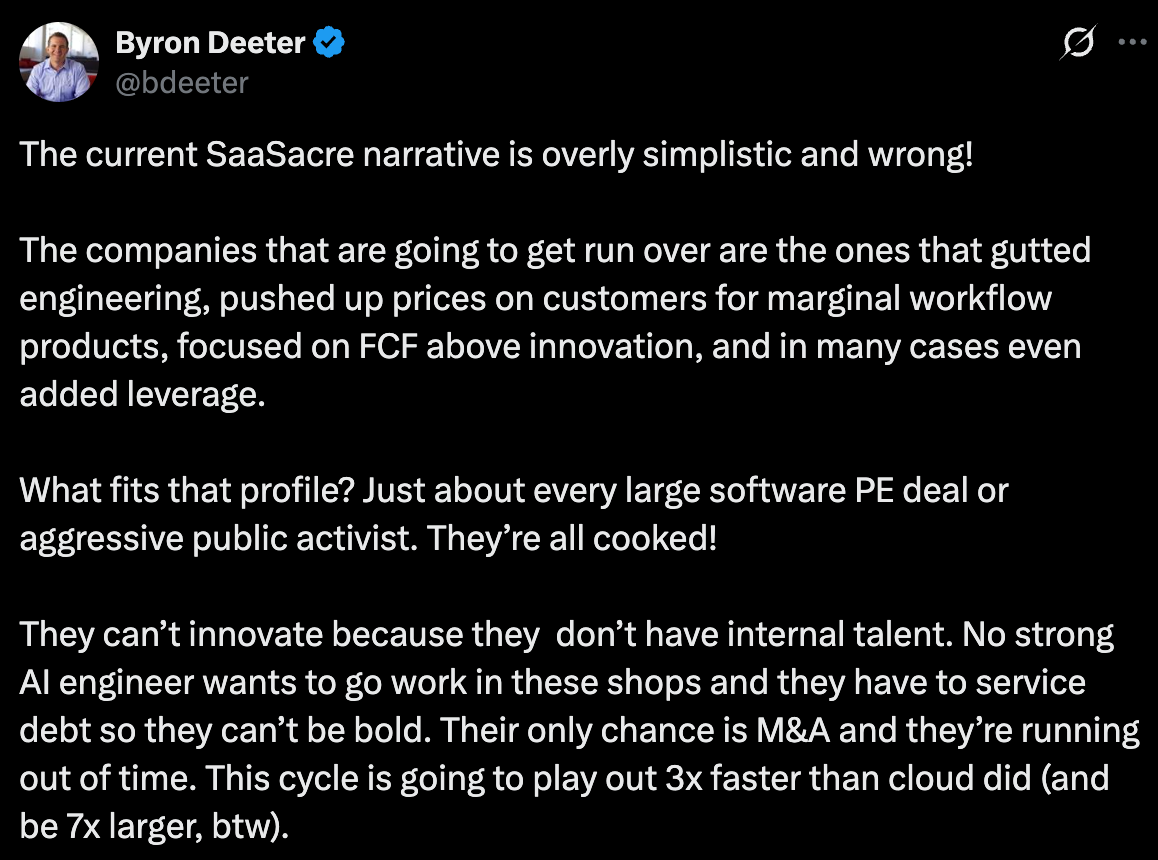

Byron (one of the best software VCs) agrees…

Final Thoughts

The overall theme of 2026: accelerate or die.

But it is MUCH harder to accelerate/innovate when you have a heavy debt burden. This is why most PE-backed companies are in trouble.

For CFOs at companies with debt…talk to your lenders sooner rather than later. It’s going to get harder over the next two years to extend or refinance.

With wishes of “amend and extends” for all,

OnlyCFO 🫡

Footnotes:

Check out this compensation guide for managing a global company. Deel has some of the best data and resources out there.

Want to sponsor? Email onlycfo@onlycfo.io

Taking the keys here feels like it could lead to a pretty good outcome for blackstone if they continue to find cost synergies and get an exit at 10x NTM FCF in 2-3 years assuming there is ANY stability in medallia revenue (which is a big TBD)

A friend pointed me to this crazy comeuppance in PE and it really shocked me, especially when you consider who ends up holding the bag. I wrote a blog post about it as a cautionary tale and explainer.

https://www.linkedin.com/pulse/breaking-thoma-bravo-handing-medallia-back-its-ken-pulverman-kdasc/?trackingId=zWTkkXLReZVlieNvIw6EYQ%3D%3D