Reading Income Statements

What you must know about finance and accounting for software companies

Both operators and investors must understand the basics of financial statements. If a company leader doesn’t understand how to read and interpret financial statements then they won’t be very good and probably won’t last very long…

It may not be sexy, but accounting is the language of business. To be successful you must learn it.

Today’s Sponsor: NetSuite

CFO's Ultimate KPI Checklist: 50 Step-By-Step Checklists to Drive Your Company's Success

Maximize your business’s success by measuring the right KPIs. Get clarity on which metrics should represent your company’s needs and goals HERE.

Understanding Financial Statements

There are three primary financial statements:

Income Statement

Balance Sheet

Statement of Cash Flows

The point of this post is to be a shareable piece of content to help investors and employees better understand accounting and finance. The focus of this post is the Income Statement (aka P&L, Statement of Operations, etc)

If you are an experienced finance/accounting professional then you should know most of this stuff. BUT….the rest of your company and less experienced investors probably does not.

If everyone understands accounting basics, then all employees (and investors) will make better decisions. Make this required reading at your company 😎

Income Statement

The income statement is a window into the performance of a company over a specific period of time by reporting on a company’s revenue and expenses.

The period of time included on income statement snapshot is almost always one year or less (typically annual, quarterly, monthly, or year-to-date). Each of those individual snapshots is reviewed with historical comparative periods for context — if you are reviewing quarterly income statement then you may want to look at the previous quarter and the one year ago quarter for context.

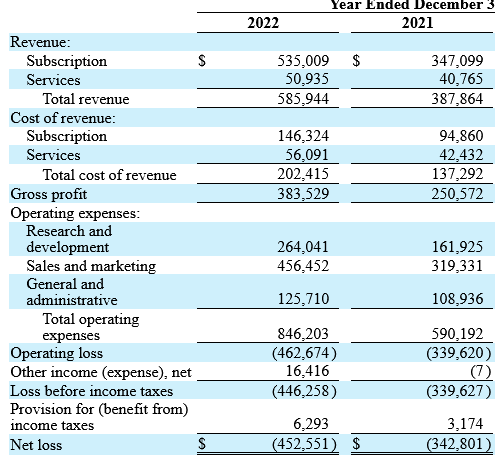

Below is a typical looking software income statement. I will breakdown each of these sections and what everyone should understand in the rest of this post.

1. Revenue

Cloud companies often have two primary categories of revenue:

Cloud revenue

Seat-based

Usage-based

Flat fee

Professional services & other

Implementation services

Advisory services

Managed services (some will include this in a recurring revenue line tho…)

When professional services revenue is immaterial, then many companies will just show one line called “revenue” on their financials. However, for internal management reporting all major revenue categories should be broken out so each revenue type can be reviewed separately.

What is “revenue”?

Revenue reported on financials is known as “GAAP” (generally accepted accounting principles) revenue.

GAAP Revenue: revenue is recognized as the services are delivered

For seat-based for flat fee contracts this usually means revenue is recognized evenly over the contract term.

For professional services and usage-based revenue, revenue recognition is typically recorded as delivered/used so there can be more variability in revenue each period.

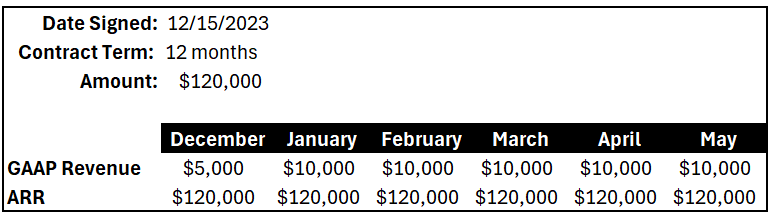

Revenue reported on financials is a lagging metric compared to other metrics like ARR (annual recurring revenue). ARR is a point in time total recurring revenue metric while revenue represents the amount recognized for the period being reviewed.

Example:

If a company closes a $120K software deal on 12/15/2023 then they would show $120K new ARR starting on that day. But they would only show revenue of $5K. Formula: $120K / 12 months = $10k per month and only halve of December should be recognized as revenue.

There are a lot of “revenue” numbers people may refer to, but revenue on the financials should ALWAYS be GAAP revenue. Make sure you know what people are referring to when they talk about revenue!

2. Cost of Revenue (aka COGS)

Cost of revenue should be broken out the same way that revenue is broken out:

Cost of revenue - cloud

Cost of revenue - professional services and other

And similar to revenue, if you have multiple types of revenue underneath each of the above (e.g. usage-based) then you should break that out at least for internal purposes/tracking.

Cost of Revenue - Cloud

The major categories that are included here are:

Customer hosting costs - AWS, GCP, Azure

Support team - responding to customer support tickets

Dev Ops - people ensuring uptime and reliability of customer accounts

Customer success management (maybe) - see my prior post on how to categorize

Software and other costs for the teams above

Cost of Revenue - Professional Services & Other

Professional services COGS is pretty straightforward:

People costs for delivering the services

Software and other people-related costs to deliver the services

Costs of any other revenue generated

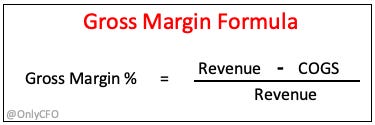

3. Gross Margins

Gross margins tell you how much (either as a $ or % of revenue) profit you have after subtracting COGS from revenue. Viewing gross margin as a percentage of revenue is generally more useful because then it is comparable to other companies.

COGS is a *very* protected expense category because software company valuations can be highly correlated with gross margins.

The reason investors care so much about gross margins is because COGS grow very linearly with revenue while operating expenses are not variable and *should* have a lot more leverage at scale (see below on what operating expenses are). Gross margin is the incremental cost of delivering more of the software solution.

Example: A company with 75% gross margins may only be able to improve gross margins to 78% after doubling revenue because of more efficiencies at scale, but it can cut its operating expenses by 30% over the same period of time. This is because COGS (and related gross margins) are direct costs of delivering the cloud solution that move in line with each additional dollar of revenue.

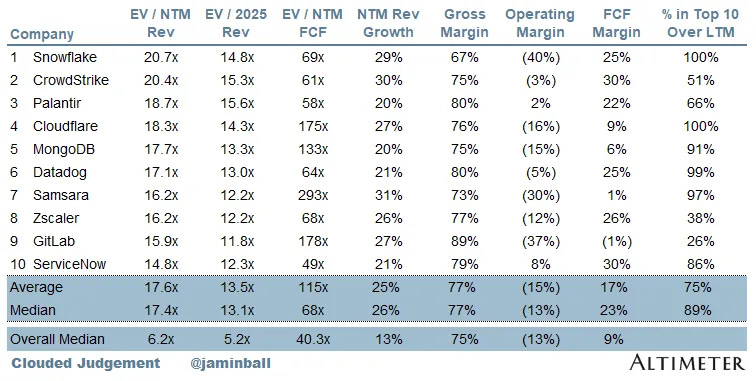

Caveat: A lot of software companies haven’t proven they can really get leverage out of operating expenses at scale. This is evident by the many software companies continuing to lose many even though revenue growth has slowed dramatically. The good ones though can be extremely profitable as evident by their 25%+ free cash flow margins.

Gross Margins by Revenue Type

A big reason to separate out revenue and COGS for each type of revenue is to better understand the gross margin profile for each revenue type.

True cloud revenue should have really high gross margins. The top 10 cloud companies with the highest valuation premiums have an average gross margin of 77%. Lower gross margin companies will have a lower valuation premium all else being equal.

When there is hardware, professional services, or other non-software revenue included then gross margins will be a lot lower.

A lot of companies run their professional services part of the business at breakeven (or even a loss) because they rely on the software revenue to generate all the profits and the professional services is just there to help sell more software.

4. Operating Expenses (aka “OpEx”)

The operating expense section of a software company’s income statement almost always has the following categories:

Sales and marketing (S&M)

Research and development (R&D)

General & administrative (G&A)

For internal purposes these categories are often further broken up, but for external financial reporting these are typically the categories.

What is included in each category?

Sales and marketing (S&M)

Sales team payroll (AE, SDR, SEs, sales management, etc)

Marketing payroll (demand gen, PR, events, comms, etc)

Customer success payroll (see COGS section on debate between COGS and S&M)

Rev ops and sales enablement

Software and other non-headcount costs for these teams

Trial hosting costs (such as AWS)

Research and development (R&D)

Engineering, product, and design team payroll-related costs

Software and other non-headcount costs for these teams

Dev infrastructure costs (such as AWS)

Note - a lot of earlier-stage companies don’t properly break these costs out properly between COGS, R&D, and S&M

Quality assurance (QA)

General & administrative (G&A)

Finance, legal, HR, and other executive payroll-related costs

Corporate insurance

Financial audits

Charitable contributions

5. Other OpEx Items

Allocated Departments

There are certain expenses and teams that are generally allocated across all of the above expense groups (COGS, R&D, S&M, and G&A) based on relative headcount or some other reasonable allocation methodology.

IT - people and software the entire company uses

Recruiting - internal recruiting resources (sometimes put into G&A though)

General - Facilities, company offsites, etc

Understand how they are coded versus other companies so proper comparisons can be made.

Stock-Based Compensation (SBC)

Most people don’t really know how to think about SBC’s impact, especially in the private markets. Check out my previous post for a SBC deep dive. The short version of is that SBC is a real expense and should NOT be ignored…

Here are the basics that you should know about SBC:

SBC represents all equity-based awards (e.g. stock options, RSUs, etc) that are given to employees, consultants, advisors, etc.

Accounting rules require companies to record an expense on the income statement that represents the fair value of these equity-based awards. The expense is recognized on the income statement over the period the award is earned (typically over 4 years).

SBC expense is a non-cash expense because the company doesn’t pay cash when issuing the award. The real impact is that there is more dilution to shareholders because more awards are issued….this is why it should not be ignored.

Sales Commissions

The majority of sales commissions for software companies do not get expensed on the income statement when earned, rather accounting rules require that they get expensed over several years. Most SaaS companies expense sales commissions over 3 - 5 years.

Example: A sales rep closed a deal on 12/15/2023 and earned a $12K commission that was paid on the day the deal closed. Even though there was a $12K cash payment to the sales rep in December, only $333 (1/36th of the commission) is expensed on the income statement. That same amount will be expensed over the next 3 years.

Pay attention to this as you try to understand the unit economics of the business because it will screw up your SaaS metric calculations unless you unwind it. I always add the full amount of commissions earned (rather than expense) to metric calculations.

6. Other income (expense)

Interest expense and income

Foreign exchange gains and losses

Investment gains and losses

7. Income Tax Expense

Eventually software companies have to become profitable, but even before that point they might have to deal with income taxes:

Foreign entities: If a company has set up foreign entities, then income taxes might be owed in these foreign jurisdictions even if the consolidated company isn’t profitable.

Financial net income doesn’t equal taxable income: Tax net income may be difference than financial net income

Change in tax laws for research and development expenses. Check out my previous article on the new tax rule Section 174 that may cause many software companies to pay more in income taxes. This is in process (at least partially) of being repealed, but if you have a lot of international R&D then you might still be in trouble.

Concluding Thoughts

All investors and business operators should understand the basics of an income statement. If you don’t understand an income statement then mistakes will be made in allocating capital and making investment decisions.

For company operators, make sure your entire company understands the basics of finance and reading financials. It will make them better decision makers and your company will be better for it.

Footnotes:

Sponsor OnlyCFO Newsletter and reach 16k+ CFOs, CEO, and other leaders in the software industry.

CFO's Ultimate KPI Checklist: Check out this great checklist of KPIs that companies and CFO’s should be tracking

Subscribe if you haven’t and share my newsletter with your friends!

Super simple to follow. Thanks for creating a shareable "how to read a P&L" guide. The industry benchmarks you added help put things in perspective too! :)