Down Rounds Won’t Kill You

CEOs got 99 problems but a down round shouldn't be one

*Welcome to the 670 new subscribers since last week. Please like and share this post if you find it interesting.

CEOs have plenty of problems (at least 99…) that can kill their company, but a potential “down round” in valuation should not be one of them. For those who don’t know, the below image is of Stripe CEO who took a massive down round on Stripe’s valuation earlier this year - $95B → $50B.

Down Round: when a company raises a financing round and the pre-money valuation of the company is lower than the post-money valuation of the previous round.

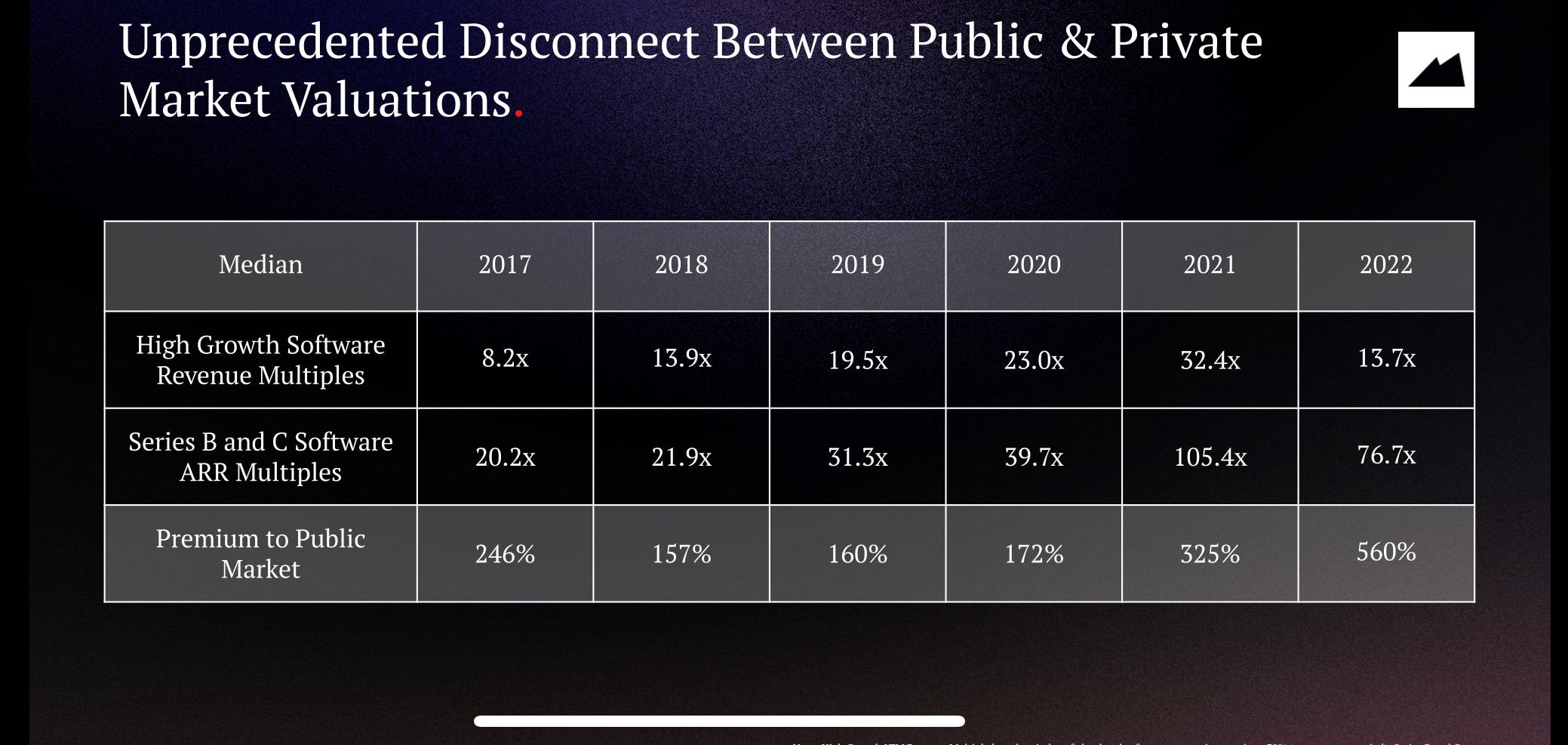

At this point, we all know that valuation multiples have come WAY down - the average top 10 public companies were valued at 60x revenue in 2021 and have sunk to ~10x today.

Private company valuations are even more extreme with 100x - 300x revenue valuations at $1B+ being somewhat common in 2021. The problem with private companies is there isn’t continual price discovery/adjustments as the market changes. While a lot of private company CEOs know valuations are down, many are still too optimistic about what their valuation would be today if they had to raise.

Accepting the new reality is tough, but how companies press forward may determine the fate of their company.

Quick side note: A lot of costly mistakes can be avoided if companies have someone with financial expertise helping them navigate this stuff.

Email me at onlyrealcfo@gmail.com

You need bookkeepers and CFO services from someone who actually understands the software industry.

Back to the topic of down rounds…

Death by Unrealistic Growth Plans

A lot of companies are going to fall into this category. CEOs and investors have pushed their companies that they need to “grow into their prior valuation”.

That’s great if you can pull it off before the next fundraising is needed but should a valuation number be the guiding North Star goal?

Valuations and headcount were the vanity metrics of 2021 that got companies in trouble in the first place. Companies should rather focus on things within their control - efficient, durable, and strong revenue growth. Trying to grow into a valuation number is aiming for a moving target.

Companies are blindly forcing a financial plan that would theoretically allow them to grow into their valuation before they have to fundraise again. In theory, that is great….but more often than not, the plan is unrealistic. Growth will be slower and cash burn will either be the same or higher (which will destroy efficiency metrics).

The below quote is very accurate. Companies are building financial models to back into what must be done to get back to their prior valuation. The problem is that there are so many lies in the model’s assumptions that the plan will be nearly impossible to hit.

A great deal more fiction is written in Microsoft Excel than in Microsoft Word

Example: When revenue growth plans are too optimistic

The hypothetical company below raised $100M at a $1B valuation (or 200x of its $5M ARR). Given where multiples are today, they need to grow pretty fast and show efficiency to “grow into their valuation”.

If they hit their plan perfectly, then sometime between 2025 and 2026 they might get a $1B valuation! Just a few potential problems:

They will likely need to raise in 2025 (not when they have zero cash in 2026) so they still probably need to take a down round.

Even if they can wait and get a $1B “flat round” it’s not neutral for existing shareholders and employees because there will be additional dilution from raising another round.

Everything won’t go perfectly. This plan assumes perfection and that growth will be amazing. Not only is high-growth *really* hard, but the macro-environment is much tougher today and a lot of founder/CEOs haven’t fully grasped that reality.

The more likely scenario below shows what can happen to companies that plan for amazing growth, but fall short:

Slower than expected growth, which will cause lower valuation multiples

The dollar cash burn remains high because they keep pushing for a plan to grow into their valuation, but efficiency metrics are now terrible because the $ burn is the same while revenue growth is a lot less than planned.

They have to raise money on a much smaller ARR, slower growth, and less efficiency. This can be incredibly destructive to valuations. I put a 7x valuation multiple here to illustrate the point, but the difference between these scenarios is likely even greater.

Don’t build a financial plan based on hopes and dreams of returning to your previously glorious valuation. Ignore that valuation.

Build a financial plan based on data and leading indicators of success. You don’t want to leave growth opportunities on the table, but you also can’t grow at all costs because that can kill you faster than anything - especially if you have all the costs but only some of the growth.

Death by Cost Cutting

Becoming incredibly efficient is not a strategy for winning. For VC-backed companies, it is a recipe for creating a zombie company that your VCs no longer care about because the exit outcome doesn’t move the needle for their funds.

Yes, most software companies need to improve efficiency, but without growth then those companies may still die - it’s just a long drawn-out death. Or they will never grow past the preferred stock liquidation preferences and employees’ equity will never be worth anything.

Example: Cost cutting your way into irrelevance

The same company as earlier, but in this scenarios they aim to be highly efficient so they can control their own destiny and become cash flow positive. The problem is that this usually no longer looks interesting as a VC outcome.

It’s one thing to not optimize for a valuation number, but if a company is growing so slowly that it will *never* be a meaningful exit then most folks stop caring. The preferred stock liquidition preference is too large.

Also, given the amount of money they raised at the high valuation, if there ever is an exit, the preferred stock liquidation preferences will eat away almost all of the returns. There aren’t really any winners.

Concluding Thoughts

Stop focusing on how to get back to your prior valuations. Accepting down rounds needs to be normalized because a lot of companies are going to just quietly go out of business over the next year. At least with a down round you have a chance to keep fighting.

I didn’t talk about “dirty” term sheets in this post…but TLDR…keep it clean and don’t do stupid things so it appears like you didn’t take a down round.

Investors want high-growth AND efficiency so build a plan based on reality. High spending often comes from seeing success rather than causing success.

Lastly, don’t lie to yourself when building a financial plan. Sure, if you slightly tweak a few assumptions then your company might IPO in 5 years….But when reality hits a lot differently and you have a lot more costs without the associated revenue then it might be too late to change course.

You have 99+ problems running a company, don’t let your pride of not wanting a down round be something that kills your company.

100% true. The other challenge though is wiping out employee equity. The prob of a sizable liquidity event, and meaningful returns to employees in the best of times is very low (your previous article). Because of the frothy fundraising env in 2021 and before, I suspect that the down-rounds will be sizable (60%+ on last valuation) and hence the expected value of employee equity is ~0

Good read for investors who should be watching how companies respond to the large drops in valuations from 2021.